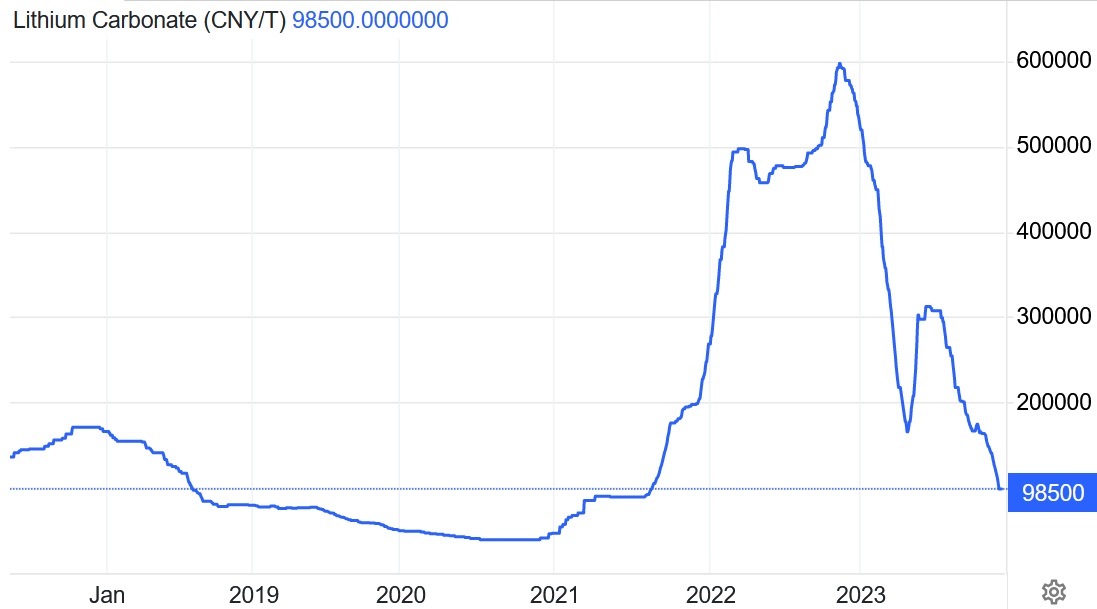

The lithium sector has been the standout of all sectors in 2021, led by lithium prices surging higher from about US$7,000/t to around US$30,000/t in 2021. Ordinarily, you could expect prices to fall back to earth, but in this case, lithium demand is so strong that prices are unlikely to fall back anytime soon.

Bloomberg recently stated: “EVs have lithium booming — and this time, there is no bust in sight. Demand is expected to outstrip metal production for at least the next five years with few new mining projects on the horizon.”

Benchmark Mineral Intelligence recently stated: “Right now lithium demand is growing at three times the speed of lithium supply.”

Furthermore, a November 2020 UBS forecast is for “lithium demand to lift 11-fold from ~400kt in 2021 through to 2030.”

Lithium carbonate price graph showing the extraordinary 2021 price gains

Source: Fastmarkets

Given the above information, it makes very good sense to invest in the potential next tier of lithium miners. Added to this is the trend towards increasing market share of lithium iron phosphate (“LFP”) batteries, which will lead to greater demand for lithium carbonate, best sourced from lithium brine. Right now Argentina offers the best exposure to emerging lithium brine miners.

Top 5 lithium junior miners (in alphabetical order)

- Alpha Lithium Corporation (TSXV: ALLI)

- Arena Minerals Inc. (TSXV: AN)

- Argosy Minerals Limited (ASX: AGY)

- Galan Lithium Ltd. (ASX: GLN)

- Lithium South Development Corporation (TSXV: LIS | OTCQB: LISMF)

Alpha Lithium Corporation

Alpha Lithium (Alpha) 100% own 27,500 hectares of the Tolillar Salar in Argentina and 5,072 hectares at one of the leading salars in Argentina, Hombre Muerto. The Tolillar Salar grades are lowish and in the 200-350 mg/L range with Mg:Li ratios between 4.90 and 5.37 which is ok. A big plus is that Alpha has 100% of the Tolillar salar to themselves and has now expanded into Hombre Muerto. Additionally, the two Projects have potential future synergies being only 10 kms from each other.

