Can the Western graphite and anode industry rise to meet China’s challenge?

China to impose some graphite and processed graphite materials ‘export permits’ from December 1, 2023

Last week it was reported that China, the world’s top graphite producer plans to curb exports of key battery material by implementing export permits for some graphite products from December 1 to protect national security. Another report stated: “China graphite export restrictions could hinder ex-China anode development….if it lasts into the longer term, it is likely to accelerate the build-out of a localized graphite and battery anode supply chain outside China.”

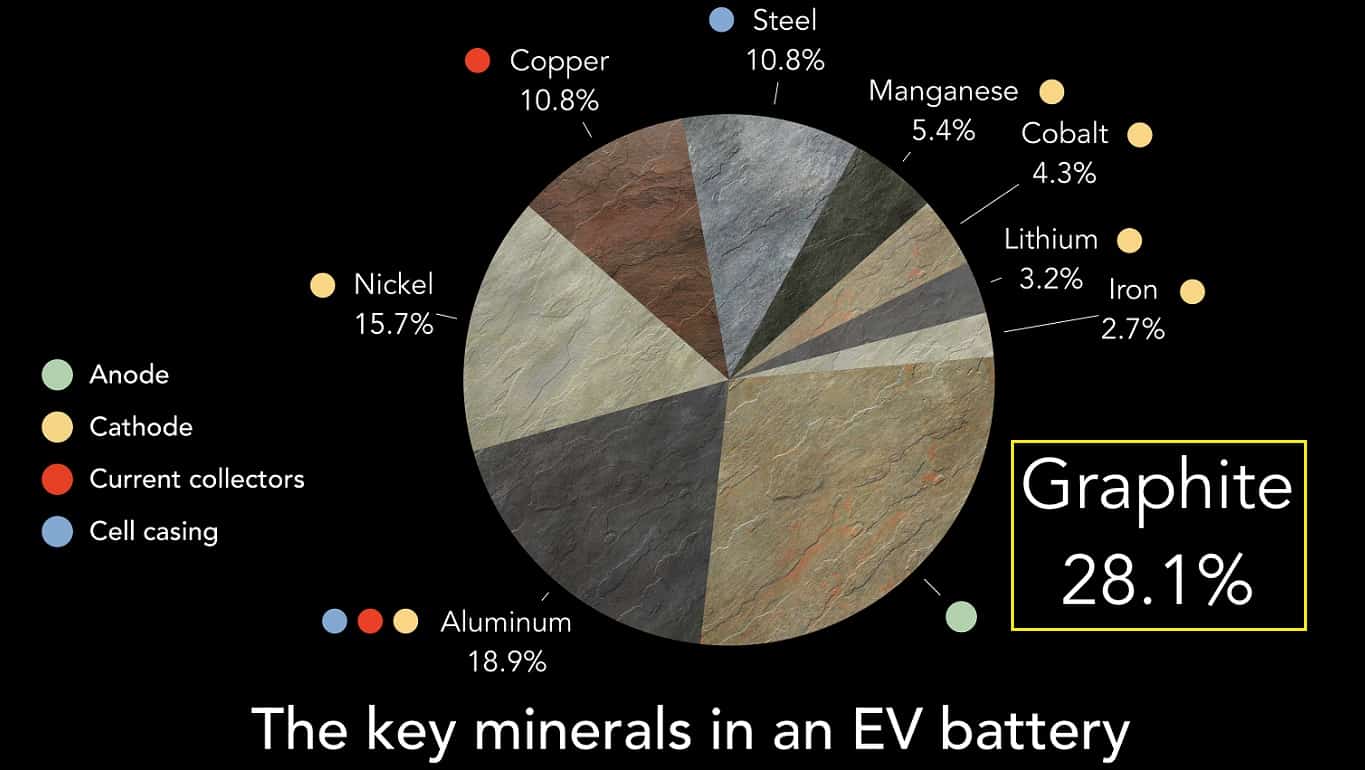

Graphite is the number one metal required for lithium-ion batteries making up about a 28% share. It is used in the anode.

The world is very dependent upon China to supply processed graphite material and anodes for Li-ion batteries

The reason why this is huge news in the graphite world is that China produces 67% of global natural flake graphite supply and refines more than 90% of the world’s graphite into active anode material (typically spherical graphite). If China were to deny or delay permits for spherical graphite it will cause major problems for anode manufacturers outside China, such as those in South Korea, Japan, or North America.

