Lithium Royalty Corp.: Poised for Success as More Affiliates Reach Production

Lithium demand continues to surge each year, despite some year on year (“YoY’) volatility in demand and prices. In 2021 the IEA forecast lithium demand to increase from 13x to 42x from 2020 to 2040. Trend Investing forecasts lithium demand to increase 35x from 2020 to 2037 as we move to a 100% electric vehicle world. Rio Tinto Group (NYSE: RIO | LSE: RIO) forecasts that the world will need 60 new lithium mines the size of Jadar. BMI forecasts that we will need 78 new lithium mines from 2022 to 2035.

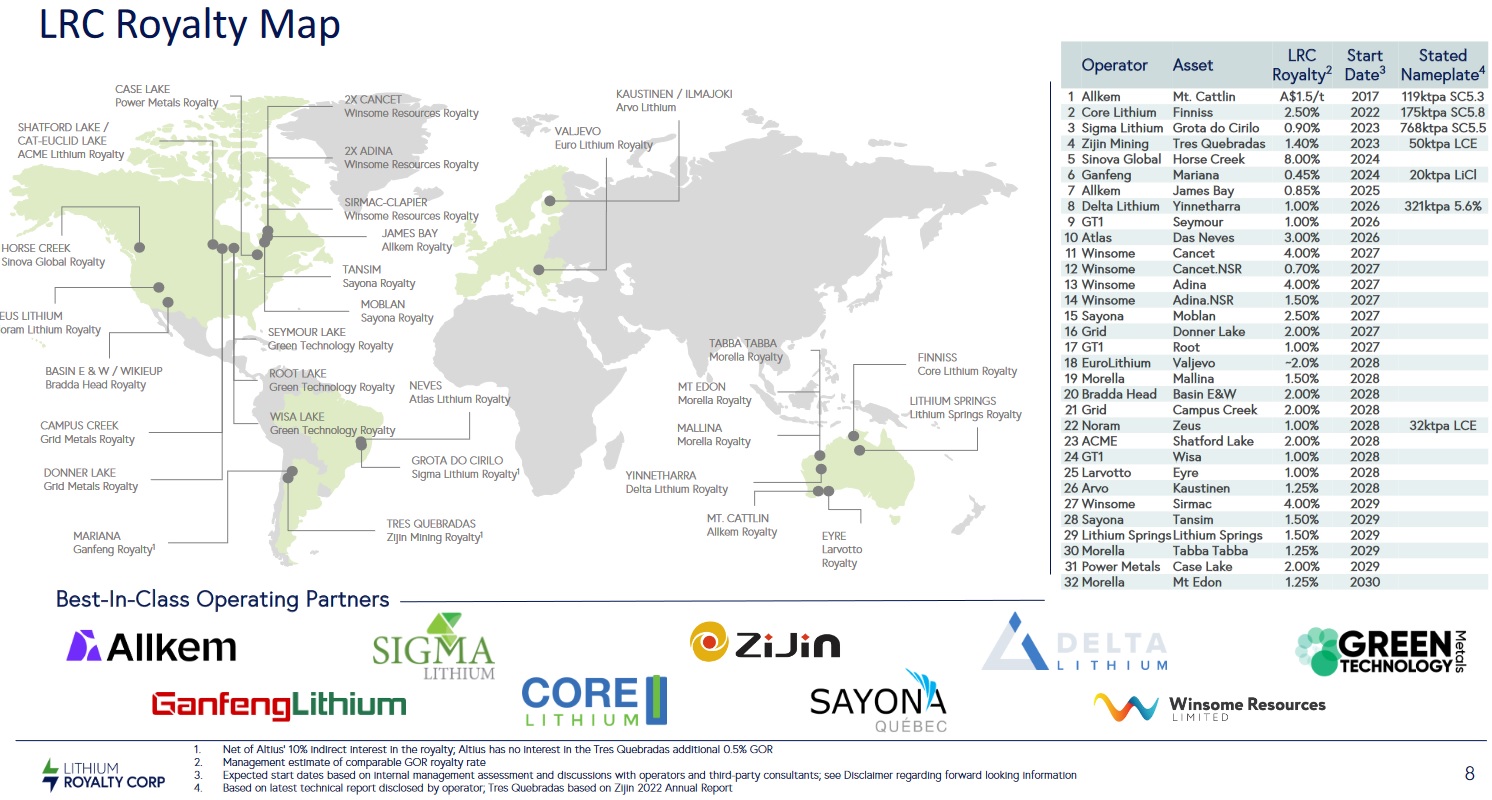

The massive demand wave coming for lithium makes for a perfect royalty play in the sector. The key advantage of royalty companies is broad exposure to many companies’ potential revenue streams. Today’s company gives investors exposure to 32 royalties across 7 countries.

Lithium Royalty Corp. (TSX: LIRC) (“LRC”)

LRC is a pure-play battery metal royalty company with a focus on lithium royalties. LRC has been steadily acquiring royalties since 2018 with a focus on safe mining jurisdictions. The large majority are lithium royalties in mines/projects located in South America, Canada, and Australia (see charts below).

Lithium Royalty Corp. (“LRC”) global portfolio of 32 royalties with a focus on lithium

LRC lithium royalty revenues with more set to potentially come online in the near term

Looking at the list in the chart above we see that LRC already has several revenue streams from key lithium producers including Allkem Limited‘s (ASX: AKE | TSX: AKE) Mt Cattlin Mine, Core Lithium Limited‘s (ASX: CXO) Finniss Mine, and SIGMA Lithium Corporation‘s (NASDAQ: SGML | TSXV: SGML) Grota do Cirilo Mine plus others potentially to follow in the near term including Zijin Mining Group‘s Tres Quebradas Project, Ganfeng Lithium Group‘s Mariana Project, and Delta Lithium Limited‘s (ASX: DLI) Yinnetharra Project.

Also, all going well, by ~2027 Winsome Resources Ltd.‘s (ASX: WR1) Cancet and Adina Projects (potential ~50Mt resource in the making) look very promising based on drill results so far, as does Sayona Mining Limited‘s (ASX: SYA | OTCQB: SYAXF) Moblan JV which already has a Total Resource of 51.4Mt @ 1.31% Li2O. Both projects are in Canada.