Alpha is testing their in-house developed Direct Lithium Extraction (DLE) process and has achieved some strong results including lithium concentrations of 9,474 mg/L with significant rejection of impurities. They are also testing DLE with Lilac Solutions (private).

At Hombre Muerto drilling is yet to start but given it is the best salar in Argentina then results could potentially be very good. Alpha’s Hombre Muerto tenements are on the outskirts of the POSCO property, noting POSCO paid US$280 million to acquire these from Galaxy Resources. Alpha Lithium is taking a fast-track approach towards reaching production, then planning to ramp up volumes thereafter.

Alpha Lithium trades on a market cap of C$158 million and has loads of potential.

Arena Minerals Inc.

Arena Minerals (Arena) has two projects in Argentina which are Sal de la Puna (11,000 hectares) in the Pastos Grandes salar, Argentina and Antofalla (6,000 hectares) located immediately adjacent and south of Albemarle’s tenements. Arena also own the Atacama Copper Project in Antofagasta, Chile.

At the Sal de la Puna Project Ganfeng Lithium has acquired a 35% project share. Ganfeng also owns a 19.9% equity stake in Arena. Lithium Americas also bought $10 million of shares in Arena recently.

Arena Minerals trades on a market cap of C$206 million. Great partners but Arena has sold some Project share at Sal de la Puna. Possible takeover target. Copper in Chile is a bonus.

Argosy Minerals Limited

Argosy Minerals (Argosy) owns a 77.5% interest (with a right to move to 90%) in their flagship Rincon Lithium Project on the Salar del Rincon in Argentina. Argosy also owns the Tonopah Lithium Project in Nevada, USA.

Argosy’s Resource is still quite small but should potentially be easily expanded when needed. Lithium grade is a bit below average at 324-369mg/L and the Mg:Li ratio is a bit high. All this means is slightly higher operating costs which is not an issue these days with surging lithium demand and very good lithium prices. Argosy is fully-funded and 45% construction completed towards their plan to expand to 2,000tpa lithium carbonate production with first product by mid-2022. Thereafter the plan is to expand by 10,000tpa lithium carbonate production to have 12,000tpa production.

The big deal about Argosy is that they are already producing at pilot plant stage with large evaporation ponds already built. This makes them one of the most advanced lithium juniors globally.

Argosy Minerals trades on a market cap of A$353 million. One of the very best and most advanced juniors.

Argosy Minerals Rincon Project is already producing battery grade lithium carbonate and working towards 2,000tpa then 12,00tpa LCE

Source: Argosy Minerals website

Galan Lithium Ltd.

Galan Lithium (Galan) is developing their flagship Hombre Muerto West (“HMW”) Project located on the west side edge of the world class Hombre Muerto Salar. Galan also has the nearby Candelas Lithium Project also at southern edge of the Hombre Muerto Salar. Galan also owns 80% of the exploration stage Greenbushes South Lithium Project which is only 3km south of the world-class Greenbushes mine.

At Hombre Muerto West, Galan has 2.3 million tonnes contained LCE at 946mg/L (very high grade) and a very low Mg/Li ratio of <2.0. When including Candelas, in total Galan has 3.0m tonnes contained LCE @858mg/L. Galan completed a very positive PEA in 2020 with a post-tax NPV8% of US$684 million.

Galan is doing further drilling in Q4, 2021 with a FS planned for 2022.

Galan Lithium trades on a market cap of A$472 million. Top class resource and looking like a future star performer.

Hombre Muerto Salar – Galan tenements (blue outline), Livent (red), Galaxy now Orecobre (yellow), POSCO (white)

Source: Galan Lithium investor presentation

Lithium South Development Corporation

Lithium South Development Corp. (Lithium South) has 3,287 hectares of tenements under purchase option at their Hombre Muerto North (HMN) Project, on the northern edge of the Hombre Muerto salar. The Project lies just north of the POSCO and Orecobre projects, and near Livent’s very successful lithium mine.