China currently produces ~77% of global lithium-ion batteries and 75-80% of global electric cars, thereby completely dominating the industry. If the West is shut out from sourcing processed EV battery materials from China then they will have a major problem producing their own EVs. China plans to prioritize EV battery materials for their own needs. This is why President Biden introduced the Inflation Reduction Act (IRA) and the EU introduced the EU Critical Raw Materials Act. Both are designed to address the shortages in the EV supply chain and the forecast shortages of future supply of critical raw materials. The problem is the IRA has done little to address the supply of raw materials and the EU Critical Raw Materials Act is woefully inadequate and targets fall way short of what will be needed.

Which western graphite companies can rise to meet the challenge to establish an ex-China graphite supply chain

The leading western graphite companies that are working to establish an ex-China supply chain for flake graphite, synthetic graphite, and spherical graphite include:

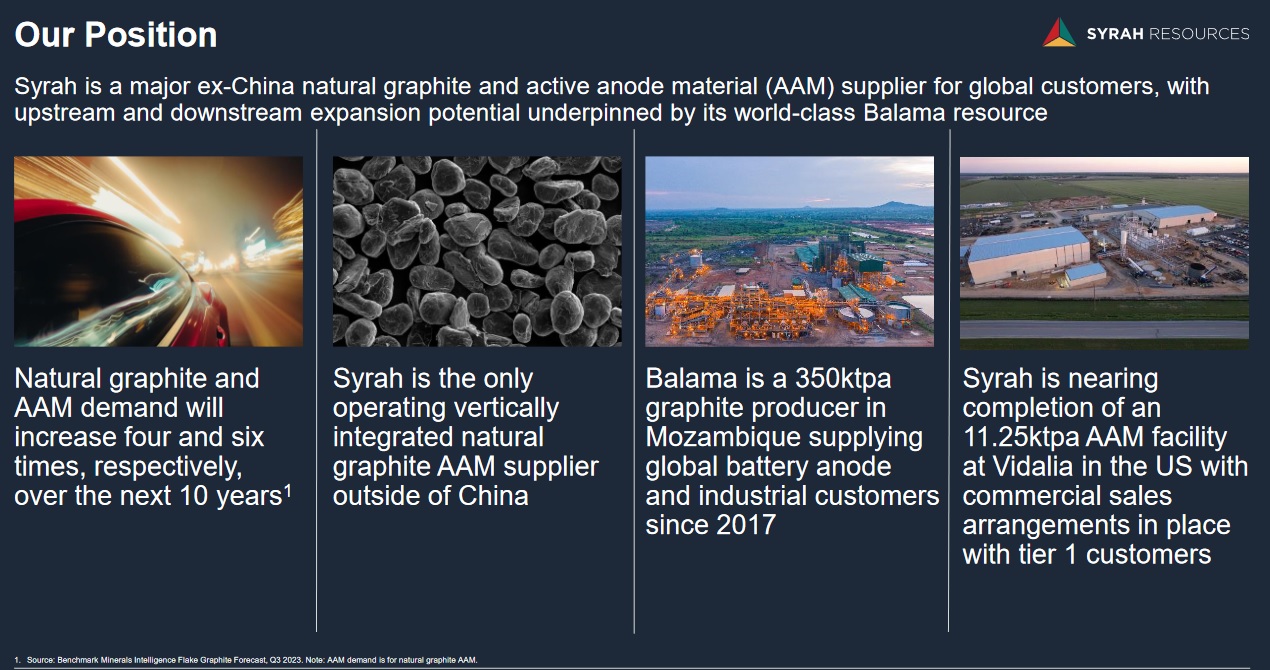

- Syrah Resources Limited (ASX: SYR) – Largest western flake graphite producer with their 350,000tpa flake graphite capacity Balama Mine in Mozambique. Currently constructing the Vidalia spherical graphite facility in Louisiana, USA with Stage 1 production plans to produce 11,250tpa of spherical graphite. Longer term they plan to expand to 45,000tpa in 2026 and then to >100,000tpa by 2030 with an Europe/Middle East facility. Syrah already has an off-take agreement with Tesla (NASDAQ: TSLA). Syrah’s stock price has surged ~80% higher the past week following the release of the China export permits news.

- Nouveau Monde Graphite Inc. (NYSE: NMG | TSXV: NOU) – Is rapidly progressing their plans for their Matawinie Graphite Mine and Bécancour Battery Anode Material Plant in Quebec, Canada. The company is working with Panasonic to qualify their graphite anode material. Panasonic supplies Tesla with batteries.

- Northern Graphite Corporation (TSXV: NGC | OTCQB: NGPHF) – Owns graphite producing and past producing mines in Quebec, Canada and Namibia. They also own the Bissett Creek graphite Project in Ontario, Canada. The Company state that they are “North America’s Only Significant Natural Graphite Producer”. The Company plans to develop one of the world’s largest battery anode materials facilities in Baie-Comeau Québec with 200,000tpa of capacity.

