Welcome to the latest Technology Metals Report (TMR) where we highlight the Top 10 news stories that members of the Critical Minerals Institute (CMI) have forwarded to us over the last 2-weeks.

Key highlights in this Technology Metals Report include significant developments such as Rainbow Rare Earths Limited’s discovery in South Africa, China’s unveiling of the new heavy rare earth mineral Bayanoboite-Y, and the Australian Nuclear Science and Technology Organisation (ANSTO)’s $13.9 million funding for critical minerals research. The edition also spotlights the “CMI Masterclass: The Middle East’s Escalating Investment Interest in Africa’s Critical Minerals,” focusing on the strategic importance of Middle Eastern investments in Africa’s mineral sector. Moreover, the increasing global interest in Saudi Arabia’s mineral resources, highlighted at a recent mining conference in Riyadh, illustrates the geopolitical and economic shifts in the critical minerals landscape.

The 10 stories selected for this edition of the TMR, with source links to source stories for this fast-paced sector, are listed chronologically for your ease and review. These narratives highlight the dynamic shifts, strategic innovations, and geopolitical complexities shaping the critical minerals landscape, reflecting the increasing significance of these resources in technology, green energy solutions, and global market dynamics.

The Rare Earths Mine That Won’t Need a Single Shovel (January 17, 2024, Source) — George Bennett, a South African mining veteran, discovered a unique opportunity in two gypsum waste piles near the Mozambique border, which contain high concentrations of rare-earth minerals crucial for wind turbines and electric vehicles. This finding is notable due to the rarity of economically viable rare-earth concentrations, particularly above ground, and China’s dominance in the rare-earth market. Rainbow Rare Earths Limited (LSE: RBW), Bennett’s company, projects over $1 billion in net value from these piles, with no traditional mining costs. The project is set to start in 2026 and offers a competitive edge due to its low production costs and innovative processing methods. Despite market volatility, Rainbow’s unique approach positions it well in the growing demand for rare-earth oxides, essential for the energy transition. Referral, CMI Director, Russell Fryer

China discovers new heavy rare earth mineral (January 16, 2024, Source) — Chinese scientists have discovered a new heavy rare earth mineral named Bayanoboite-Y at the Bayan Obo Rare Earth Mine in Baotou, North China’s Inner Mongolia Autonomous Region. This mineral, unique in its chemical composition and crystal structure, contains significant heavy rare earth elements like yttrium, dysprosium, gadolinium, erbium, and lutetium. It marks the world’s first fluorocarbonate heavy rare earth new mineral discovery, signifying a major breakthrough in understanding the occurrence and evolution of heavy rare earth minerals. The Bayan Obo mine, crucial to China’s rare-earth reserves, has discovered 18 new minerals since 1959. China, leading globally in rare earth production, plans to expand its rare-earth industry, leveraging recent advancements in mining efficiency and recovery rates. Referral, CMI Director, Alastair Neill

China’s rare earth exports rise on demand from EV, high-tech sectors (January 12, 2024, Source) — In 2023, China’s rare earth exports rose by 7.3% to 52,307 metric tons, fueled by growing demand from the electric vehicle and high-tech sectors. As the world’s leading producer, China’s rare earths are essential in various applications, including new energy vehicles, wind power, and military equipment. Despite international tensions over critical mineral control and China’s export restrictions on certain key materials, demand continued to outstrip supply, affecting prices. However, fears of supply shortages, especially after a mining suspension in Myanmar, drove prices up. While China increased its mining quotas, its rare earth exports dropped by 18.24% in December 2023 compared to the previous month. Meanwhile, China’s rare earth imports surged by 45% in the last month, reflecting a 44.8% annual increase. Referral, CMI Director, Alastair Neill

