Technology Metals Report (02.02.2024): Rumors between MP and Lynas, Tesla EV Recall – the Rightsizing of Critical Minerals Begins?

Welcome to the latest Technology Metals Report (TMR), where we highlight the Top 10 news stories that members of the Critical Minerals Institute (CMI) have forwarded to us over the last 2 weeks.

In early 2024, the rare earths sector is witnessing significant strategic movements amidst a backdrop of declining prices and geopolitical tensions. Lynas Rare Earths Ltd. and MP Materials Corp., key players outside China, are rumored to be considering a mega-merger in response to falling rare earth prices and to mitigate the impact of Chinese trade restrictions. This potential consolidation aims to strengthen their production capabilities and align with the Australian and US governments’ efforts to reduce reliance on Chinese supplies, particularly for defense applications.

CMI’s Jack Lifton comments, “In the swirling rumors of a mega-merger between MP Materials and Lynas Rare Earths, it’s clear that the OEM industry’s disdain for single sourcing of critical materials is being overlooked. Litinski is eager to deploy his capital before it devalues, while Lacaze eyes a boost in share price ahead of her retirement. This scenario is akin to two veterans of the trade, unadorned and stark, facing the harsh daylight. Both MP and Lynas are in a precarious position, each with a singular customer and seemingly devoid of new strategies to navigate the market’s tumultuous waters.”

Concurrently, the industry is adjusting to market corrections, as highlighted by the Critical Minerals Institute’s observations on the electric vehicle (EV) materials market, indicating a shift towards efficiency and cost management. Meanwhile, initiatives like Controlled Thermal Resources Holdings Inc.’s funding quest for its lithium brine project and Appia Rare Earths & Uranium Corp.‘s (CSE: API | OTCQX: APAAF) exploration successes underscore the ongoing diversification and expansion within the critical minerals domain. These developments reflect a broader industry trend towards securing resilient supply chains for critical minerals amidst fluctuating market dynamics and geopolitical pressures.

Also breaking news today, Tesla Inc.: The EV maker is recalling 2.2 million vehicles, or nearly all of its electric vehicles in the United States, due to incorrect font size on warning lights, which increases the risk of a crash, the National Highway Traffic Safety Administration (NHTSA) said. This is more than the 2.03 million vehicles it recalled in the United States two months back, its biggest-ever such move at the time, to install new safeguards in its Autopilot advanced driver-assistance system. The latest recall includes vehicles across Tesla’s various models, including the Model S, Model X, 2017-2023 Model 3, Model Y, and 2024 Cybertruck vehicles, the NHTSA said. Separately, U.S. safety regulators said they have upgraded their probe into Tesla vehicles over power steering loss to an engineering analysis – a required step before they could potentially demand a recall.

Lynas linked to rare earths mega-merger as price falls bite (February 2, 2024, Source) — Amid a sharp decline in rare earths prices and concerns over Chinese trade restrictions, there are speculations that Lynas Rare Earths Ltd. (ASX: LYC) may be considering a merger with its New York-listed rival, MP Materials Corp. (NYSE: MP). Industry insiders suggest that the two companies, both leading non-China producers of essential rare earth materials used in defense and various industries, could be in talks to create a mega-merger. The exact details of the deal are unclear, given the current slump in rare earth prices and Western concerns about China’s dominant position in the supply chain. However, a potential merger between Lynas, based in Western Australia and Malaysia, and MP, operating in California’s Mountain Pass, aligns with efforts by the Australian and US governments to strengthen collaboration between their resource companies for critical minerals extraction and processing, reducing dependency on China. Both Lynas and MP have suffered significant stock price declines, and a merger could help them bolster production capabilities and meet growing demands, particularly from the US Department of Defense, which aims to reduce reliance on Chinese supplies. Referral, CMI Co-Chairman Jack Lifton

