Under Secretary Jose Fernandez Discusses U.S. Critical Minerals Strategy for Clean Energy Transition

written by InvestorNews | March 6, 2024

In a compelling conversation with InvestorNews host Tracy Weslosky, Jose W. Fernandez, the Under Secretary of State for Economic Growth, Energy, and the Environment for the US, shared insights into the country’s strategic initiatives to secure and diversify the critical minerals supply chain, vital for the clean energy transition. Fernandez emphasized the significance of critical minerals like nickel, manganese, cobalt, and lithium, outlining the efforts to expand their supply to meet future demands.

“The ones—critical minerals—that we’ve been focusing on are the ones that are needed for the clean energy transition. And those are four or five minerals. They include nickel, manganese, cobalt, and lithium. We’re working to find ways to expand the supply of that. And we think that there are opportunities in a number of countries that have reached out to us. Now, what we’re trying to do is really not focus so much on the philosophy of things but actually on concrete projects. How do we go to a country in Africa that’s looking for investment and provide them with an alternative? In order for us to do that, we’re going to have to find the right companies. Our banks are going to have to get involved in the financing. These companies and we are going to have to convince these countries that we will do things the right way.”

Fernandez highlighted the challenges faced by the US in the global supply chain, noting the vulnerability and need to address the monopolization of critical mineral resources. Currently, a significant portion of these essential minerals is controlled by China, presenting a strategic vulnerability for the United States and its allies.

“Companies and organizations have recognized a need, a vulnerability, and a challenge. Simply put, the need is for exponentially greater quantities of critical minerals than we use today. To give you a couple of examples, we will need 42 times the amount of lithium and 25 times the amount of manganese than we use today by 2050. The numbers are staggering. The vulnerability lies in the fact that currently, two-thirds or more of these minerals are owned, controlled, mined, or processed by one country, China. This represents a significant vulnerability. The challenge is for our companies to become more involved in this industry, which is essential for us to diversify our supply chain. To do this, we need to promote our values. Our values include respecting the environment, working with communities, and doing everything we can to improve transparency. These are our selling points. Despite the progress not being as fast as we would like, we are making headway.”

The interview underscored the United States’ proactive approach to not just securing but also ethically sourcing critical minerals necessary for the global transition to clean energy.

The Critical Minerals Institute Report (01.25.2024): U.S. government bans Pentagon battery purchases from major Chinese companies starting October 2027

written by Matt Bohlsen | March 6, 2024

Welcome to the January 2024 Critical Minerals Institute (CMI) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the CMI List of Critical Minerals or visit the CMI Library.

Global macro view

January 2024 saw a slight rise in U.S. inflation reported from 3.1%pa in November to 3.4%pa in December 2023. This has led market commentators to suggest the proposed 2024 interest rate reductions may be pushed out to H2, 2024, or be smaller in nature.

The next U.S. Fed rates announcement is due on January 31, 2024, and no changes in rates are expected. Year to date, as of January 21, 2024, the S&P 500 is up 2.04%. U.S. GDP looks set to slow in Q4, 2023 (announcement due 25 January 2024) with forecasts for 2% annualized growth, which would result in a 2023 GDP of ~2.7%. 2024 U.S. GDP is forecast to be ~2.2%. The U.S. consumer remains resilient with U.S. employment very strong.

China continues its property led slowdown with 2023 GDP recently reported at 5.2% annualized. China’s December new home prices fell at the fastest pace in almost 9 years. Despite this the Chinese Central Bank left rates unchanged, defying expectations for a 0.1% cut.

The Russia-Ukraine war continues as does the Hamas-Israel war which last month spread to include the U.S. and UK forces bombing Iran-backed Houthis over their attacks in the Red Sea. The Middle East is a hotbed ready to explode.

Global plugin electric vehicle (“EV”) update

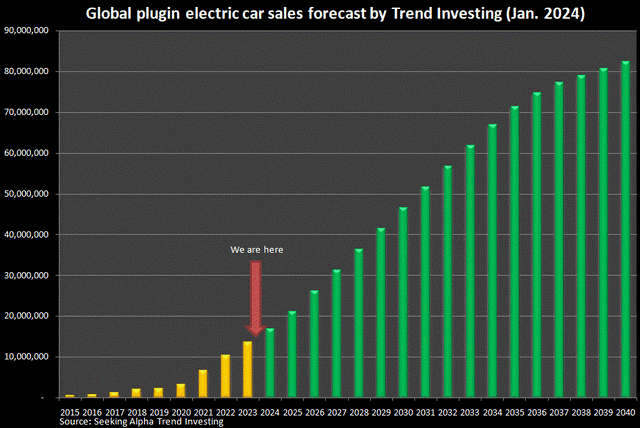

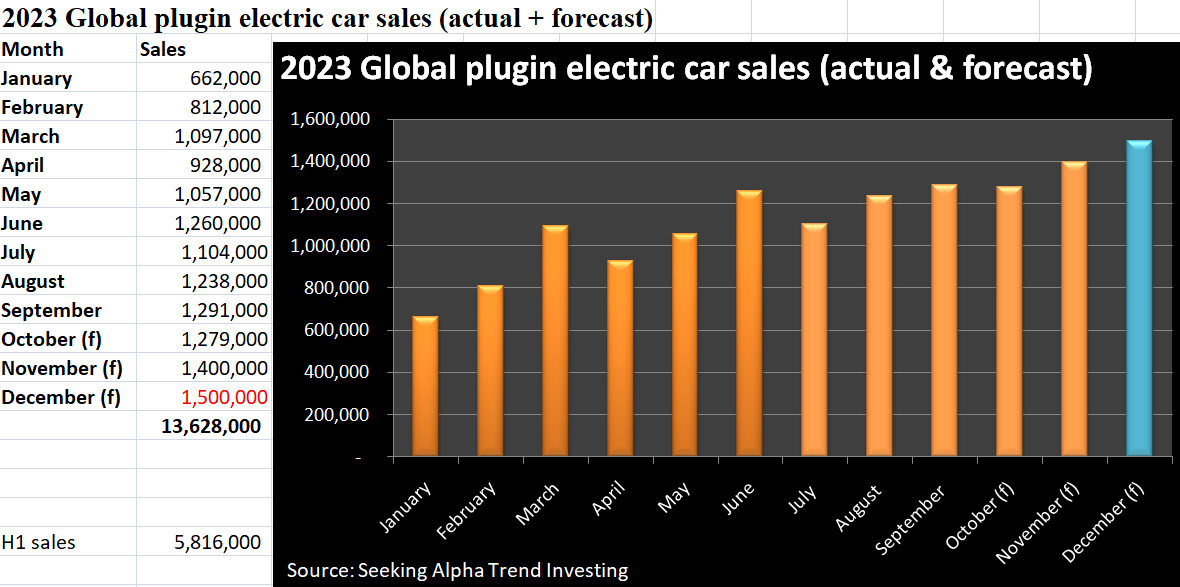

December 2023 saw the usual seasonal upswing in global plugin electric car sales reaching a record ~1.5 million. China led the way with a stellar result of 1.191 million units, up 46% YoY.

Global plugin electric car sales ended 2023 at 13.6 million units (~16% market share), for a growth rate of 31% YoY (a significant slowdown from the ~60% growth rate in 2022).

Trend Investing forecast for 2024 is 17 million units (20% market share), for a growth rate of 25% YoY.

BloombergNEF forecast for 2024 is 16.7 million units (~20% market share), for a growth rate of 21% YoY.

We are still at the very early stage of the EV boom.

Trend Investing’s global plugin electric car sales forecast to 2024 (green bars)

In early January, news was released that a record 1.2 million EVs were sold in the U.S. in 2023, according to estimates from Kelley Blue Book. The report noted that U.S. market share reached 7.6% in 2023 and that 55% of EV sales were attributable to Tesla (NASDAQ: TSLA).

The UK announced that their Zero Emission Vehicle (ZEV) mandate to increase electric car sales has become law. Key rules include:

“ZEV Mandate demands makers up share of electric car sales to 22% in 2024.

Electric vehicles currently make up around just 18% of all registrations in the UK.

Mandate thresholds rise annually to an 80% share in 2030 – and 100% by 2035.

Failure to meet the ZEV mandate sales targets can result in huge fines for auto makers of £15,000 per model below the required threshold.”

EV battery news

The U.S. government continues to tighten the screws towards developing their own EV supply chain independent of Foreign Entities Of Concern (“FEOC”). On January 20 Bloomberg reported: “US to ban Pentagon battery purchases from China’s CATL, BYD”. The ban will commence from October 2027 and include 4 other Chinese battery makers (Envision Energy Ltd., EVE Energy Co., Gotion High Tech Co., and Hithium Energy Storage Technology Co).

