CoTec says ‘Yes to ESG!’ and Critical Minerals Technology

In an era where China dominates the critical minerals supply chain, there is a strong need for Western companies to develop and innovate better ways to mine and process critical minerals. New disruptive technologies that are not only ESG-friendly, but cost-effective are needed to help the West compete with China. Demand for green technologies is expected to soar as the resource industry seeks cleaner, more efficient ways to extract and process minerals.

CoTec Holdings Corp.

CoTec Holdings Corp. (TSXV: CTH | OTCQB: CTHCF) (“CoTec”) is an ESG focused commodity extraction disruptor. CoTec acquires innovative technologies that can be used to better extract and process minerals in the mining industry in a greener and more cost-effective way. A key focus is on recycling and mine waste stream projects as they are typically much faster to reach production than discovering and developing a conventional new producing mine.

CoTec states: “These technologies, requiring significantly less energy and water, transform undervalued commodity-rich assets into profitable ventures while focusing on recycling and waste mining. This not only produces critical minerals rapidly, but also accelerates revenue generation compared to traditional processes.”

CoTec’s business model

CoTec’s business model is to create a revenue generating portfolio of diversified high-margin, eco-friendly assets in commodities that support the energy transition. A key differential is that focusing on recycling and mine tailings can lead to much faster ramp-up in production than a conventional mine.

CoTec states:

“CoTec intends to use disruptive scalable technology to:

- Produce metals and minerals faster than developing conventional greenfield mines

- Build low carbon plants to generate green steel inputs, produce green recycled magnets and rare earths, produce green copper.

CoTec intends to reduce the development timeline in comparison to conventional greenfield mines within the following areas:

- Reduce timeline for permitting approvals

- Using existing infrastructure and power

- Lower capital costs, including access to governmental funding

- Quicker resource and reserves vs. greenfield mines.”

CoTec’s business model summary

Source: CoTec company presentation

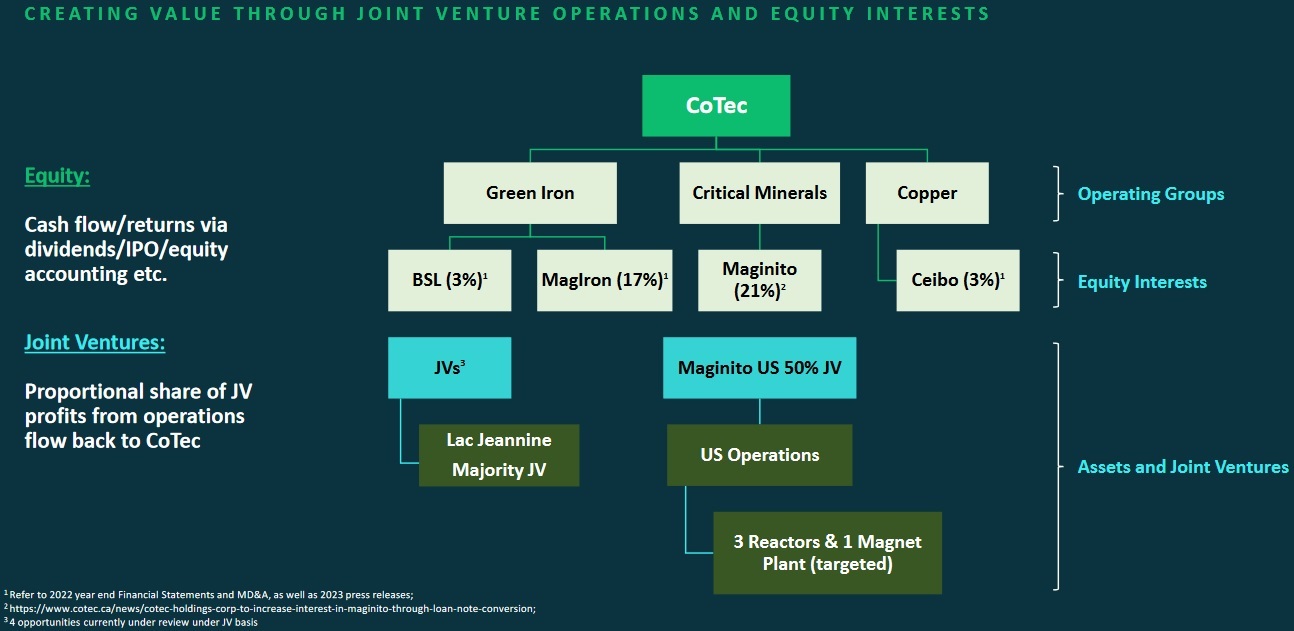

CoTec’s technologies and asset projects are focused on three operating groups – critical minerals, green iron, and copper.

