Energy Fuels on Path to Become the American Critical Mineral Powerhouse

Uranium has been a winning sector in 2023 with uranium prices up 41% YoY, making it the best performing energy commodity in the past year. As the uranium price hovers near a 12 year record high (US$69/lb), today’s company is set to benefit.

25 year uranium price chart shows uranium approximately at the highest level since Jan. 2011

Source: Trading Economics

Energy Fuels Inc.

Energy Fuels Inc. (NYSE American: UUUU | TSX: EFR) (“Energy Fuels”) is the leading producer of uranium and vanadium and a growing rare earths processor, all in the USA.

Energy Fuels holds two of America’s key uranium production centers: The White Mesa Mill in Utah and the Nichols Ranch in-situ recovery (“ISR“) Project in Wyoming. The White Mesa Mill has a licensed capacity of over 8 million pounds of U3O8 per year.

Q2, 2023 financial results

As announced on August 4, 2023, Energy Fuels reported a small net loss in Q2, 2023 of US$4.89 million. The Company reported some nice revenues and profits from its uranium and rare earths sales during the quarter; however, increased expenses associated with preparing four uranium mines for production and expenses associated with developing commercial rare earth element separation capabilities dragged down the bottom line.

The key is that their existing uranium and rare earths operations are profitable with gross margins running at around 50%. Furthermore, the increased expenses are those related to project developments to bring on new uranium production and in time rare earth oxides. The plan is that these expansions should lead to much stronger revenues and potential profits down the track. An analogy could be with Tesla (NASDAQ: TSLA) who ran losses until they got their new EV factories into scaled production.

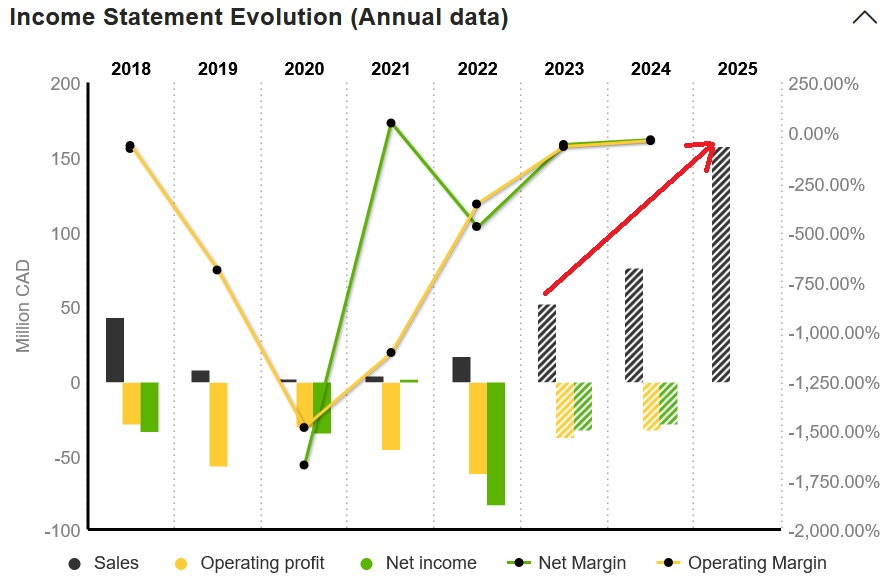

Energy Fuels revenues are forecast to grow rapidly in 2024 and 2025 which should thereafter potentially lead to significant profits depending upon commodity prices

Source: Market Screener (Note: Red arrows by the author)

A robust balance sheet with strong inventory

As of June 30, 2023, Energy Fuels had a robust balance sheet with US$134.36 million of working capital (versus US$116.97 million as of December 31, 2022)

As of June 30, 2023, the Company held 766,000 pounds of finished U3O8, 906,000 pounds of finished V2O5, and 37 MT of finished high-purity, partially separated mixed REE carbonate in inventory.

The strong balance sheet supports Energy Fuels expansion plans.