Global critical minerals update

There is an enormous amount of doom and gloom surrounding the EV and battery metals sector as we commence 2024. A key theme in recent months has been very depressed prices for many of the critical minerals, especially those related to the EV segment. A combination of the slowing EV growth rate in 2023 from ~60% in 2022 to ~31% in 2023, combined with an excess of battery inventory from 2022 and new EV metals supply has left most EV metal markets in surplus with prices collapsing.

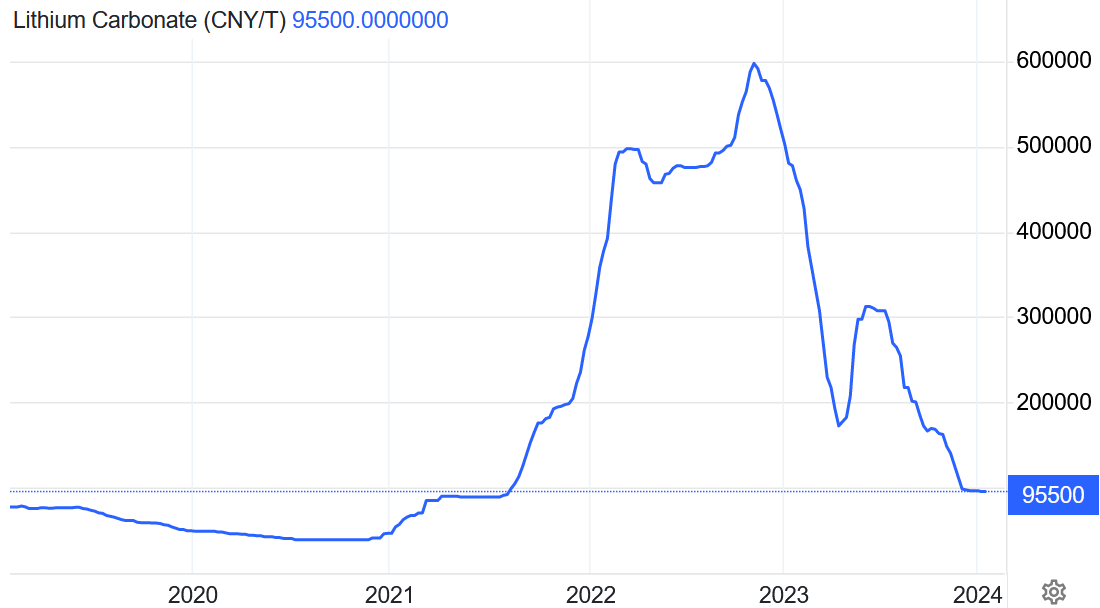

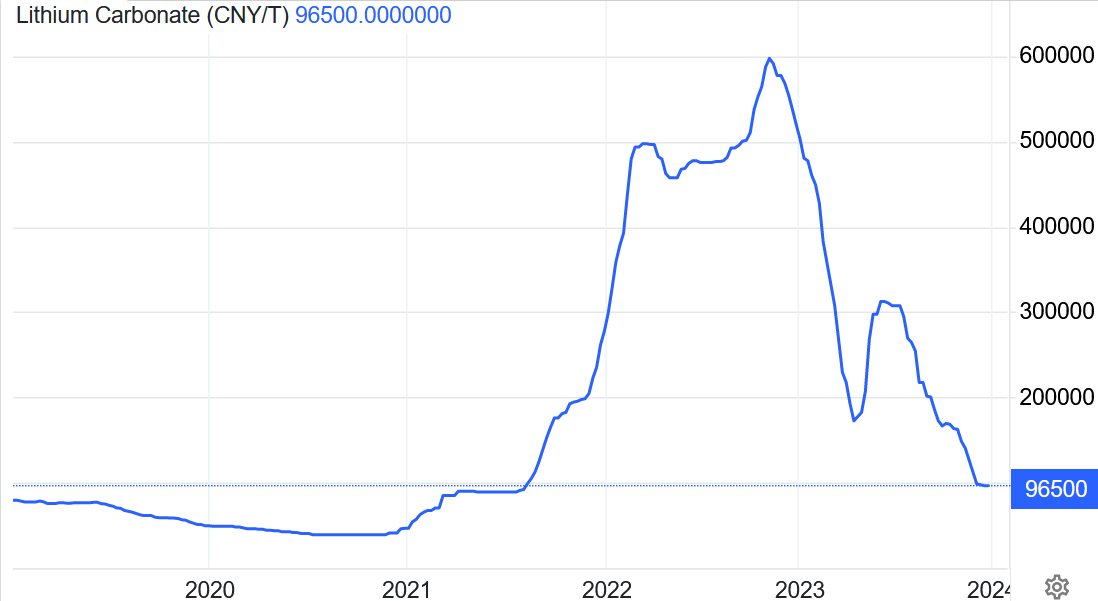

China lithium carbonate spot prices were flat the past month, with the price now at CNY 95,500/t (USD 13,275/t). After an ~80% fall from the high, lithium prices appear to have finally stabilized. This is logical given that prices are now at or below the marginal cost of production, especially for the higher cost China lepidolite producers.

Industry participants have been calling for a price bottom in recent months, with China Futures Co. analyst, Zhang Weixin, forecasting lithium prices to bottom out between CNY 80- 90,000/t and average CNY 100,000/t in 2024.

The other key recent trend in the lithium sector has been several announcements from lithium producers either stopping production or reducing their expansion plans. Core Lithium (ASX: CXO) announced on January 5, 2024 it will temporarily suspend mining operations. Then on January 17, 2024, Albemarle Corporation (NYSE: ALB) announced “actions to preserve growth, reduce costs, and optimize cash flow”. This includes deferring plans to build a fourth lithium hydroxide processing train at their Kemerton LiOH facility.

The China lithium carbonate spot price has stabilized near the marginal cost of production

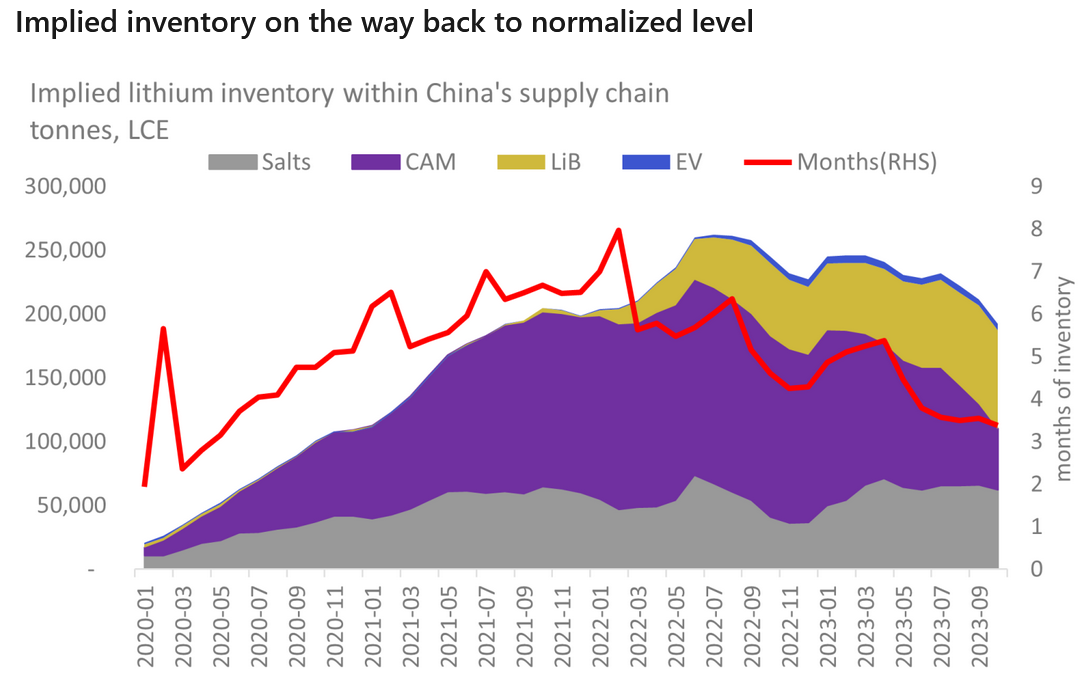

On the topic of when we might see some recovery in lithium prices. On January 19 Fastmarkets put out a report stating: “…We expect orders to start flowing upstream again either towards the end of the first quarter or early in the second quarter.” If this proves correct and EV demand remains solid, then we could expect some lithium price recovery late Q1, early Q2, 2024.