Critical Minerals “rightsizing” in reaction to governments’ efforts to regulate market (February 1, 2024, Source) — The critical minerals industry is undergoing significant changes in the electric vehicle (EV) materials market. Jack Lifton, Co-Chairman of the Critical Minerals Institute (CMI), views recent price declines in key EV component materials as a natural market correction rather than a disaster, emphasizing minimal regulatory intervention. Declining profits for industry leaders, including China Northern Rare Earth, result from overestimated EV demand, economic factors, and falling sales, especially in California. Lifton advises investors to focus on efficient, low-cost producers, particularly in neodymium. The January 2024 CMI Report notes the U.S. government’s plan to ban Pentagon battery purchases from major Chinese companies and hints at potential recovery in lithium prices. Lynas Rare Earths’ revenue drop reflects market trends but also strategic capacity expansion. In summary, the industry faces short-term challenges but underscores the importance of efficiency, cost management, and adaptability for long-term success. Source, Investor.News

GM, Stellantis-Backed Lithium Startup Seeks More Than $1 Billion for Brine Project (February 1, 2024, Source) — Controlled Thermal Resources Holdings Inc., (CTR) a US lithium startup backed by Stellantis N.V. (NYSE: STLA) and General Motors (NYSE: GM), seeks over $1 billion in funding for its California lithium brine project. This initiative defies the industry’s 80% drop in lithium prices since late 2022. CTR’s unconventional approach focuses on geothermal brine deposits, seen as a potential future lithium supply source once technology challenges are overcome. This aligns with US government efforts to establish a domestic EV commodity supply chain. The funding plan includes equity and debt financing, with Goldman Sachs as the lead bank. Stellantis and GM have previously invested significantly in CTR to secure lithium for EV production. Referral, CMI Co-Chairman Jack Lifton