Lithium South has a M&I Resource of 571,000t contained LCE, with a high lithium grade of 756mg/L and a very low Mg/Li ratio of 2.6:1. The Project has potential exploration upside. Lithium South is trialing DLE technology in parallel with proven evaporation technology. Their environmental baseline study is also underway with Phase 1 recently completed. The Hombre Muerto North Project PEA (based only on some of the claims) resulted in a post-tax NPV8% of US$217 million and 28% IRR, based only on 5,000tpa lithium carbonate production over a 30 year mine life. Initial CapEx was estimated at US$93.3 million and OpEx at US$3,112/t lithium carbonate. These are excellent numbers, albeit for an initial smaller size production project. Lithium South is working to further expand the resource following some good TEM study results.

Lithium South trades on a market cap of C$67 million. Looks very attractive on such a low market cap.

Closing remarks

The above top 5 lithium juniors all have lithium brine projects located in Argentina. All still have reasonably low market caps and all have great potential in the years ahead. The usual risks apply to lithium juniors such as country risk, exploration risk, funding risk, permitting risk, production risk etc. In the case of these juniors, many have run up in price recently so buying in stages can add safety in case there is a price pullback.

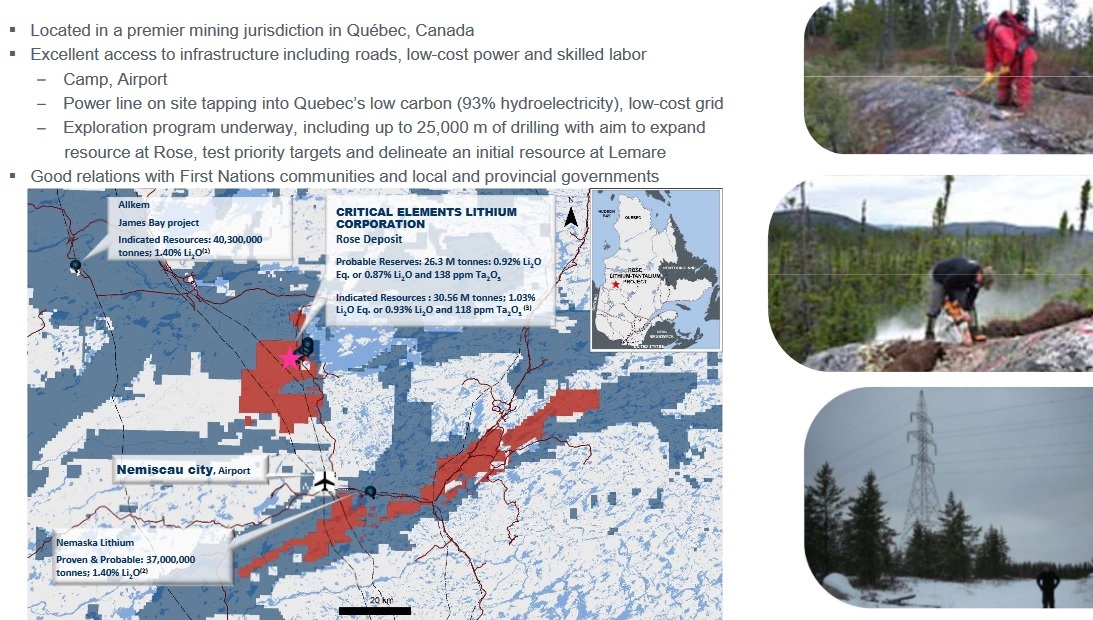

If looking to diversify away from Argentina then some other good juniors such as Critical Elements Lithium Corporation (TSXV: CRE | OTCQX: CRECF) (Canada lithium spodumene project), Global Lithium Resources (ASX: GL1) (Australian spodumene project), and Lithium Power International Ltd. (ASX: LPI) (Chile JV lithium brine high grade project) are worth considering.

Best to take a 5 year time frame and remember to diversify. The EV boom has only just begun so lithium still has a great decade ahead.

Disclosure: The author is long all of the stocks mentioned in the article (except Livent and POSCO).