Fastmarkets reports China lithium inventory levels are now back to the pre-boom levels with ~3 months of supply (red line)

Neodymium spot prices fell again the past month to CNY 505,500/t. Prices peaked in February 2022 at CNY 1,506,530 and have been trending lower ever since then.

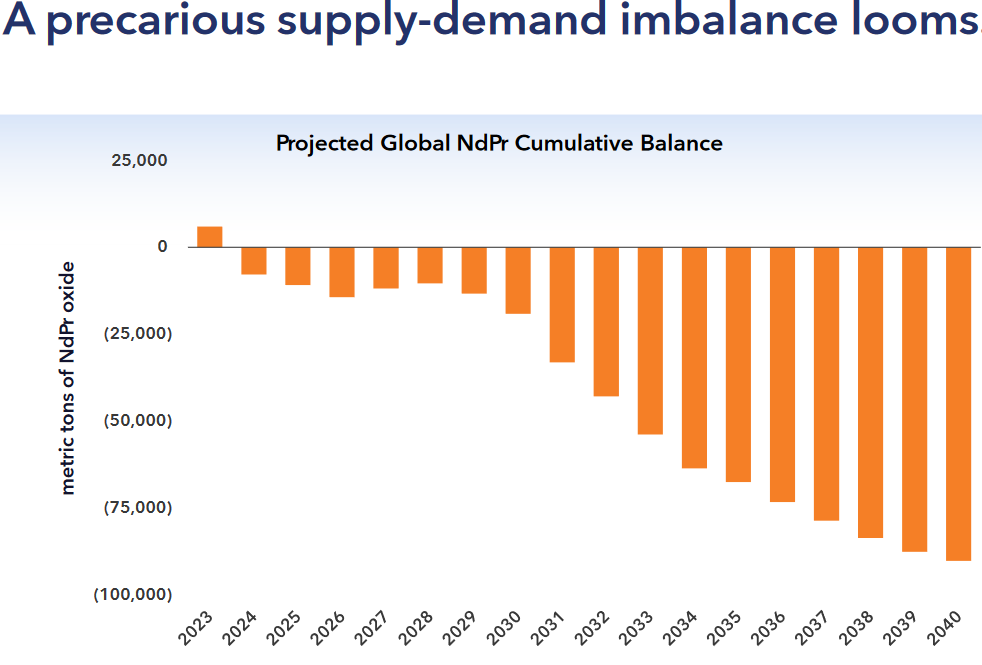

As discussed in a recent InvestorNews article, the consensus of industry experts is for 2024 to be a consolidation year. The article states: “2024 should see a year of consolidation for the rare earths sector as some experts are telling me. Some forecasts are for NdPr supply deficit to begin as early as 2024; however, this will largely depend on China demand, the global economy, EV sales, and new NdPr supply hitting the market.”

One interesting news item that emerged in January was of Rainbow Rare Earths Limited (LSE: RBW) (“Rainbow”) and their Phalaborwa Project in South Africa. The key aspect being that the Project consists of gypsum waste piles that contain large quantities of the magnet rare earths. Rainbow CEO Bennett stated: “We’ve got no mining cost, no crushing, no milling, no flotation. I saw the advantages to lead to a low capital intensity and low operating cost environment project.” Rainbow targets first production for 2026.

Some analysts are forecasting deficits ahead for NdPr rare earths driven by strong EV and wind energy demand

Cobalt, Graphite, Nickel, Manganese and other critical minerals

Cobalt prices (currently at US$12.90/lb) were flat the past month and remain at very depressed levels. The cobalt market is suffering from excess cobalt supply from the DRC which combined with a global slowdown in demand has led to cobalt prices dropping by almost 2/3 since their April 2022 peak. With LFP batteries gaining in popularity (no cobalt required) and a weak global consumer electronics market, there appears to be no short term turnaround for cobalt. Leading cobalt producer Glencore PLC (LSE: GLEN | OTC: GLCNF) has been stockpiling their excess material. At current prices, there is limited incentive for western producers to expand or enter the market.

Cobalt has lost two-thirds of its value since a recent peak in 2022

Flake graphite prices remain very weak with prices near the marginal cost of production and down ~2% over the past month.

A January 2024 Bloomberg report noted that natural flake graphite shipments slumped 91% in December from November 2023. Of course, sales surged prior to the Chinese export license permits being implemented in December 2023. December exports were 3,973 tons compared to the past monthly average of ~17,000t, so still a very significant fall.

Despite the spate of recent bad news, graphite is one of the EV metals with the largest demand profiles ahead this decade. Several groups are forecasting deficits ahead this decade starting from 2024/25 for the various types of graphite including flake, spherical, and synthetic. You can read more on the graphite outlook here.

Nickel prices fell again last month to USD 15,799/t. The 1 year outlook for nickel remains poor due to oversupply concerns from Indonesia. As a result of low nickel prices we saw the collapse of Panoramic Resources (ASX: PAN) in December and then on January 22, 2024, it was reported that BHP Group (ASX: BHP | NYSE: BHP) plans “to put parts of Kambalda nickel concentrator in Australia on care and maintenance” from mid-2024. This was caused by Wyloo Metals, which supplies ore to the plant, announcing a pause in mining operations due to low nickel prices.

Manganese prices were flat the past month and are now at CNY 29.25/MTU.

Uranium prices have been the exception to the rule the past year as they continue to rise, now at US$106/lb.

The biggest trend that looks to be emerging in Q1, 2024 for the EV metals sector is a negative supply response from producers. Producers are cutting CapEx, scaling back expansion, and in some cases reducing or stopping production. Expect to see a lot more of this in H1, 2024.

They say “the cure for low prices is low prices”. Well that’s exactly where we are now in the cycle. The next 3-6 months is likely to see the washout phase, where many miners collapse, reduce production or put their mine into care and maintenance. There is no point running a mine and selling a limited resource and making no profit. I will end with three well known sayings:

“Bear markets are the author of bull markets”

“Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.”

“You have suffered through the pain, now hang around for the gain.”

Given the EV metals markets have been in a bear market for the past 15-18 months the end is near, and we should expect some recovery during H2, 2024, assuming EV sales can grow at a reasonable rate.

The Critical Minerals Institute Report (12.27.2023): Politics Driving Marketable Commodities into 2024

written by Matt Bohlsen | March 6, 2024

Welcome to the December 2023 Critical Minerals Institute (“CMI”) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the CMI List of Critical Minerals or click here to visit the CMI Library.

Global macro view

December 2023 saw a further fall in U.S. inflation from 3.2%pa in October to 3.1%pa in November. As expected the U.S. Fed left interest rates unchanged at their December meeting. Even more significant was the Fed indicated that there are potentially ‘3 interest rate cuts coming’ in 2024. This was an early Christmas present for U.S. equity markets which continued their recent rally. Year to date, as of December 26, 2023, the S&P 500 is up 25.75% and the NASDAQ is up an amazing 43.25%. Of course, this follows heavy falls in 2022.

In late December China signaled a possible early 2024 interest rate cut when they reduced bank deposit rates. As a result China 30 year government bond yields hit their lowest level since 2005. All of this recent support for China’s economy and property market looks likely to set up a potential China recovery story in 2024. If China starts to recover in 2024 it would be a positive for commodity markets including the critical minerals.

The Russia-Ukraine war drags on through the European winter. There are some very early signs that both sides may be willing to end the war in 2024. We will see. Meanwhile, the Hamas-Israel war has been contained for now. We can only hope for peace in 2024.

Global plugin electric vehicle (“EV”) update

Global plugin electric car sales were 1,279,000 in October 2023 (the second-best month ever), up 37% YoY. November global sales reached 1.4 million. December should be even better. CPCA expects China’s NEV (New Energy Vehicle) retail sales in December 2023 to reach a record 940,000 units (41.4% market share), up 46.6% YoY. That should mean December global EV sales will be around 1.5 million.

This means that 2023 global plugin electric car sales should end up close to 13.6 million (~17% market share), for a growth rate of ~29% YoY (a significant slowdown from the 56% growth rate in 2022).

In other EV related news, in December Germany announced an abrupt ending to their EV subsidy. The subsidy was originally intended to apply until the end of 2024.