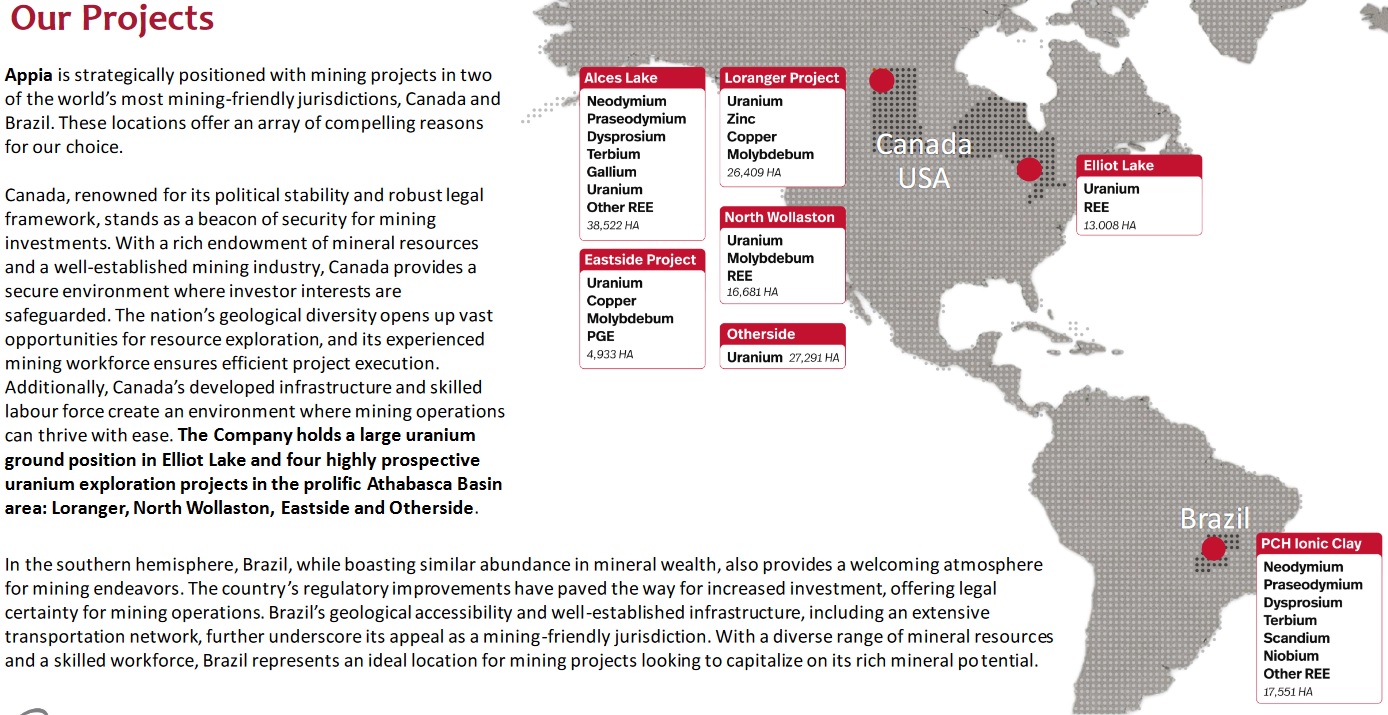

Attention set on rare earths in Canada and Brazil, Appia hits 2024 running (January 31, 2024, Source) — Appia Rare Earths & Uranium Corp. (CSE: API | OTCQX: APAAF) is focusing on its rare earths projects in Canada and Brazil: the Alces Lake Project and the PCH Ionic Clay Project. The Alces Lake Project in Canada is recognized for its high-grade rare earths and gallium in monazite ore. Recent drill results have shown up to 1.57 wt.% Total Rare Earth Oxides (TREO) with mineralization extending to a depth of < 85 meters. In Brazil, the PCH Project offers a simplified extraction process for rare earths essential for electric motor magnets in most EVs. Hole RC-063 reported a total weighted average of 3.87% TREO. Appia’s expansion of mining claims and plans for a Maiden Resource in Q1, 2024, signal their commitment to these projects, with a market cap of C$27 million suggesting a potentially significant year ahead in 2024. Source, Investor.News