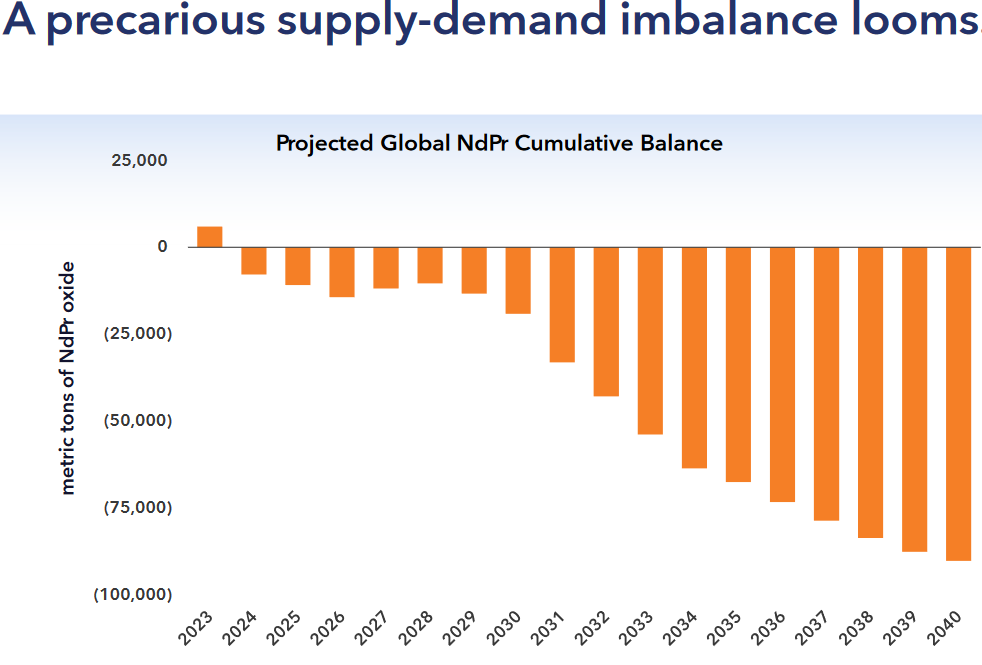

Will the magnet rare earths prices rise in 2024? (January 12, 2024, Source) — The magnetic rare earths sector, impacted by falling prices in 2022 and 2023 due to reduced global EV demand, is examined with a focus on Lynas Rare Earths Ltd. (ASX: LYC) and MP Materials Corp. (NYSE: MP). The downturn is linked to a slow global economy and EV sales decline, but a recovery is anticipated. Lynas has launched production at Australia’s Kalgoorlie Rare Earths Processing Facility, signaling progress. MP Materials is expanding in the USA with a focus on NdPr oxide and NdFeB magnets production. The sector’s future, potentially seeing a NdPr supply deficit as early as 2024, hinges on global economic recovery and EV market resurgence. These developments are crucial for establishing a Western-dominated rare earths and magnets industry within this decade.

ANSTO welcomes $13.9M critical minerals funding (January 12, 2024, Source) — The Australian Nuclear Science and Technology Organisation (ANSTO) has been allocated $13.9 million under the Australian Critical Minerals Research and Development Hub, as part of a wider $22 million funding package. This investment, announced by Minister Madeleine King, will support ANSTO’s research into rare earth elements, focusing on the discovery, extraction, and processing from clay-hosted and ionic adsorption deposits. Led by CEO Shaun Jenkinson, the project aims to enhance Australia’s standing in the global rare earth market, develop specific mineral processing techniques, and improve environmental outcomes. Collaborating with Geoscience Australia and CSIRO, ANSTO’s two-year project aligns with the national strategy for critical minerals, emphasizing their importance in green technologies and the pursuit of net zero emissions. Referral, CMI Co-Chairman Jack Lifton