We also heard news that the U.S. is considering raising tariffs on Chinese EVs and Chinese solar products. The White House plans to complete a tariff review in early 2024. Chinese EVs entering the USA already have a 25% tariff. This follows the EU’s probe into China subsidies for EVs. All of this has come about due to the fact that about 60% of all global plugin EV sales are in China and the fact that China completely dominates the EV market and EV supply chain. This is now leading to a flood of compelling Chinese electric cars being exported to global markets where Western manufacturers (excluding Tesla Inc. (NASDAQ: TSLA)) are struggling to compete with China.

Finally, in December it was announced that Canada will require all new cars and trucks to be zero-emissions vehicles by 2035. The Canadian government stated: “The Standard will ensure that Canada can achieve a national target of 100 percent zero-emission vehicle sales by 2035. Interim targets of at least 20 percent of all sales by 2026, and at least 60 percent by 2030.”

Global critical minerals update

In December we got a key U.S. political announcement that will impact EV sales and critical minerals demand in 2024 and beyond.

U.S. Foreign Entity of Concern (“FEOC”) proposal

The U.S. DoE releases proposed interpretive guidance on Foreign Entity of Concern (“FEOC”) rules. FEOC’s include China, Russia, North Korea, and Iran. Key proposals include:

Beginning 2024, companies that have >25% ownership or control by a FEOC will not be eligible for tax credits available under the Inflation Reduction Act (IRA).

Beginning in 2024, an eligible clean vehicle (for IRA credits) may not contain any battery components that are manufactured or assembled by a FEOC.

Beginning in 2025, an eligible clean vehicle may not contain any critical minerals that were extracted, processed, or recycled by a FEOC.

These rules are quite strict and it is looking like the majority of EVs sold in the USA will not qualify in 2024 and hence not receive the subsidy of up to US$7,000 per vehicle. For example, the Tesla Model 3 and Model Y base range EVs use Chinese made LFP batteries, making them both ineligible to meet the FEOC rules. Things will only get harder in 2025. Of course, this is designed to motivate auto and battery OEMs to hurry up and build a new western battery supply chain, independent of FEOC.

The FEOC proposal follows last month’s news of new guidelines for the EU Critical Raw Materials Act (“CRMA”) as discussed here. A key ruling was that “not more than 65% of the Union’s consumption of each strategic raw material comes from a single third county.”

U.S. proposal to create a ‘Resilient Resource Reserve’ for key critical minerals

As reported in December, the U.S. select committee has recommended the creation of a critical mineral reserve to protect domestic industry. The Fastmarkets report stated:

“The adoption of such a reserve is intended to “insulate American producers from price volatility and (the People’s Republic of China’s) weaponization of its dominance in critical mineral supply chain. Such a reserve would be used to sustain the price of a critical mineral when prices fall below a certain threshold and would be replenished through contribution from companies when prices are “significantly” higher”…The fund would target critical metals where there is high price volatility, low US domestic production and import dependence on China. Cobalt, manganese, light and heavy rare earths, vanadium, gallium, graphite, germanium and boron are critical minerals that fall under that category, according to the report…”

Note: Bold emphasis by the author.

Lithium

China lithium carbonate spot prices fell again in December 2023, with the price now at CNY 96,500/t (USD 13,505/t) and down 82% over the past year. Prices are now below the marginal cost of production, meaning a bottom should be found very soon (assuming EV sales hold up in 2024).

Industry participants are increasingly calling a likely bottom. For example, China Futures Co. analyst, Zhang Weixin, forecasts China’s lithium carbonate spot to bottom out between CNY 80- 90,000/t (US$11,200-US$12,600/t). Goldman Sachs is a little more bearish with a 1 year price target for China’s spot lithium carbonate of US$11,000/t.

The negative price action has not deterred SQM and Gina Reinhart’s Hancock Prospecting (private) who recently increased their bid to A$3.70 per share to takeover Australia’s Azure Minerals Limited (ASX: AZS).

In December we saw shareholders approve the Allkem Limited (ASX: AKE | TSX: AKE) – Livent Corporation (NYSE: LTHM) ‘merger of equals’ which is now expected to close by January 4, 2024. The new company is to be known as Arcadian Lithium PLC (NYSE: ALTM | ASX: LTM).

Finally, in December we got news that free markets supporter Javei Milei was elected as the new Argentina President. This is good news for those companies with mining projects in Argentina, of which there are many lithium projects under development.

The lithium carbonate spot price collapsed in 2023 and is now below the marginal cost of production and expected to form a bottom very soon

Neodymium prices fell in December to CNY 560,000/t almost 1/3 the price of the February 2022 peak. The one year outlook remains quite weak; however, this will largely depend on how China’s economy performs in 2024. A strong pickup in EV sales in 2024 could quickly change the market dynamics.

The big news in December in the rare earths market this month was China’s announcement to ban the export of rare earth processing technology. As discussed in an InvestorNews article, Western companies have been efficiently separating rare earths for some time, so this ban has minimal implications. CMI Co-Chair and rare earths expert, Jack Lifton, states: “Solvent extraction separation is a long-established practice everywhere. The issue is the production of rare earth metals and alloys and from them of rare earth permanent magnets. This is where China’s massive lead in manufacturing technology may be insurmountable. Time will tell.”

Of course, the trend for Western auto OEMs is concerning, especially following China’s recent introduction of export license permits on graphite products (including synthetic graphite, flake graphite, and spherical graphite).

Cobalt, Graphite, Nickel, Manganese, and other critical minerals

Cobalt prices (currently at US$12.91/lb) were lower the past month and continue to be very depressed. China’s slowdown and the slowdown in global electronics sales have suppressed cobalt demand at the same time as new supply from the DRC and Indonesia has risen.

One glimmer of hope for the Western cobalt producers is that the U.S. government announced in December the creation of a critical mineral ‘Resilient Resource Reserve’ (as discussed above).

Flake graphiteprices also remain very weak with prices near the marginal cost of production. Following the introduction of Chinese export license permits in December 2023 there has been some increased signs of buying activity and a slight graphite price improvement. However, the main concern for flake and spherical graphite is that lower energy input costs in China have lowered the cost of producing synthetic graphite, thereby dampening demand for flake and spherical graphite. Despite this, there are several analysts now forecasting graphite deficits to begin as soon as 2024/25 as you can read in a recent InvestorNews article here.

Nickel prices fell slightly in December to US$16,279/t. The 1 year outlook for nickel remains poor due to oversupply concerns from Indonesia. A recovering global economy and Chinese property sector will be needed to help balance the nickel market, which is currently in oversupply.

Manganeseprices also fell slightly in December and are now at CNY29.20/MTU.

2023 has been a tough year for many critical mineral prices (except for gallium, germanium, tellurium, indium, tin, and uranium – a critical mineral in Canada) as a slowing China and global economy weighed down demand at a time where supply increased. Uranium was the standout performer in 2023 with a gain of over 75%. You can read an article here from back in April 2023 where we highlighted the coming rise of uranium.

The key to watch in 2024 will be if we see lower interest rates in China trigger a China property and economy recovery. A stronger U.S. and Europe in 2024 would also help boost the global economy and demand for critical minerals. Lower interest rates in 2024 could potentially make it a great year for the auto sector and EV metals.

Wishing you all a safe and prosperous 2024 from the Critical Mineral Institute (“CMI”).

The Critical Minerals Institute Report for September 2023

written by Matt Bohlsen | March 6, 2024

Welcome to the mid-September 2023 Critical Minerals Institute (“CMI”) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the IEA list of Critical Minerals.

Global critical minerals and electric vehicle (“EV”) update

Early September 2023 saw several major global events that impacted critical minerals.

The EU raised interest rates by 0.25% to a new 22 year high of 4.5%, signaling this may be the peak in rates. The US Fed is set to meet on September 20 with most analysts expecting a pause (at the current 5.5% rate, also a 22 year high), despite this week’s 3.7% CPI number, up from 3.2% the previous month. Rising interest rates in the West is slowing the economy which slows demand for most critical minerals. This has been a trend in 2023 with most critical minerals prices falling.

China announced a rate decrease last month and a decrease in the reserve rate ratio this week, all of which is starting to boost their sluggish economy. This is important as China is a key driver of critical mineral prices.