- NextSource Materials Inc. (TSX: NEXT | OTCQB: NSRCF) – A new graphite producer from their Molo Graphite Mine in Madagascar with Phase 1 capacity of 17,000tpa of flake graphite production and plans to expand to 150,000tpa. The Company’s short term plan is for a Battery Anode Facility in Mauritius and longer term for similar facilities in USA/Canada, UK, EU.

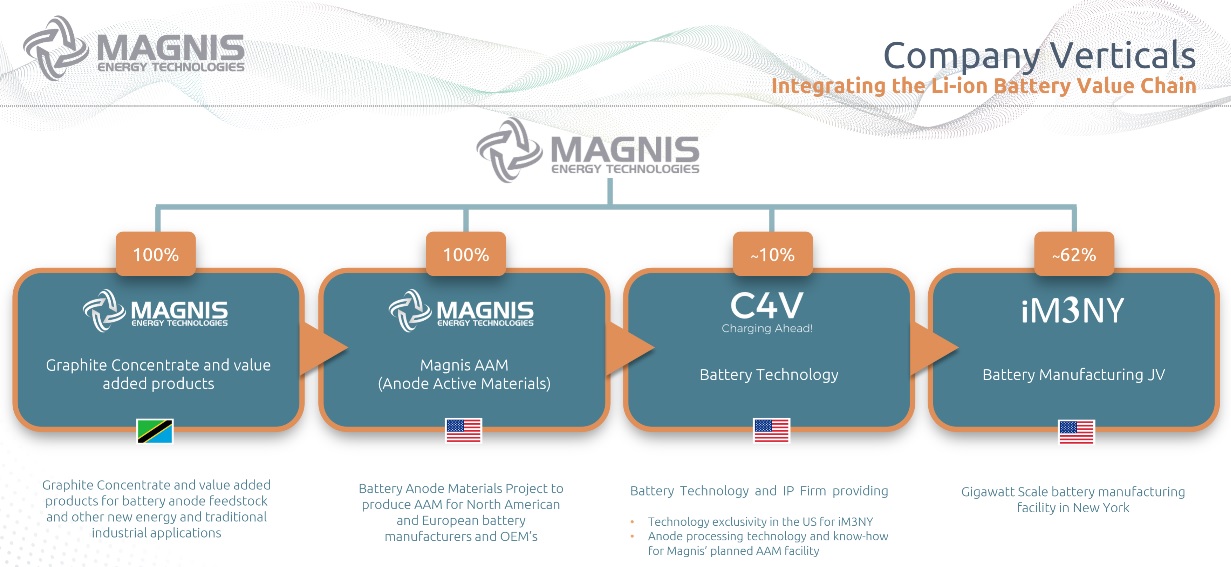

- Magnis Energy Technologies Ltd. (ASX: MNS | OTCQX: MNSEF) – Magnis aims to produce high performance anode materials utilising ultra-high purity natural flake graphite from their Nachu Graphite Project in Tanzania. Magnis’ partially owned U.S.-based subsidiary Imperium3 New York, Inc (“iM3NY”) operates a gigawatt scale lithium-ion battery manufacturing project in Endicott, New York.

- Talga Group Ltd. (ASX: TLG) – Own the integrated mine to anode Vittangi Graphite Project in Sweden. In September 2023 Talga broke ground on their 19,500tpa anode facility, stating “the refinery is projected to be the first commercial anode production in Europe for electric vehicle Li-ion batteries”.

- Novonix Limited (NASDAQ: NVX | ASX: NVX) – Has a production capacity target of up to 20,000 tpa of synthetic graphite anode material from their Tennessee facility in the USA.

- Anovion Technologies (private) – The USA anode producer plans to invest US$800 million to produce a 40,000tpa synthetic graphite anode material facility in Georgia, USA with plans to expand to 150,000tpa by 2030.

Syrah Resources leads the West’s attempt to build an ex-China flake graphite and anode material supply chain

Magnis Energy Technologies is working towards becoming a graphite producer, anode materials producer and is already a small scale JV battery producer in the USA

Closing remarks

The Western world received a loud wake-up call the past week. The China graphite products ‘export permits’ may only serve to restrict or slow down some anode material supply from China, but it puts the West on notice of how dependent they are upon China.

Given the world is rapidly moving to electric vehicles, the West must urgently build up its EV materials supply chains or risk being left behind in the global EV race.

The USA is making some bold moves and the companies discussed in this article are moving in the right direction. Let’s just hope that the western EV supply chain build out accelerates rather than stalls like GM’s latest electric pickup truck plans. I think Americans will want U.S.-branded electric cars and I know Europeans will want European branded electric cars. If we are not careful our only choice one day might be Tesla and Chinese electric cars. Stay tuned.