The twenty-first century began with an unprecedented (outside of war) mammoth growth of demand for the ores of the structural metals (a/k/a base metals, such as iron, aluminum, copper and the alloying elements for steels). Brazilian, Australian, and Indian iron ore miners whose American, Japanese, and European markets had matured were thrilled. Chile, Jamaica, Africa, and Polynesia prospered. China, the source of the new demand, just grew and grew into the world’s newest manufacturing center.

The ironically named “progressives” of the West are those who think that progress is attainable only under a benevolent central government run by elites dedicated to prosperity for all. Of course, this definition makes the logical error of self-reference, progress is whatever the progressives say it is. The simple fact that progress, defined as an uplifting of all, is only possible through wealth creation and its wide distribution and that, by far, the best system for doing this, so far created, has been free market capitalism, has been rejected by the self-serving “elites” who today hold elective office and control the permanent civil services of the West.

The fact that today’s Western elites consider only themselves, their narrow clique, worthy of defining, being the beneficiaries of, and promoting progress has not escaped the attention of the 90% of the world that does not live in the United States or Europe.

In the nineteenth and twentieth centuries, the use of military power by European states was after the World Wars followed by the economic domination of the United States to continue to guarantee the flow of cheap mineral resources to the self-serving progressive fantasists of the West. That era is closing. The revolt against their exclusion, first by the Germans and the Japanese, was to mimic the imperial style of Britain and France. This failed in both instances as did the similar Russian (Soviet) attempt, but they bought the United States a century of world domination. This era is now closing as the progressive fantasists have destroyed its ability to create and fairly distribute wealth.

For the last generation the financializers who replaced the engineers as CEOs of American and European OEMs have moved the majority of manufacturing off-shore and witlessly (not unwittingly) caused the metals processing and fabricating industries to relocate closer to their raw material sourcing and new end-users. This second move, of the minerals and metals processing industry, perhaps even more than the move of the OEMs, was an unintended gift to a China that no one foresaw as a global industrial powerhouse aborning.

The perspective of necessary time must be examined to understand the deleterious effect of Western financialization on commodity production and pricing. There is an excellent example of this in the attempt to “reshore” a total rare earth permanent magnet supply chain.

The massive Chinese dominance in the total supply chain to produce rare earth permanent magnets did not occur overnight, and it will not and cannot be rectified (in the sense of being made irrelevant) in any short period of time. By which I mean years. In fact, China controls the market for rare earth permanent magnets, because it first built or acquired control over the overwhelming majority of rare earth minerals on this planet. This occurred simultaneously with the West giving over to China the technology to separate the mixed rare earths extracted from the ore into individual rare earth compounds. This was followed by the technology to make rare earth metals, alloys, and permanent magnets. This overall agenda, supported by the building, in China, of a strong and focused educational system to support a world-class technologically advanced nation, has established in China a, long-term, holistic approach to acquiring, developing, supporting the mass production of, and deploying state-of-the-art technology to its people for the last 25 years. What does this mean for the West?

An example of the approach taken by America, the former leader, in technology and its deployment is illustrative: There are two separate domestic (North) American markets for rare earth permanent magnet (REPM) enabled devices; the military and the civilian. Dishonest attempts at promoting and marketing rare earth projects to investors have confused not only the low information “journalists” who cover this story but also the self-designated rare earth experts, in particular the ones who refer to their work as “intelligence.”

The military “need’ for REPMs can be defined very simply. The lighter the weight of the components of a weapons system the larger can be the weight of the explosives in the weapons. Rare earth permanent magnet motors (REPMMs), are also, by weight, the most efficient converters of electricity to mechanical motion of all types of electric motors. Thus a warship whose propeller shaft is the rotor of a large electric motor is easier to maintain than one that is the end of a gear train from an immense diesel engine. Better to use the diesel engine to generate the electricity for the drive motor and have (lithium-ion) batteries for backup during diesel engine service or in case of breakdowns. And what about those electromagnetic catapults on an aircraft carrier? REPMMs are a lot easier to maintain than AC motors and a battery backup can save an expensive aircraft and its pilot’s life in an emergency where the electricity supply from the reactor/generator is interrupted. And the fin actuators on a “smart” bomb… The actual demand for REPMMs by the U.S. military is classified, but in 2013 it wasn’t, and the number bandied about then was 1000 mt/year. The coming into service of new stealth fighters and direct electric propulsion ships and electromagnetic catapults since then has surely increased the demand for REPMMs by the military. Let’s say then that it must be 3000 tpa by now. Oh, and I forgot to mention all of these active military uses for REPMMs in extreme conditions mean that they run hot. This means they must be of the type that uses the very rare rare earths, dysprosium and terbium, as well as the even rarer metal, gallium, in their construction. As of this writing 100 percent of the world’s supply of Dy and Tb is processed in China.