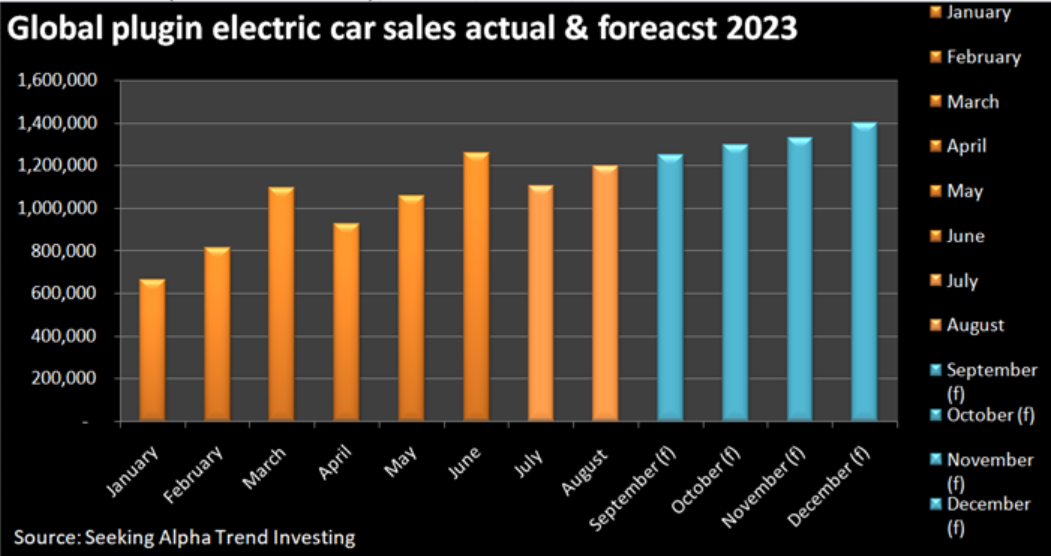

Global plugin electric car sales have generally been improving each month of 2023 after a slow start in Q1. Global EV sales reached 1.2 million units in August 2023, up 39% YoY, bringing YTD sales to 8.2 million. Sales in China have grown by 35% YTD, in EU and EFTA and UK by 30%, and in the US and Canada by 59%. 2023 sales look set to finish at ~13.5 million and 17% market share, which would be a 28% increase on 2022 (10.522 million and 13% market share). BYD Co. Ltd. (OTC: BYDDF) and Tesla Inc. (NASDAQ: TSLA) are dominating EV sales as you can read here in an article by CMI Director Matt Bohlsen.

Global plugin electric car ‘monthly’ sales in 2023 (source)

In mid-September we heard news that the Saudis and the US are in talks to secure critical metals in Africa needed to help the US with their energy transition. CMI Co-Chair Jack Lifton and CMI Director Melissa Sanderson shared their views on this controversial topic here. The Chinese have a long track record of mining in Africa, so it will be interesting to see what happens now they have sovereign wealth funds, such as that from Saudi Arabia, as competition. Glencore PLC (LSE: GLEN | OTC: GLCNF | HK: 805) has also increased its DRC activity with the recently announced backing of Tantalex Lithium Resources Corp.‘s (CSE: TTX | OTCQB: TTLXF) DRC lithium project.

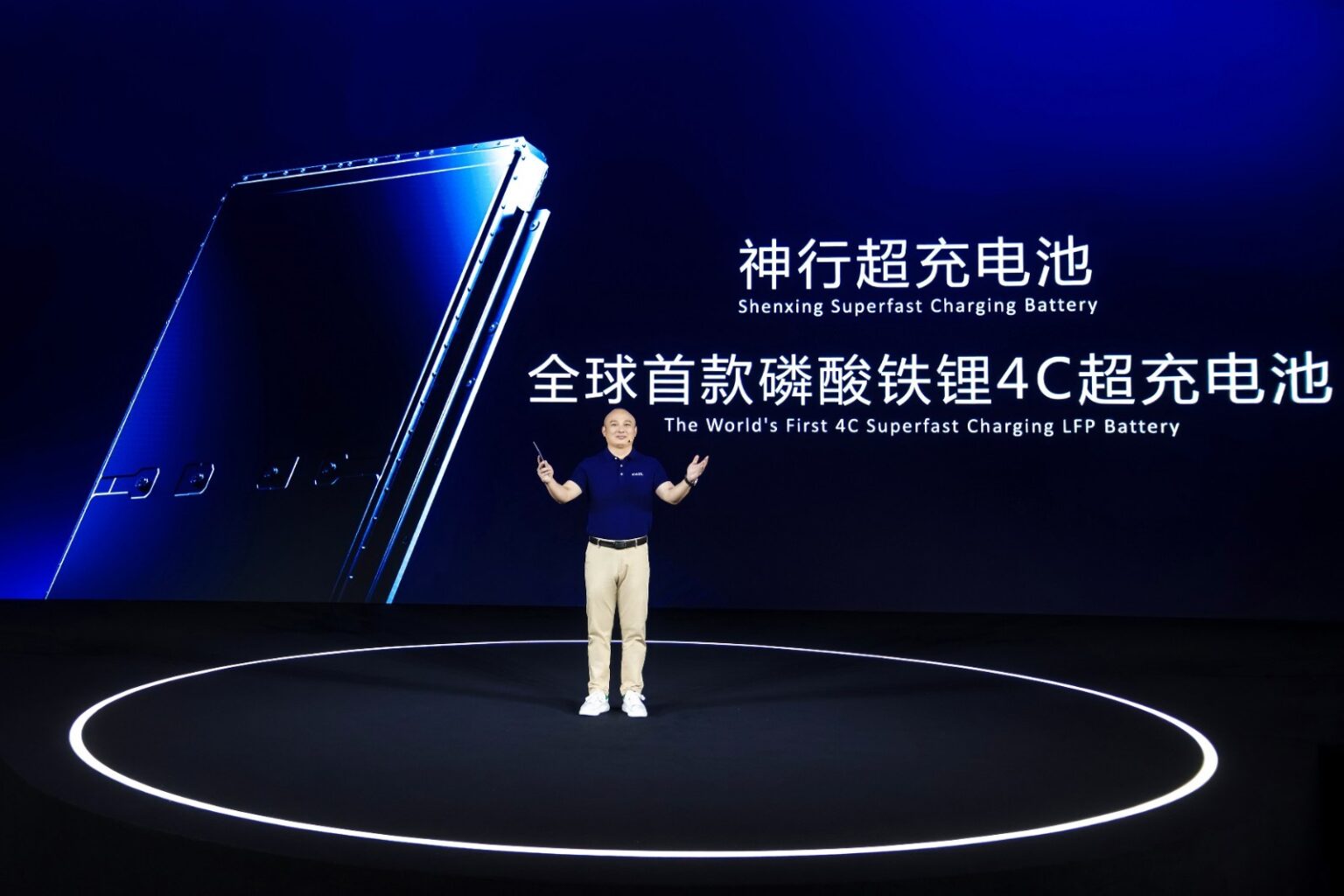

Battery news – CATL has a new superfast charging battery that can revolutionize fast charging

In some groundbreaking battery news, Contemporary Amperex Technology Co. (“CATL”) the world’s leading battery manufacturer, recently announced a new ‘superfast charging’ lithium iron phosphate (“LFP”) battery. It is reported that the new 80kWh battery, named Shenxing, is “capable of delivering 400 km of driving range with a 10-minute charge as well as a range of over 700 km on a single full charge.”

Now that’s impressive, especially given current batteries typically take about 3x longer to charge. It certainly has the potential to revolutionize fast charging speeds.

CATL has a new superfast charging LFP battery, named Shenxing (source)

Lithium

Lithium chemical spot prices fell so far in September 2023, with China lithium carbonate spot at CNY 186,500 (US$ 26,022). Prices now look to be close to reaching a bottom due to being close to the current marginal cost of production of ~US$ 25,000/t. News out of China has reported that some marginal lepidolite producers have recently been halting production.

The good news is that lower material prices have led to battery cell prices falling below the magical US$ 100/kWh for the first time in 2 years. At this price, electric cars potentially reach purchase price parity with internal combustion engines as we are now seeing in China, where almost 2 out of every 5 new cars purchased are EVs (July was 38% and 2023 YTD is 36% market share).

Of interest in September it was reported that the Australian Government said “tax breaks for lithium are ‘on the table’”. Australia is already the world’s largest supplier of lithium ore but has ambitions to grow its lithium chemicals production and to value add in other areas.

We also had a most interesting report that quotes leading lithium industry expert stating: “Mr Lithium says he’ll ‘be dead’ before the lithium market is oversupplied.”

September also saw an interesting report stating: “The world’s largest deposit of lithium may have been discovered inside a US supervolcano”. The report is referring to a study conducted by Lithium Americas Corp. (TSX: LAC | NYSE: LAC), which hypothesizes that the McDermitt Caldera contains 20 to 40 million metric tons of lithium.

Rare Earths

Neodymium (“Nd”) prices showed some strong recovery so far in September 2023 after a rough 2023 which has seen prices fall ~33% YTD. Most of the other rare earths prices have also been struggling in 2023, weighed down by a slowing China.