Hunt for Critical Minerals Draws World Powers to Saudi Arabia (January 12, 2024, Source) — The global quest for critical minerals has brought world powers like the U.S., China, and Russia to Saudi Arabia, which is emerging as a key player in the mining sector. The kingdom, traditionally known for its oil wealth, is investing heavily in mining to diversify its economy and has positioned itself as a central hub in a “super region” rich in natural resources. This was highlighted at a recent mining conference in Riyadh, attended by international government and industry leaders. Saudi Arabia aims to leverage its strategic geographical position and vast untapped mineral wealth, recently re-estimated at $2.5 trillion, to attract global investments and partnerships. The conference saw significant participation, indicating a growing interest in Saudi Arabia’s mining potential and its efforts to establish stronger diplomatic and economic ties with various countries. Deals worth approximately $20 billion were expected, with the U.S. and Russia signing memorandums of understanding. This shift towards mining is part of Saudi Arabia’s broader Vision 2030 strategy to reduce oil dependency and cultivate new economic sectors. Referral, CMI Co-Chairman Jack Lifton

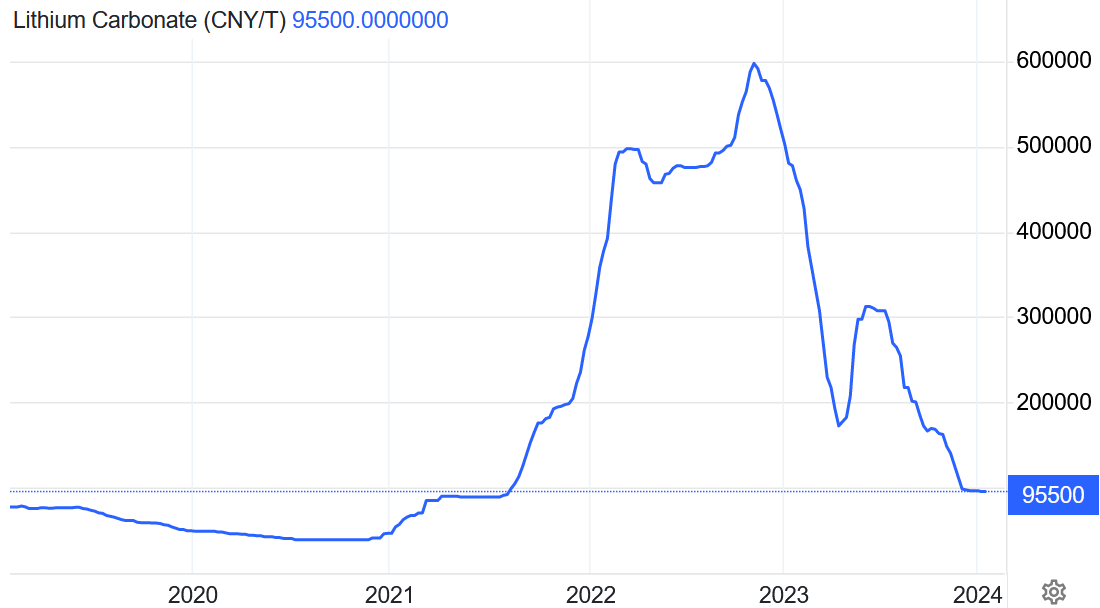

Why Core Lithium’s mine closure was just the tip of the iceberg (January 11, 2024, Source) — Core Lithium’s closure of its Grants mine reflects a broader crisis in the Australian mining sector, particularly impacting small-to-mid cap companies unnoticed for the last 12-24 months. Several mines, including First Quantum Minerals Ltd. (TSX: FM) and POSCO’s Ravensthorpe, Arcadian Lithium PLC’s (NYSE: ALTM | ASX: LTM) Mt Cattlin, and others, face similar risks due to declining battery metal prices and operational challenges. The cobalt market, for instance, saw dramatic price fluctuations, impacting projects like Jervois Global Limited’s (ASX: JRV | TSXV: JRV | OTCQB: JRVMF) Idaho Cobalt Project. Other companies, such as Hastings Technology Metals Ltd. (ASX: HAS) and Panoramic Resources Limited (ASX: PAN), have had to alter strategies due to various challenges. This trend contrasts with larger, stable companies like Pilbara Minerals and underscores the need for revised economic studies and strategies in a volatile market. Referral, CMI Director, Peter Clausi