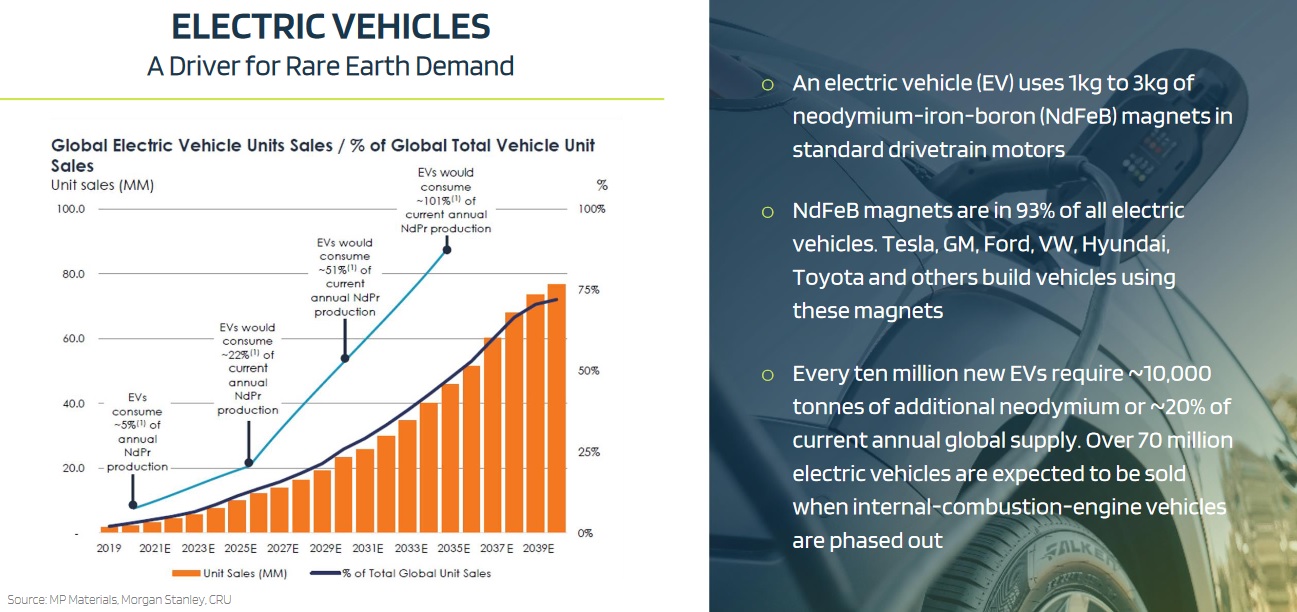

Now let’s look at the North American civilian market for REPMMs. An internal combustion, fossil fueled vehicle produced in North America today has between 25 and 50 micromotors. All of which are REPMMs. The total demand for REPMs to construct these motors is 0.5kg/vehicle. Even so, in a typical model year, the domestic American OEM automotive industry uses 8,500 mt of REPMs. But now, a major change is in the wind. A drive motor for a battery powered electric vehicle, if it is of the REPMM type, uses 2.5 kg of REPM! Thus each BEV that uses a REPMM for traction (drive) requires 5-10x the amount of REPM that an entire ICE powered vehicle requires!!

What began as a financial system to maximize profits has now created a dual market in critical minerals, the Chinese and the Rest of the World, (C+ROW). The financializers, their work done and rolling in the profits of their selfish misdeeds have now returned the problem of the security of supply chains back to the engineers. The dual commodity markets though will sharply reduce profits and the West’s capital is in the hands of those whose only interest is in the accumulation of money not the creation of wealth.

The military can pretend that increased prices for the support of domestic self-sufficiency don’t matter by subsidizing the military-industrial complex with “cost-plus” awards. The consumer economy does not have that luxury.

The latest existential crisis (the first such crisis was the ancient fear of God’s wrath by floods), “climate change,” has now pitched this dual commodity pricing problem to the forefront.

There is not enough of the critical metals for EV batteries and drive motors, not already under the control of China, to convert the global fleet of ICE vehicles to battery electric operation. Nor can there ever be.

China, alone, is and will remain self-sufficient in the critical metals necessary to convert its domestic ICE fleet to BEV operation and to produce enough stationary storage to be able to convert a large part of its domestic energy production by intermittent sources, wind and solar, to reliable maintenance of the grid.

The ROW (rest of the world), if it adopts the mandates of the Green Revolution, will have to choose winners and losers. There can be enough lithium, neodymium, praseodymium, dysprosium, and terbium produced outside of the control of China for some countries to achieve a significant fraction of their electricity by non-fossil fuel methods and the conversion of some of their transportation to electric operation. But those countries will have to together or individually create markets for the production and processing of those metals independent of Chinese control and pricing. This means permanent subsidies to miners, refiners, fabricators, and consumer and military product manufacturers. This means a lowering of living standards to pay for the subsidies.

Perhaps it’s time to rethink the Green New Deal. Are the consequences worth the decline of the West? Is climate variation really an existential crisis? And, how much longer can we ignore 90% of the world’s population that has most of the critical minerals we need within their control??