In an interesting rare earths September market update titled “The Chinese Rare Earths Monopoly Saga Continues”, leading global expert Jack Lifton stated: “China is doubling the size of its rare earth permanent magnet industry. It is said that this will happen by 2025. This means that China needs more, much more of the magnet precursor rare earths and all of the heavy rare earths, in particular, that it controls.”

The interesting part is that the West, boosted by the U.S Inflation Reduction Act (“IRA) and the EU Critical Raw Minerals Act (“CRMA”), is also working to rapidly build up their own supply chains of key critical metals, notably the magnet rare earths.

One such development in this direction is by Neo Performance Materials Inc. (TSX: NEO”) (“Neo”), who recently held their groundbreaking for a new permanent magnet plant in Estonia, Europe. The new plant targets Phase 1 production to reach 2,000/t pa in 2025, with Phase 2 targeting production of 5,000 tonnes/year (to support the manufacturing of ~4.5 million electric cars). The new plant will be fed by Neo’s rare earth oxide feed to come from Neo’s existing rare earth separations plant in Estonia. Another company Energy Fuels Inc. (NYSE American: UUUU | TSX: EFR) is also making great strides at developing a US supply chain for critical rare earths as you can read here. There are also several other junior rare earths companies, notably in Canada and Australia looking to supply the sector in future years.

Cobalt, Graphite, Nickel, Manganese and other critical minerals

Cobalt prices (currently at US$ 14.84/lb) continue to be very depressed in 2023, not helped by the slowdown in the global electronics sector. Some reports that China may be starting to pick up as well as some strength in superalloys (used in aerospace & military) demand gives a glimmer of hope.

Flake graphiteprices are also very weak with prices near the marginal cost of production. Flake graphite is forecast by Macquarie and others to start heading into deficit from about 2024. Leading western graphite producer Syrah Resources Limited (ASX: SYR) has been slowing production. Syrah announced in September that they had received a US$150 million conditional loan commitment for Balama approved by United States International Development Finance Corporation. The US government is supporting Syrah as they are well advanced towards construction of an active anode materials (spherical graphite) plant in the USA, which happens to have an off-take deal with Tesla (NASDAQ: TSLA).

Nickelprices have remained quite strong the past 3 years; however, oversupply concerns from Indonesia and a slowing Chinese economy have taken their toll in 2023. A pickup in China stainless steel demand will be key to watch out for.

Manganeseprices continue to be weighed down by weak Chinese demand as the Chinese housing industry continues to rebalance after years of over construction and oversupply. On the positive side manganese is starting to be used in lithium manganese iron phosphate (“LMFP”) batteries, by both Gotion Hi-Tech and CATL’s Qilin battery.

Special Thanks to the Editor of The Critical Minerals InstituteMonthly Report, Matt Bohlsen who is a CMI Director.

About the Critical Minerals Institute: The Critical Mineral Institute (CMI) is an international organization for companies and professionals focused on battery materials, technology metals, defense metals, ESG technologies and practices, the general EV market, and the use of critical minerals for energy and alternative energy production. Offering an online site that features job opportunities that range from consulting roles to Advisory Board positions, the CMI offers a wide range of B2B service solutions. Also offering online and in-person events, the CMI is designed for education, collaboration, and to provide professional opportunities to meet the critical minerals supply chain challenges.

————————

The Critical Minerals Institute was created to offer education, collaboration, and an online resource to learn about critical mineral projects, emerging technologies, legislative initiatives, government funding, human capital needs, and capital market investment opportunities. There is no charge or sign up required for access to the Critical Minerals Institute website: www.criticalmineralsinstitute.com. A range of enhanced benefits are available to individual and corporate members of the CMI, including attendance at the CMI Summit, virtual events and additional resources. For details see: www.criticalmineralsinstitute.com/cmi-membership/.

Elcora Ramps Up Manganese Sales with Vanadium Prospects on the Near-Term Horizon

written by InvestorNews | March 6, 2024

Elcora Advanced Materials Corp. (TSXV: ERA) (“Elcora”) is a relatively new manganese ore producer and has other battery material projects containing vanadium, graphite, and copper located in Morocco and Canada. Elcora also has exposure to anode materials and graphene. Demand for manganese remains strong both for the steel industry, but also for lithium-ion batteries containing manganese, typically used for electric vehicles.

Elcora’s goal is to be a globally competitive extractor and processor of battery-grade minerals and metals. They plan to do this by becoming a vertically integrated battery materials company and use their cost-effective process to purify high-quality battery metals and minerals that are commercially scalable.

How Elcora is anticipating and responding to the Global Energy Revolution

Manganese production has started in Morocco and new orders are rolling in

As announced in June 2023, Elcora delivered its first manganese order of 500 metric tons of 37%+ high-quality manganese from their Morocco Mine. Elcora owns theAtlas Fox Project in Morocco, which includes the Beni Mellal Manganese Deposit/Mine and the Ouarzazate Project (includes the Omar Mine). Elcora plans to rapidly ramp up their manganese production from these projects with an 8-12 month production target of 20,000 tonnes per month of 37% manganese ore.

As announced on July 6, 2023, Elcora has secured two more orders for a total of 1,500 metric tons of 37%+ manganese ore set to be delivered by the end of July 2023, thereby securing sales revenue for the second month in a row for Elcora.

Vanadium production plans with sales potentially as soon as only 6 months away

Elcora is currently developing their Atlas Lion Vanadium Project in Morocco.

Elcora announced in June 2023 the completion of the first phase of vanadinite comminution testing. The result was 8.9% vanadium concentrate. Elcora then began shipping bulk samples for trial tests in smelters in Asia and Europe, and if results come back positive Elcora say they could potentially have concentrate sales revenue in as quick as 6 months.

The short-term plan is to build a semi-mobile concentrator plant to produce a 46% lead (“Pb”) and 9%+ vanadium (“V”) concentrate, with a ramp up to 2,500t/month of concentrate production. Elcora’s mid-term plan is to build a hydrometallurgical plant scheduled to produce 1,500 t/year of 99.99% V and 15,000t/year 99.99% Pb.

Elcora’s graphite products

In addition to manganese, vanadium and lead; Elcora has developed the technology to produce flake graphite, advanced natural graphite anode powder and graphene. Elcora states:

“Elcora has developed a unique low-cost effective process to make commercially scalable graphite nanomaterials ranging from micro-graphite to graphene.”

Flake graphite and anode powder are in growing demand for electric vehicles and energy stationary storage where the graphite is used in the anode part of the battery. Graphene has numerous potential uses and is known as a new wonder material.

“Elcora has been structured to become a vertically integrated graphite & graphene company that mines, processes, refines graphite, and produces both the graphene and end graphene applications. Elcora’s graphene production system is suitable for use with many different graphite sources and has produced industry-leading quality graphene.“

Closing remarks

Elcora is executing well on their plans to become a vertically integrated battery materials company. Elcora already has a strong history within the flake graphite, anode powder, and graphene sectors.

Near-term catalysts will be further sales revenue of manganese concentrate from their Moroccan Mine and potentially good news on their vanadium concentrate smelting trials. Looking out a year or so from now Elcora should potentially have ramped up their vanadium concentrate production to 20,000t/month and vanadium concentrate to 2,500t/month. Beyond that, the plan is to potentially produce a final product via more processing thereby value adding to their current situation.

Elcora Advanced Materials trades on a market cap of only C$6 million. Exciting times for Elcora, especially if they can continue to execute well and bring in growing revenues in 2023.

Focused on becoming a battery material supplier, Elcora sells first manganese order and prepares vanadium assets

written by InvestorNews | March 6, 2024

During an interview between Troy Grant, Founder, CEO and Director of Elcora Advanced Materials Corp. (TSXV: ERA), and Tracy Weslosky from InvestorIntel, several key points were discussed surrounding Elcora’s manganese and vanadium milestones towards production. Troy confirmed that Elcora is currently selling manganese and has successfully shipped trial shipments to two customers. Preparing for shipments to four additional customers, Elcora’s ultimate goal is to become a fully vertically integrated battery material supplier.

Troy emphasized the importance of their manganese assets in Morocco and their aim to generate cash flow from them. The demand for manganese is strong, and they are focused on meeting that demand as quickly as possible. He explained that the percentage of manganese in the product determines its pricing, with higher percentages commanding higher prices. Elcora’s target is to build a production plant capable of producing 20,000 tons of manganese per month. They estimate that it will take 8 to 12 months to reach this level of production.