Serra Verde Enters Commercial Production (January 11, 2024, Source) — Serra Verde has commenced commercial production of Mixed Rare Earth Concentrate from its Pela Ema deposit in Brazil. Targeting 5,000 tonnes annually, these rare earths are crucial for electric vehicle motors and wind turbines. The company has secured customer acceptance and offtake agreements, with plans to double production by 2030. Emphasizing sustainability, Serra Verde’s operations use eco-friendly methods and renewable energy. CEO Thras Moraitis highlights the company’s role in producing critical rare earths, supporting sustainable energy transitions. Ricardo Grossi, COO, emphasizes Brazil’s emerging role in rare earth production and the company’s commitment to sustainable practices and stakeholder benefits. Referral, CMI Director, Alastair Neill

Rare Earth Oxide separation work commences at the back-end pilot plant in Florida, U.S. (January 11, 2024, Source) — Rainbow Rare Earths Limited (LSE: RBW) has initiated the separation of rare earth oxides at their pilot plant in Florida, U.S., using a continuous ion exchange and chromatography process developed by K-Technologies. This innovative approach, replacing traditional solvent extraction, is set to produce critical rare earths like neodymium, praseodymium, dysprosium, and terbium, crucial for the green economy. The Johannesburg pilot plant has prepared and shipped mixed rare earth carbonate to Florida for separation, enhancing the process by producing a cerium-depleted version for more efficient separation. Despite some delays, the project continues to make significant advancements in optimizing the process for commercial scale. The Phalaborwa project, a key part of Rainbow’s strategy, aims to establish an independent, ethical supply chain for rare earth elements, essential in various advanced technologies and green energy solutions. Referral, CMI Director, Alastair Neill

CMI Masterclass: The Middle East’s Escalating Investment Interest in Africa’s Critical Minerals (January 10, 2024, Source) — The “CMI Masterclass: The Middle East’s Escalating Investment Interest in Africa’s Critical Minerals,” led by Tracy Weslosky of the Critical Minerals Institute, discussed the rising Middle Eastern investment in Africa’s mineral sector. Experts, including Melissa Sanderson, Jack Lifton, and Russell Fryer, explored its strategic significance for the global market and supply chain. The impact on American firms and competition with China in Africa were key topics. The session also examined the broader implications of such investments, as illustrated by Robert Friedland’s company’s Middle Eastern funding. The panel weighed the financial benefits against long-term strategic, economic, and geopolitical challenges, offering insight into the complex dynamics of global critical minerals investment.

Defense Metals Signs MOU with Ucore to Ship Rare Earth Carbonate to RapidSX™ Facility in Ontario (January 9, 2024, Source) — Defense Metals Corp. (TSXV: DEFN | OTCQB: DFMTF) and Ucore Rare Metals Inc. (TSXV: UCU | OTCQX: UURAF) have agreed on a Memorandum of Understanding (MOU) to forge a North American rare earth element (REE) supply chain. Under this MOU, Defense Metals will send a rare earth carbonate sample from its Wicheeda REE project in British Columbia to Ucore’s RapidSX™ facility in Ontario for processing. This initiative is a critical step in establishing a Western REE supply chain, responding to the growing demand for REE feedstock. The collaboration, featuring Defense Metals’ strategically located Wicheeda project and Ucore’s innovative RapidSX™ technology, aims to evaluate joint venture possibilities. This partnership aligns with Ucore’s broader strategy, including the development of a commercial REE processing plant in Louisiana, supported by the US Department of Defense and the Canadian Government.