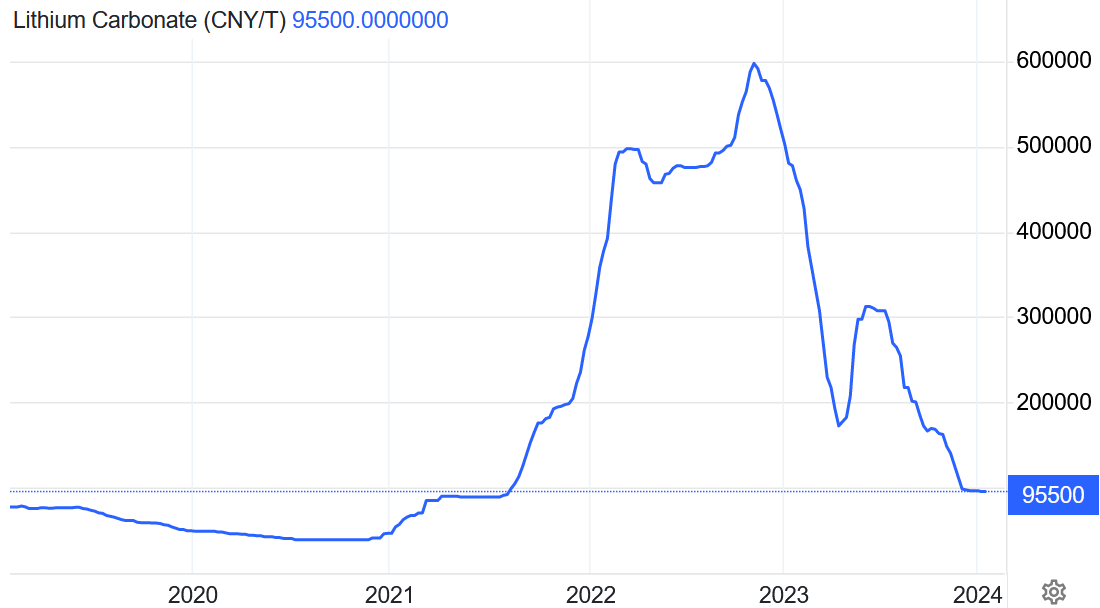

China EVs: lithium producers Ganfeng, Tianqi issue profit warnings, blame price plunge for battery material as stocks sink (January 31, 2024, Source) — Chinese lithium producers Ganfeng Lithium and Tianqi Lithium have issued profit warnings, attributing their declining profits to a significant drop in lithium prices. Ganfeng expects its 2023 net profit to plummet by 70-80% to between 4.2 billion yuan and 6.2 billion yuan. After accounting for non-recurring items, net profit will range from 2.3 billion yuan to 3.4 billion yuan, down 83-88.5% from 2022 levels. Tianqi anticipates a net profit decline of 62.9-72.6% to 6.62 billion yuan – 8.95 billion yuan. Both companies attribute their struggles to the cyclical nature of the lithium industry and declining lithium prices. The average price of China-produced lithium hydroxide exported to South Korea fell by 45% last month. While electric vehicle sales are still growing, the rate has slowed, impacting lithium demand. However, global lithium demand is expected to rise by 27% this year, with a surplus expected before a deficit in 2026. Referral, CMI Co-Chairman Jack Lifton

Mining analyst-turned-Vital Metals CEO eyes much larger Nechalacho reboot (January 29, 2024, Source) — Geordie Mark, CEO of Vital Metals Limited (ASX: VML), aims to revamp the Nechalacho rare earths project in the Northwest Territories, leveraging 15 years of experience as a mining analyst. Recognizing the growing demand for rare earth elements in the technology and electric vehicle (EV) markets, Mark plans to shift Vital’s strategy towards a bulk tonnage operation targeting lighter rare earths like praseodymium and neodymium. This comes after the failure of the company’s processing division and a Chinese investment lifeline in 2023. A comprehensive scoping study is crucial for long-term viability, and Mark expects demand for praseodymium and neodymium to rise significantly in the next decade, particularly in China and Europe. Shenghe Resources’ investment provides vital capital for Nechalacho’s development, positioning it to compete with North America’s only rare earths mine, MP Materials Corp.’s (NYSE: MP) Mountain Pass operation. Referral, CMI Co-Chairman Jack Lifton

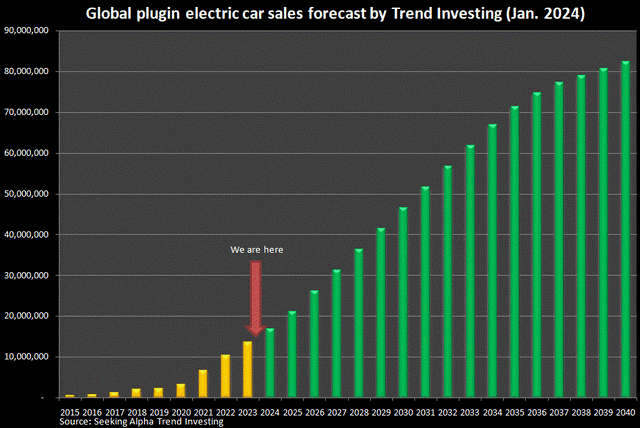

The Critical Minerals Institute Report (01.25.2024): U.S. government bans Pentagon battery purchases from major Chinese companies starting October 2027 (January 25, 2024, Source) — The January 2024 Critical Minerals Institute (CMI) report highlighted key economic and geopolitical developments. U.S. inflation in December 2023 impacted interest rate reduction plans, while the S&P 500 rose by 2.04% year-to-date. China’s economy slowed, with falling home prices, and global tensions persisted. In the global electric vehicle (EV) market, December 2023 set a record for plugin electric car sales, led by China. However, the EV sector’s growth rate slowed compared to previous years. The U.S. reported a surge in EV sales and enacted Zero Emission Vehicle mandates to boost adoption. In the EV battery sector, the U.S. government announced a ban on Pentagon battery purchases from major Chinese companies, starting October 2027. Challenges in the critical minerals sector included depressed prices due to oversupply and slowing EV market growth. Recovery in lithium prices was anticipated in late Q1 or early Q2 2024. The report emphasized a negative supply response from producers and expected a potential recovery in the second half of 2024, assuming reasonable EV sales growth. Source, Investor.News

