U.S. producer Western Uranium & Vanadium well positioned to profit from the current uranium price boom

Uranium prices are on a tear. Uranium prices have moved ~42% higher in 2023 YTD, mostly in the past few months. In the last month alone prices have surged ~20% higher. Prices are the highest since the Fukushima nuclear reactor disaster in 2011.

InvestorNews has been warning of a uranium deficit for well over a year as you can read here.

A combination of increasing demand and restrained supply is helping the uranium price move higher. Mining analyst John Meyer was recently quoted by Reuters stating:

“The market has been slowly building higher prices as mining costs rise and nuclear generators look to build stocks to guard against increasingly risky supply-side issues…We see prices rising year-on-year for next 10-20 years or till the world finds another source for large scale un-interruptible base load power with a low carbon footprint.”

Uranium prices have surged higher in the past 2-3 months, now at US$70/lb

Source: Trading Economics

Today’s company has been waiting for this moment in time to begin to prosper from higher uranium prices. Their President, CEO, and Director George Glasier has been preparing the company for exactly this outcome.

Western Uranium & Vanadium Corp.

Western Uranium & Vanadium Corp. (CSE: WUC | OTCQX: WSTRF) (“Western”) is a Colorado-based uranium and vanadium conventional mining company focused on low cost production of uranium and vanadium in the western United States. Western has been stockpiling ore ready to be sold at a later date. Western is currently mining at their 100% owned Sunday Mine Complex in Colorado. They also own the San Rafael Project in Utah, the Hansen/Taylor Ranch Project in Colorado, and have a royalty interest in the Bullen Oil & Gas Property. Western has also developed a kinetic separation technology.

Western is further developing and mining their Sunday Mine Complex with underground drilling and blasting to expand its resources. As announced in June 2023 the GMG Ore Body is now ready for full-scale production which will produce high-grade uranium and vanadium ore. Western states:

“The results from the ongoing project at the Sunday Mine Complex (“SMC”) continue to vastly exceed expectations…high-grade uranium ore was continuously intersected. This caused the team to shift from development to mining and stockpiling of the ore...Underground drilling will explore areas of the SMC project site that were never drilled due to the mountainous terrain limiting surface exploration drilling.“

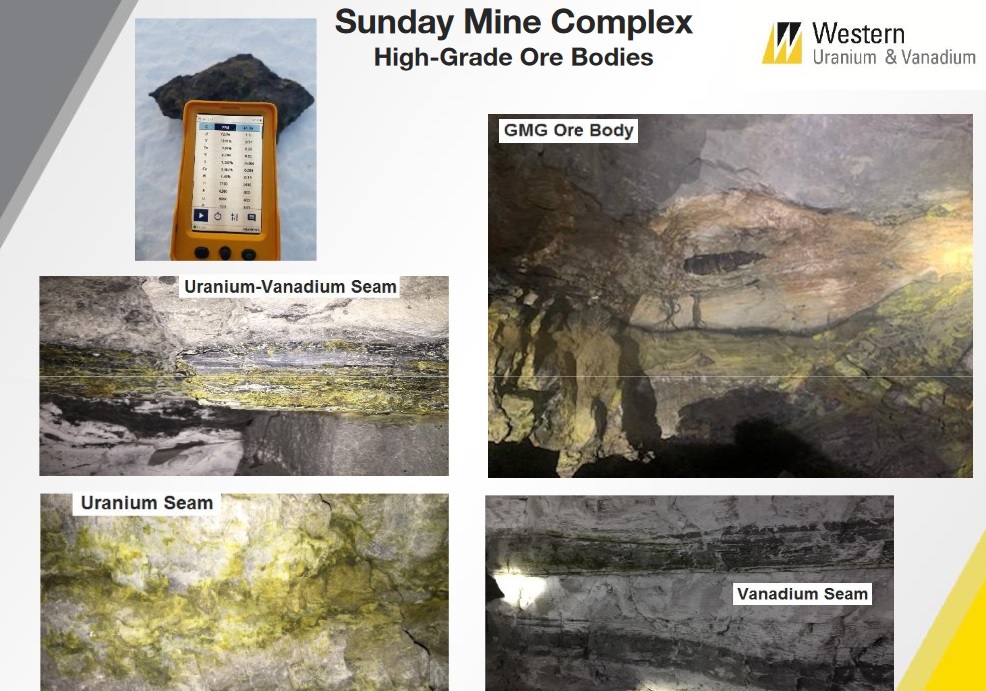

Western’s high grade Sunday Mine Complex is made up of 5 underground projects in Colorado – The image shows seams of high grade uranium and vanadium