Energy Fuels expansion potential

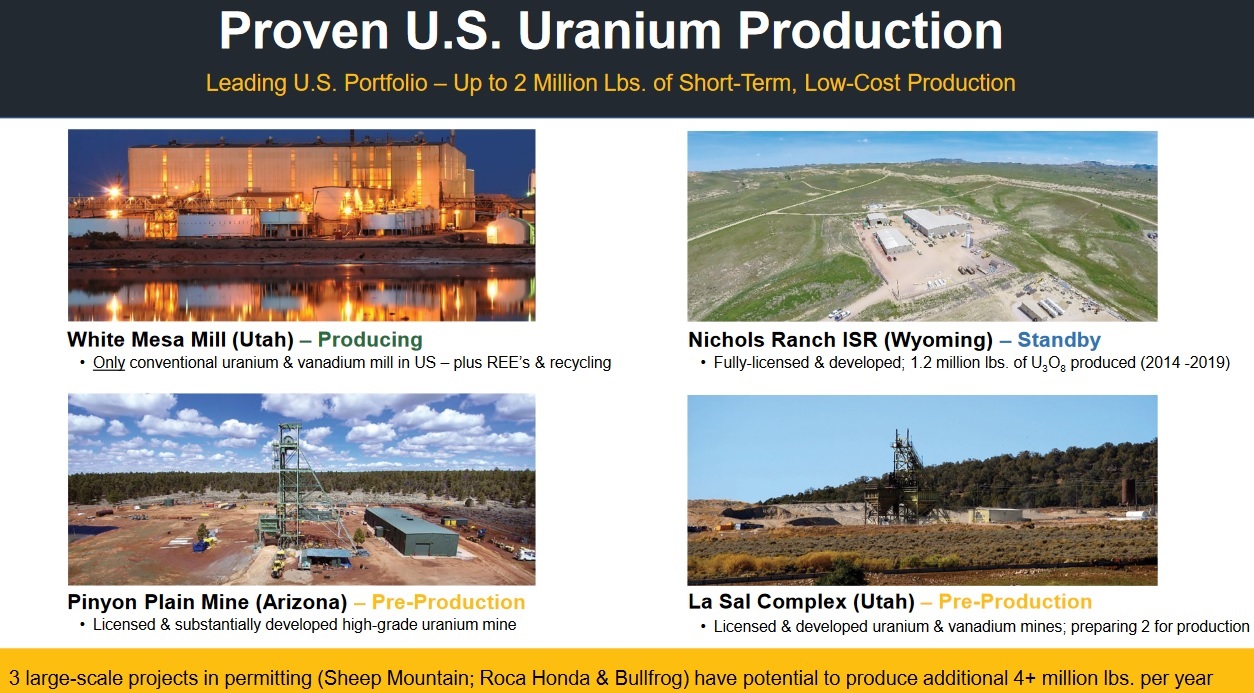

Energy Fuels state they have up to 2 million lbs. of short-term, low-cost uranium production capacity, all located in the USA.

Energy Fuels owns a portfolio of uranium assets with one producing, one on standby, and two in the pre-production stage. They also have 3 large-scale projects in permitting (Sheep Mountain; Roca Honda & Bullfrog) that have potential to produce additional 4+ million lbs. per year.

Energy Fuels most advanced uranium assets

Source: Energy Fuels company presentation

Energy Fuels also has their rare earths processing capacity to produce a mixed rare earth concentrate at their White Mesa Mill in Utah, USA. The near term plan is to expand this to include rare earths separation to produce rare earth oxides. Phase 1 plans to have a capacity of 800 – 1,000 MT of NdPr oxide per year by early 2024 and Phase 2 a capacity of 1,500 – 3,000+ MT NdPr oxide per year by 2026. The Phase 3 plan is to produce separated heavy rare earths including Dy and Tb by 2027. These figures are subject to achieving sufficient monazite ore as feed.

Energy Fuels has also recently acquired the Bahia heavy mineral sand (“HMS”) Project in Brazil which contains significant quantities of monazite (rare earths containing ore), titanium (ilmenite/rutile) and zirconium (zircon).

Closing remarks

Energy Fuels continues to establish itself as a leader in the critical minerals space in the US. They are already the leading uranium, vanadium, and rare earths producer in the USA.

Currently, financial results are not yet reflecting Energy Fuels’ full potential as expenses are elevated to support the Company’s aggressive growth plans.

Energy Fuels Inc. trades on a market cap of US$1.177 billion.

For investors willing to look out just a couple of years as their capacity ramps up very quickly, Energy Fuels should be strongly on your radar.