The discussion also touched upon Elcora’s vanadium production. Troy mentioned that they have been working with Dr. Ian Flint to complete a preliminary assessment on their vanadium assets in Morocco. The initial test results for their vanadium concentrate product are positive, and they are currently testing it with smelters in Europe and Asia. If the results are encouraging, they could start generating cash flow from vanadium production within six months.

Troy expressed optimism about the future, stating that they expect encouraging news regarding vanadium production and the commissioning of the manganese production plant in the next quarter. Overall, Troy’s update showcased Elcora’s progress and their focus on meeting the demand for manganese and exploring the potential of vanadium production for the Company.

To access the full InvestorIntel interview, click here

Don’t miss other InvestorIntel interviews. Subscribe to the InvestorIntel YouTube channel by clicking here.

About Elcora Advanced Materials Corp.

Elcora was founded in 2011 and has been structured to become a vertically integrated battery material company. Elcora can process, refine, and produce battery related minerals and metals. As part of the vertical integration strategy Elcora has developed a cost-effective process to purify high-quality battery metals and minerals that are commercially scalable. This combination means that Elcora has the tools and resources for vertical integration of the battery minerals and metals industry.

To know more about Elcora Advanced Materials Corp., click here

Disclaimer: Elcora Advanced Materials Corp. is an advertorial member of InvestorIntel Corp.

This interview, which was produced by InvestorIntel Corp. (IIC) does not contain, nor does it purport to contain, a summary of all the material information concerning the “Company” being interviewed. IIC offers no representations or warranties that any of the information contained in this interview is accurate or complete.

This presentation may contain“forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein.

Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Prospective investors are urged to review the Company’s profile on Sedar.com and to carry out independent investigations in order to determine their interest in investing in the Company.

If you have any questions surrounding the content of this interview, please contact us at +1 416 792 8228 and/or email us direct at [email protected].

Elcora order is just the beginning of its journey in the manganese market

written by InvestorNews | March 6, 2024

Manganese is becoming a key part of the lithium-ion battery market, traditionally used in nickel, manganese, cobalt (“NCM”) batteries; but now it is also used in lithium manganese iron phosphate (“LMFP”) batteries. This new battery type offers greater energy density (and hence EV range) than the standard LFP battery. Manganese is still largely used in steel, but the battery demand looks set to grow much faster. Overall the global manganese market is expected to grow at a CAGR of 5.5% from 2023 to 2027.

LMFP batteries containing manganese are the latest development to improve lithium-ion batteries

As announced last month Gotion High-tech Co Ltd. (SHE: 002074) has developed a breakthrough LMFP battery that offers a “range of up to 1,000kms for a single charge and could last two million kms”. Their new battery pack will go into mass production in 2024.

In 2022 it was reported that “CATL will soon mass produce LMFP batteries”. Contemporary Amperex Technology Co., Limited (SHE: 300750) (“CATL”) is the world’s largest lithium-ion battery manufacturer by far with 37% market share and is a leading supplier of Tesla Inc. (NASDAQ: TSLA). At Tesla Battery Day in 2020, Elon Musk pointed out that Tesla targets to use manganese in its batteries for long-range electric cars.

At Tesla Battery Day 2020, Tesla targets to use nickel and ‘manganese’ batteries for long range vehicles where vehiclemass is not too large

Note: Red oval done by the author to highlight manganese

Today’s company made a key announcement this week regarding commencement of manganese ore sales.

Elcora Advanced Materials Corp.

Elcora Advanced Materials Corp. (TSXV: ERA | OTCQB: ECORF) (“Elcora”) is working towards becoming a vertically integrated battery material company. Elcora has developed a cost-effective process to purify high-quality battery metals and minerals that are commercially scalable.

Elcora’s key projects have graphite, manganese, and vanadium. Elcora also has exposure to anode materials and graphene.

“has received its first monthly order for 1000 metric tons of 37% + manganese ore. The delivery of the first part of the order is scheduled before the end of June 2023. The order was placed by a leading European customer looking for a long-term supply relationship and marks a significant milestone for Elcora’s mining division.“

The order is not large but it marks the beginning of what can be a good business for Elcora if they can achieve large-scale production. Manganese ore (37% Mn grade) currently trades at about US$3.13/ dmtu (Dry Metric Tonne Unit) FOB Port Elizabeth.

“The recurrence of orders is expected to generate significant revenue for Elcora Advanced Materials Corp, further strengthening its position in the industry. With the increasing demand for manganese ore, the company is well-positioned to meet the needs of its customers...Elcora Advanced Materials Corp is well-positioned to benefit from this growing demand, and this order is just the beginning of its journey in the manganese market.”

Elcora’s Atlas Fox Project in Morocco – Beni Mellal Manganese Deposit/Mine and the Ouarzazate Project (including the Omar Mine)

Elcora’s Atlas Fox Project in Morocco is rich in manganese. It is comprised of the Beni Mellal Manganese Deposit/Mine and the Ouarzazate Project (including the Omar Mine).

At the Beni Mellal concessions, Elcora has a 10-year Exploitation License. This manganese concession contains a surface deposit mine that operated during French colonial times. Elcora plans to leverage on-site infrastructure with ore ready for processing. In Q4 2023 Elcora plan to build a gravimetric concentrator to upgrade raw ore content (30% Mn) to 50% Mn and increase mine production to 2,500 to 3,000 t/month of 50% Mn concentrate.

At the Ouarzazate Project Omar Mine, Elcora has acquired exclusive mining rights and an option to purchase the 16 km² manganese mining concession. The concession contains both a surface deposit and underground mine. Elcora is leveraging on-site infrastructure and has existing manganese ore piles of approximately 6,000 tonnes that are ready for processing. Elcora plans to ramp up mining production to 2,500 tons per month at the Omar Mine.

Elcora’s overall manganese ore production capacity is targeted to be more than 5,000 metric tonnes per month from the above concessions.

Atlas Lion Vanadium Project in Morocco

Elcora owns the Atlas Lion Vanadium Project (304 Km2) concessions in Morocco. Elcora plans to further explore and develop these concessions with the goal of producing vanadium.

Elcora’s next steps for mining manganese and vanadium in Morocco

In total, Elcora currently owns seventeen polymetallic (vanadium, lead, other), one manganese (and one option to purchase) and one copper licences/concessions in Morocco.

Elcora is making strong progress on its goal to become an integrated battery metals producer. The Company already has the technology and facilities to purify high-quality battery metals (notably spherical graphite, graphene, and anode powder) and is now working on the mining side with manganese and vanadium (noting they already have a graphite mine). The Atlas Fox Projectin Morocco has commenced stockpiled manganese ore sales and plans to ramp up manganese ore production from its concessions to 5,000/t per month. Following this will be development work and potentially production from the Atlas Lion Vanadium Project, also in Morocco.

Elcora Advanced Materials Corp. trades on a market cap of only C$18 million, suggesting this may potentially be just the beginning for Elcora.

The critical task of the Three Amigos

written by Stephen Lautens | March 6, 2024

The “Three Amigos” summit underway this week has a lot on the table for the leaders of the US, Canada, and Mexico to discuss. There are pressing issues on the agenda for US President Biden, Canadian Prime Minister Trudeau and Mexican President Obrador, such as migration and immigration, North American economic integration, climate change and cooperation in clean energy technologies, and Mexico’s efforts to shut others out of investment in its energy sector.

Even before they met, all three countries announced their ongoing commitment to work together on key sectors, including critical minerals and supply chains. According to reports, “while no financial commitments have been announced yet, those agreements include a cabinet-level summit on semiconductors, mapping mineral resources across the North American continent and promoting educational investment.”

Canada and the US have already announced their own commitments to developing and securing a domestic critical minerals supply chain. President Biden issued a directive in March 2022 invoking the Defense Production Act to incentivize the mining and domestic production of the critical minerals needed to manufacture batteries for electric vehicles and long-term energy storage. The US DoE awarded US$2.8 billion of grants in October, 2022, to accelerate US manufacturing of batteries for electric vehicles and the electric grid. In the 2022 Federal Canadian Budget, the government allocated an additional C$3.8 billion for critical minerals, including those that feed into clean technologies.

Besides Mexico and Canada, the US lists about a dozen countries as strategic partners for “supply chain resilience”. Mexico and Canada are the only ones that share a border with the US, with Canada being the US’s largest trade partner with US$664.8 billion in trade in 2021, and Mexico close behind as the US’s second largest trade partner with US$661.2 billion in trade. In 2021 China came third with US$657.4 billion in trade with the US.