CoTec holds stakes in four key technologies and three assets, with the goal of obtaining 10 technologies, and 30-40 assets. CoTec’s current investments include:

- Maginito Limited (20.6% equity interest and a 50-50 JV right) – Collaboration on deploying a patented process to extract rare earths from recycled material in the USA.

- MagIron (17% equity interest) – A brownfields restart of an iron ore processing plant (Plant 4) in the midwestern United States designed to process previously discarded waste materials from historical mining operations; and a beneficiation technology that can be applied to the waste material.

- Binding Solutions Limited (“BSL”) (~3% equity interest) – BSL has developed a proprietary cold agglomeration technology for the production of high-quality clean pellets from primary materials, waste dumps, and stockpiles. Includes an exclusive right to participate in JVs with BSL in certain jurisdictions. BSL has recently announced a strategic investment by Mineral Resources Limited (ASX: MIN), a top 5 Australian iron ore producer. CoTec acquired an asset option for the Lac Jeannine property for iron ore tailings to apply the BSL technology.

- Ceibo (~3% equity interest) – A transformational low-carbon copper heap leaching technology which targets chalcopyrite and other refractory copper minerals. Recently Ceibo announced that BHP Ventures has joined as an investor closing Ceibo’s Series B financing.

A summary of CoTec’s equity interests and JVs

Source: CoTec company presentation

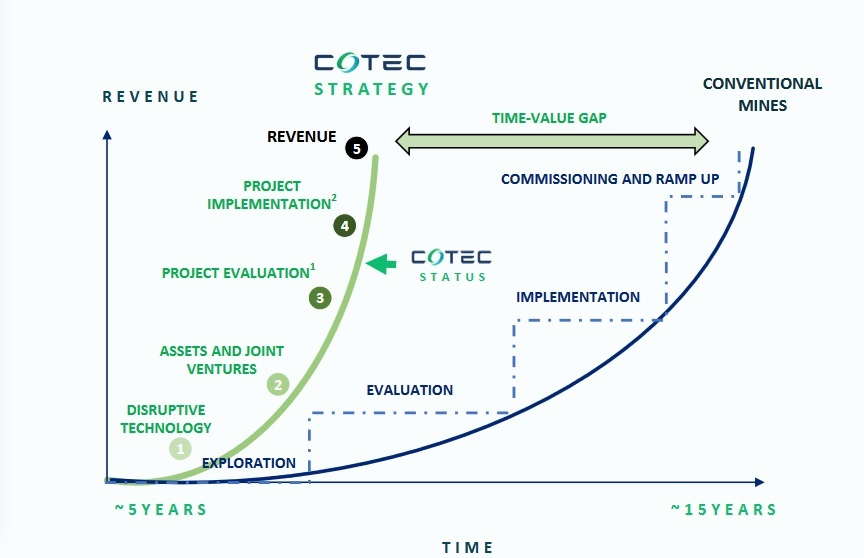

The various projects discussed above are at the evaluation stage. The next stage would be detailed engineering, then construction with the Project owners’ teams, followed potentially by production and revenues.

CoTec’s strategy is to focus on recycling and waste mining which potentially has a much faster timeline to production

Source: CoTec company presentation

Closing remarks

In life, we all know it is generally wiser to work smarter. This is what CoTec is doing with their focus on innovative technologies and speed to production. Using existing mine waste streams or by using recycled material the time to reach production is dramatically faster than creating a new mine from zero. It is also better for the environment if done in an ESG friendly way.

CoTec Holdings Corp. trades on a market cap of C$44 million.