Source: Company presentation

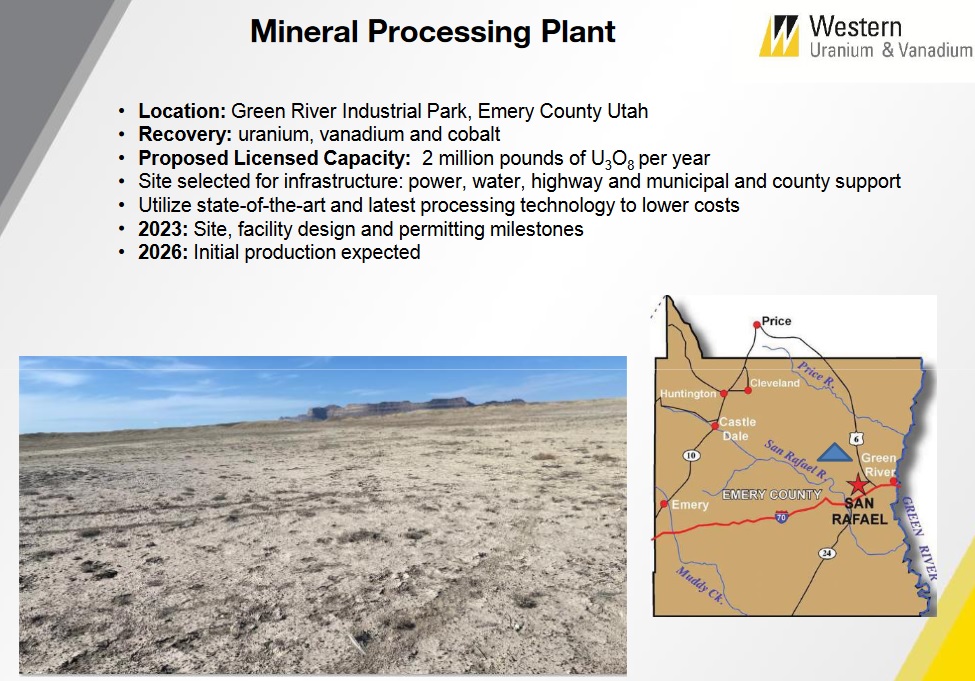

Mineral processing plant in Utah in the making

Western has also been working towards a new state-of-the-art mineral processing plant in Utah, where plans were recently upsized to allow for the future scale of operation to be increased beyond the initial planned annual production of 2 million pounds of uranium and 6-8 million pounds of vanadium.

Western states:

“The Utah mill site in the Green River Industrial Park has been upsized through the addition of adjacent land. This allows the future scale of operation to be increased beyond the initial planned…The selection process for engineering, environmental, and permitting contractors remains ongoing.”

Western plans to build a mineral processing plant in Utah with initial production targeted for 2026

Source: Company presentation

Western’s master plan for the years ahead (source)

- Explore, develop and mine uranium & vanadium across their Sunday Mine Complex.

- Sell product only at acceptable prices.

- Advance a mineral processing plant into 2026 production.

- Develop San Rafael as the 2nd production center.

- Consider & develop mining methods at Hansen/Taylor as 3rd production center.

Closing remarks

The uranium price has surged higher and now sits at a US$70/lb, the highest price its been in over 12.5 years.

Western’s patience is now being rewarded. After redevelopment of their Sunday Mine Complex in 2022 and reopening the mine in January 2023, the ore that they have been mining can now potentially be sold at strong prices. We will have to wait for a further update from the Company on this.

Trading on a market cap of only C$64 million, Western Uranium & Vanadium is only one of less than a handful of U.S uranium producers well placed to profit from the current uranium price boom. Stay tuned.