The Biden vision at the Three Amigos summit is for a more integrated North America supply chain, with the US naturally seeing themselves in the driver’s seat. Canada and Mexico have slightly different views, but do agree on greater, mutually beneficial co-operation as long as the Biden administration’s continuation of the “Buy American” policy doesn’t leave them out in the cold.

Canada has been rapidly developing its own critical minerals and rare earths resources, which leaves the question of what Mexico brings to this particular table.

When people think about Mexico most think about copper and silver, with precious metals accounting for about half of Mexico’s production. Mexico’s metals sector, which in 2020 generated more than US$18 billion in exports and contributed around 8% of its gross domestic product.

As far back as 2014 Mexico’s largest mining company, Grupo Mexico, announced its intention to diversify into rare earth metals business, however there has been little progress to date. At present, of the four critical minerals that the US lists for the high-capacity battery sector (nickel, cobalt, lithium, and manganese) Mexico only produces manganese, and that in relatively small quantities.

The Mexican states of Sonora, Chihuahua, Oaxaca and Chiapas are recognized to have large, undeveloped deposits of rare earths. The U.S. Geological Survey (USGS) has also identified 1.7 million tons of lithium deposits in Mexico, making it potentially the 10th largest source in the world. However, the Mexican lithium deposits are largely held in clay substrates that are not accessible with current technology, and for the time being will remain in the ground.

That leaves Mexico’s development of its lithium resources lagging well behind other Latin American countries like Argentina or Chile. To further stymie development, in April 2022, Mexico passed legislation to ban private and non-Mexican lithium mining and processing activities and restrict all future projects to state-run companies. Mexico’s current president has pledged to honor existing lithium concessions, but has clearly declared not just a “Mexico First”, but a “Mexico Only” policy in the sector. Unfortunately, the government’s strategy so far has consisted only of the creation of a state-owned company, which has left development in a standstill.

As a rare earths, and particularly lithium, producer, it will be a long time before Mexico is able to contribute to the North American critical minerals supply chain. Not only is it starting from a standing stop, its mineralogical separation challenges are substantial and the current Obrador government is determined to not allow foreign companies and therefore foreign capital to develop any lithium assets in the country.

On top of these mineral development issues, Mexico has other challenges, including widespread organized criminal activity, corruption, civil unrest, and contract risks arising out of the current nationalist climate of Mexican president Andres Manuel Lopez Obrador.

In the near future, it appears that Mexico will continue to assemble electric cars, but not provide the materials for many of the key components required for a greener future. And it is unlikely that any amount of photo ops by the Three Amigos will fix this anytime soon.

Elcora Advanced Materials Prepares for Manganese Production in Morocco

written by InvestorNews | March 6, 2024

In this InvestorIntel interview, Tracy Weslosky secures an update on battery material and graphite technology company Elcora Advanced Materials Corp. (TSXV: ERA | OTCQB: ECORF). Starting with an update on the Atlas Fox Deposit, Founder, CEO and Director Troy Grant explains that as soon as the production license for this manganese project in Morocco is received production will begin immediately.

Explaining how manganese production may commence by the end of the year, Troy discusses the timeline as it relates to revenue for Elcora. Additional discussions include the general critical minerals market, and how the Company intends to use the recently closed private placement proceeds. Troy updates the InvestorIntel.com audience with a further update on the objective to initiate the ore production on the Vanadinite (Vanadium and Lead) concessions as soon as the Exploitation licenses have been granted.

To access the full InvestorIntel interview, click here

Don’t miss other InvestorIntel interviews. Subscribe to the InvestorIntel YouTube channel by clicking here.

About Elcora Advanced Materials Corp.

Elcora was founded in 2011 and has been structured to become a vertically integrated battery material company. Elcora can process, refine, and produce battery related minerals and metals. As part of the vertical integration strategy Elcora has developed a cost-effective process to purify high-quality battery metals and minerals that are commercially scalable. This combination means that Elcora has the tools and resources for vertical integration of the battery minerals and metals industry.

To know more about Elcora Advanced Materials Corp., click here

Disclaimer: Elcora Advanced Materials Corp. is an advertorial member of InvestorIntel Corp.

This interview, which was produced by InvestorIntel Corp. (IIC) does not contain, nor does it purport to contain, a summary of all the material information concerning the “Company” being interviewed. IIC offers no representations or warranties that any of the information contained in this interview is accurate or complete.

This presentation may contain“forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein.

Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Prospective investors are urged to review the Company’s profile on Sedar.com and to carry out independent investigations in order to determine their interest in investing in the Company.

If you have any questions surrounding the content of this interview, please contact us at +1 416 792 8228 and/or email us direct at [email protected].

The Dean’s List – Part 5: Which manganese companies could benefit from Canada’s commitment to critical minerals?

On top of all this, there was some big news out of the U.S. last week that could also have a trickle-down effect on Canadian miners – the passing of the Inflation Reduction Act, a Bill that includes requirements for domestic manufacturing of EVs and their battery components to qualify for tax credits. It requires that 40% of battery components be sourced from factories in the U.S. or its free trade agreement partners (like Canada). It also states that Chinese components and minerals be phased out beginning in 2024. It seems logical to continue our critical minerals focus on battery materials for now given all the recent announcements, so we’ll keep our focus on this particular aspect of the great energy transition.

We have so far discussed lithium & rare earths, nickel, graphite, and copper which leads us to today’s material – manganese. The cells in the average battery with a 60 kilowatt-hour (kWh) capacity—the same size that’s used in a Chevy Bolt—contained roughly 185 kilograms of minerals. NMC batteries, which accounted for 72% of batteries used in EVs in 2020 (excluding China), have a cathode composed of nickel, manganese, and cobalt along with lithium. Here’s how the mineral contents differ for various battery chemistries with a 60kWh capacity:

You might look at this and think “What’s the big deal?”, manganese is pretty much the smallest component. However, the devil is in the details. Guess how many manganese mines there are currently in North America? If you guessed anything more than zero, you’d be wrong. Not only that, High Purity Manganese Sulphate Monohydrate (HPMSM) is the highest purity “battery grade” manganese sulphate and is the manganese chemical used in a NMC cathode of a lithium-ion battery. There is currently no western hemisphere producer, and in particular no North American producer, of HPMSM. As you can probably guess, approximately 90% of current production of HPMSM is based in China. I think my decade old Christmas wish for an Aston Martin One-77 is more realistic than some of the commodities on the critical minerals list, but I digress.

But what if there were two companies that had the potential to be the first (and thus only) manganese producers in North America. That’s right, today is a bonus edition with two companies for the price of one given their assets are literally beside each other. I suspect they’d be pretty popular with all the EV battery plant manufacturers noted above, as well as any politician that could somehow attach their name to the support of one or both companies.

The first is Canadian Manganese Company Inc. (NEO: CDMN), who is focused on the exploration and development of its wholly owned manganese project located in Woodstock, New Brunswick, Canada (“Woodstock Project”). The Woodstock Project contains the largest, highest grade manganese carbonate deposit for development in North America. It is strategically located adjacent to the U.S. border, and within close proximity to both the St. Lawrence Seaway and Atlantic Ocean, ideally positioned to support the domestic lithium-ion battery supply chain for generations.

The second, Manganese X Energy Corp. (TSXV: MN | OTCQB: MNXXF) is advancing its Battery Hill manganese project, directly North of the Woodstock Project. It encompasses all or parts of five manganese-iron zones including Iron Ore Hill, Moody Hill, Sharpe Farm, Maple Hill and Wakefield.

In his Master’s Thesis on the Woodstock area manganese occurrences, Brian Way (2012) reports that the area “hosts a series of banded iron formations that collectively constitute one of the largest manganese resources in North America, approximately 194,000,000 tonnes”. It appears that someone from both these companies read this Master’s Thesis. Perhaps several EV battery plant companies will also search out this document as well.

As for who is in the driver’s seat of the two, Manganese X has recently reported a PEA on the Battery Hill project with highlights including: after-tax NPV10 of US$486 million; CAPEX of US$350 million with a payback of 2.8 years and life of mine operating cost of US$122/t material processed. While Canadian Manganese is only at the PFS stage. To date, both companies have comparable total tonnage, albeit Canadian Manganese is only inferred while Manganese X has a measured plus indicated number due to the extra work done to complete the PEA. Canadian Manganese appears to have better grades of Mn at approximately 10.0% versus 6.4% for Manganese X.

Both have roughly C$4 million of cash at present with market caps of C$25 million for Canadian Manganese and C$36 million for Manganese X. So if you want exposure to the manganese component of the North American critical minerals supply chain your choices appear to be somewhat limited, because it’s a pretty small field.