Tesla Projects Slower Growth in 2024 as EV Demand Softens (January 24, 2024, Source) — Tesla Inc. (NASDAQ: TSLA) anticipates slower growth in 2024 amid a challenging landscape for the electric vehicle (EV) industry. CEO Elon Musk desires greater control, aiming for a 25% ownership stake to deter activist shareholders. This follows Musk’s ultimatum to shift focus to AI and robotics if control isn’t achieved. Tesla faces declining demand, shrinking profit margins, heightened competition, and recent price cuts. Despite doubling fourth-quarter net income to $7.9 billion, costs for projects like the Cybertruck and AI research impact profitability. Tesla’s valuation, historically tied to sales and Musk’s vision, faces uncertainty. Challenges include Hertz selling EVs and Chinese automakers overtaking Tesla. EV enthusiasm wanes due to pricing, charging concerns, and range limitations. Tesla plans cost reduction for future vehicles but encounters short-term cost pressures. Despite this, strong Cybertruck demand is expected, with production scaling up gradually. Referral, CMI Director, Alastair Neill

Rare-earths miner Lynas’ Q2 revenue halves on falling prices, lower China demand (January 24, 2024, Source) — Australia’s Lynas Rare Earths reported a significant drop in its second-quarter revenue, falling by 51.7% to A$112.5 million due to plummeting rare earth prices and reduced demand in China, particularly in the appliance sector amid a construction slowdown. This decline in revenue, which missed analysts’ forecasts, led to a 30-month low in its share prices. Despite this downturn, Lynas has continued to expand its operations, including the near-completion of its Kalgoorlie processing plant in Australia, upgrades to its Malaysian facilities, and ongoing work at the Mt Weld mine. The company, a major supplier outside China, has also been working on a new facility in Texas to serve the U.S. Department of Defense. Despite these efforts, Lynas’ challenges are compounded by the lower average selling price of its products, which has more than halved compared to last year. Referral, CMI Director, Russell Fryer

Investors turn to copper, gold and uranium amid battery metals rout (January 24, 2024, Source) — In 2024, investors are shifting their focus away from battery metals, such as nickel and lithium, due to significant price declines. Instead, they are turning to commodities like copper, gold, and uranium. Copper prices have rebounded following supply shortages and disruptions in production by key global producers. Gold is experiencing renewed interest, driven by geopolitical crises and a weakening US dollar, with forecasts predicting it to trade above $2,000 per ounce in the coming year. Uranium has gained substantial momentum, reaching decade-high prices, driven by limited supply and increased demand for nuclear energy in Western countries. Investors are diversifying their portfolios, seeking better prospects in these alternative commodities. Referral, CMI Director, Russell Fryer

China, in comic strip, warns of ‘overseas’ threats to its rare earths (January 22, 2024, Source) — China’s State Security Ministry released a comic strip on social media, depicting foreign threats to its rare earth resources. The narrative shows security officers uncovering covert operations by foreign-looking characters, suggesting overseas interest in China’s strategic minerals. China, the leading producer of rare earths essential for high-tech industries, has imposed export restrictions on these elements and related technologies, citing national security. The move has heightened tensions, particularly with the United States, amidst accusations of economic coercion. The comic underscores the importance of safeguarding these resources against international competition and espionage. The state-controlled Global Times highlighted the story, reflecting on the global race for rare earths, vital in military, consumer electronics, and renewable energy sectors, as a national security issue. Referral, CMI Director, Alastair Neill

Tanzanian, Canadian firms to search for rare metal (January 22, 2024, Source) — Tanzanian firm Memnon Project Management Services Company Limited and Canadian company Anibesa Energy Metals Corp. are set to collaborate in prospecting for niobium in Mbozi District, Songwe Region, with an anticipated investment of up to $50 million. They have obtained regulatory approvals and are finalizing the acquisition of three licenses for niobium minerals, while three more geologists are expected to join the exploration team. Memnon Project Management Services is involved in various projects, including the Kongwa Lithium Project and solar energy initiatives. Niobium, a rare metal, enhances the strength of alloys and is used in various industries, including aerospace and construction. As of 2022, Brazil held the largest niobium reserves globally. The partnership aligns with Tanzania’s goal of attracting international companies to boost the mining industry by focusing on valuable critical metals projects. Referral, CMI Director, Alastair Neill