Investor.News Critical Minerals Media Coverage:

- January 12, 2024 – Will the magnet rare earths prices rise in 2024? https://bit.ly/48Q1C6f

- January 9, 2024 – Defense Metals Signs MOU with Ucore to Ship Rare Earth Carbonate to RapidSX™ Facility in Ontario https://bit.ly/4aIQH05

- January 7, 2024 – Unveiling Hallgarten & Company’s Latest Insight: Model Resources Portfolio: Peak Climate Hysteria https://bit.ly/48raH5E

Investor.News Critical Minerals Videos:

- January 16, 2024 – Jeff Killeen on PDAC 2024: Shaping the Future of Critical Minerals and Mining https://bit.ly/3TYprop

- January 10, 2024 – CMI Masterclass: The Middle East’s Escalating Investment Interest in Africa’s Critical Minerals https://bit.ly/3HnUQZL

Critical Minerals IN8.Pro Member News Releases:

- January 19, 2024 – Power Nickel Commences 2024 Drill Program https://bit.ly/3vF8yot

- January 19, 2024 – Zentek Announces Eric Wallman Appointed as Chairman of the Board https://bit.ly/3u2y0nx

- January 17, 2024 – Defense Metals Announces McLeod Lake Indian Band Co-Design Agreement and Partnership Investment https://bit.ly/48UduUX

- January 16, 2024 – Fathom Announces Commencement of Exploration at Albert Lake Project and Selection for Participation at AME Roundup Core Shack https://bit.ly/3tJGujq

- January 16, 2024 – Appia Reports 92,758 ppm (9.3%) TREO, 13,798 ppm MREO (1.38%) and 2,241 (.24%) ppm HREO over 2m Within the Total Weighted Average of 38,655 ppm (3.87%) TREO, 6,869 ppm (.69%) MREO, and 1,380 ppm (.14%) HREO Across 24m (EOH) Following the Reanalysis of Over-Limit Assay Results from PCH-RC-063 at the PCH Ionic Adsorption Clay Project in Goias, Brazil https://bit.ly/48MrNuQ

- January 16, 2024 – F3 Announces Intention to Spin-Out F4 Uranium Corp. https://bit.ly/3Hm37NV

- January 15, 2024 – Panther Metals PLC – Fulcrum Metals: Update on Saskatchewan Uranium Projects https://bit.ly/423pmlh

- January 15, 2024 – Appia Announces Significant Geochemical Critical REE Assay Results at Alces Lake Project, Saskatchewan, Canada https://bit.ly/3HlFLbc

- January 12, 2024 – F3 Grants Options https://bit.ly/3vCzYvi

- January 12, 2024 – Ucore Invited to Present at National Defense Industry Association Event https://bit.ly/3TZ7giq

- January 11, 2024 – Panther Metals PLC: Graphite Discovery Grows Significantly at Obonga https://bit.ly/3SeTjvc

- January 11, 2024 – Ucore Makes Announcement Regarding Convertible Debentures https://bit.ly/4aQ3de5

- January 11, 2024 – Appia Receives Approval for 12 Additional Claim Blocks at Its PCH Rare Earths Ionic Adsorption Clay Project, Goias, Brazil https://bit.ly/3O0yzFc

- January 11, 2024 – Nano One Announces Carlo Valente as CFO https://bit.ly/3RSkpaf

- January 9, 2024 – Auxico Announces Results of a 2023 Sampling Campaign on the Minastyc Property https://bit.ly/47w158C

- January 9, 2024 – Critical Metals PLC Notice of AGM / Board Changes and Extension of Warrant Term https://bit.ly/3TSV2rB

- January 9, 2024 – Imperial Welcomes Guy Bourassa as CEO New Appointment Adds Depth to the Management Team https://bit.ly/48r6C1l

- January 9, 2024 – Power Nickel Raises $2,180,000, Outlines 2024 Plans https://bit.ly/41Pr4qe

- January 9, 2024 – Defense Metals to Ship Wicheeda Mixed Rare Earth Carbonate Sample to Ucore Rare Metals Inc. https://bit.ly/3RNhWhn

- January 8, 2024 – Sage Potash Secures Permit Approvals for Exploration Program at Sage Plain Potash Project https://bit.ly/3H9x9En

- January 8, 2024 – F3 Mobilizes to Drill A1 and B1 at PLN https://bit.ly/3TPP0Yw

- January 8, 2024 – Critical Metals PLC Placing https://bit.ly/3NPxiRm