Investor.News Critical Minerals Media Coverage:

- February 01, 2024 – Critical Minerals “rightsizing” in reaction to governments’ efforts to regulate market https://bit.ly/49f78zC

- January 31, 2024 – Attention set on rare earths in Canada and Brazil, Appia hits 2024 running https://bit.ly/3ueaxjg

- January 25, 2024 – The Critical Minerals Institute Report (01.25.2024): U.S. government bans Pentagon battery purchases from major Chinese companies starting October 2027 https://bit.ly/4961zU0

- January 22, 2024 – Unveiling Insights from Ecclestone on the Future of Mining and Investment from Riyadh’s Future Minerals Forum Event https://bit.ly/491pVOS

Critical Minerals IN8.Pro Member News Releases:

- February 2, 2024 – Appia Announces Plans for Drilling at the Loranger Uranium-Bearing Property, Saskatchewan, Canada https://bit.ly/3UphbOs

- February 1, 2024 – Obonga: Wishbone Exploration Permit Application https://bit.ly/3UlnFOj

- February 1, 2024 – First Phosphate to Provide Project Update to the Federation of Chambers of Commerce of the Saguenay-Lac-Saint-Jean Region of Quebec, Canada https://bit.ly/42ugvt1

- January 31, 2024 – Defense Metals Announces Closing of its $738,836 Non-Brokered Private Placement https://bit.ly/3umNv9S

- January 31, 2024 – First Phosphate Announces Launch of 25,000 m Drill Campaign at its Bégin-Lamarche Project https://bit.ly/3SmPtPD

- January 30, 2024 – Ucore Announces Closing of Debenture Offering https://bit.ly/3SHT1xa

- January 30, 2024 – Western Uranium & Vanadium Bolsters Mining Team to Scale-Up Uranium Production https://bit.ly/47UTIHZ

- January 30, 2024 – F3 Hits 2.05m Off Scale >65,535 CPS in First Hole of Winter Program at JR Zone https://bit.ly/3SCxru9

- January 29, 2024 – First Phosphate Confirms Two Additional New High-Grade Discoveries at Begin-Lamarche Property and up to 39.45% P2O5 at Larouche https://bit.ly/3OlGWew

- January 29, 2024 – American Rare Earths Quarterly Activities Report for the Period Ending 31 December 2023 https://bit.ly/3SBQQeM

- January 29, 2024 – Australian Strategic Materials Quarterly Activities Report to 31 December 2023 https://bit.ly/3UdGXVK

- January 26, 2024 – Appia Rare Earths & Uranium Corp. Announces New Cooperation Agreement with the Ya’thi Néné Lands and Resources Office https://bit.ly/3Oke4TU

- January 25, 2024 – First Phosphate, American Battery Factory and Integrals Power Sign MOU to Produce LFP Cathode Active Material and Battery Cells in North America https://bit.ly/48MnCiU

- January 23, 2024 – F3 Announces Commencement of Drilling at PLN https://bit.ly/3Uc6COo

- January 23, 2024 – Power Nickel Announces Filing of Amended Technical Report https://bit.ly/3HvYPUd

- January 23, 2024 – First Phosphate Corp. Welcomes the Addition of Apatite (Phosphate) to the Critical and Strategic Minerals List of Quebec, Canada https://bit.ly/48Pv7Wf

- January 22, 2024 – First Phosphate Announces Closing of the Third and Final Tranche of Oversubscribed Private Placement Financing for Total Gross Proceeds of $8.2 Million https://bit.ly/3U5Vl2l

- January 22, 2024 – Elcora Develops Innovative Process To Extract Vanadium From Its Moroccan Vanadinite Deposit https://bit.ly/3Hu8Zon

- January 22, 2024 – American Rare Earths Announces Breakthrough Metallurgical Results https://bit.ly/3O96trp

- January 22, 2024 – F3 Expands PLN Project with Acquisition of PW Property from CanAlaska https://bit.ly/3vKBMTb