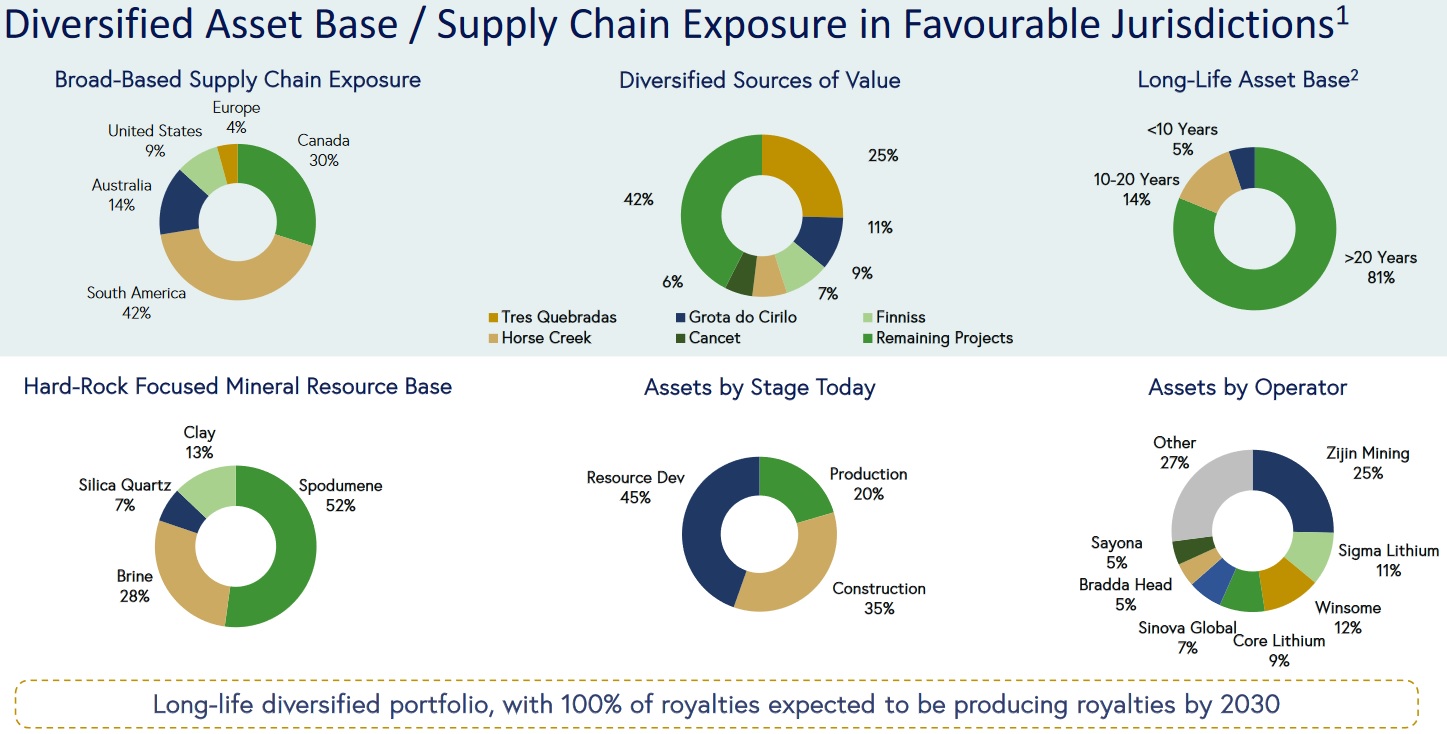

LRC’s portfolio is advancing well with 20% in production

LRC’s portfolio has grown since 2018 to now include 32 royalties.

Country exposure of the LRC portfolio is South America (42%), Canada (30%), Australia (14%), USA (9%), and Europe (4%). This would be considered a safe mix of countries, noting the South America exposure is mostly Argentina and Brazil.

Portfolio value is nicely diversified with 42% of the portfolio in the others category. The largest holding by value is the Zijin Mining’s Tres Quebradas Project (25%); however, the next largest is only at 11%.

LRC’s royalty portfolio has good long-life assets averaging 19 years.

Hard rock spodumene assets dominate the portfolio at 52% which is seen as a positive considering they are usually faster and cheaper to bring into production than other lithium projects.

20% of the LRC royalty portfolio is already in production, 35% are in the construction stage, and 45% are in the development stage.

The overall quality of the portfolio looks solid with most companies standing a good chance at being producers by 2030.

A summary of LRC’s royalty portfolio characteristics

Source: LRC company presentation

Some advantages of royalty companies include – Diversification across a large portfolio is much lower risk than just owning a few lithium miners and exposure to the underlying commodity price (lithium) with minimal project execution risk.

LRC’s Q2, 2023 financial results

LRC announced Q2, 2023 results on August 14, 2023, which included royalty revenue up 98%, gross profit up 280%, and a small loss of C$0.02 per basic share. LRC’s royalty income for Q2 was C$838k. The announcement gives a lot more details on their royalty portfolio, including the newer acquisitions, and mentions a new credit agreement with the National Bank of Canada for C$25 million.

Closing remarks

The lithium boom looks to be very well established and still has about 2 decades to run as the world transitions to sustainable energy (energy storage with Li-ion batteries) and electric vehicles.

Buying a lithium royalty portfolio is a safer way to gain broad exposure to a number of companies. The main risk is that if the royalty portfolio companies don’t make it to production. Valuation is not an easy task so investors may need to rely on analyst’s price targets.

Lithium Royalty Corp. trades on a market cap of C$688 million. The August 2023 company presentation stated LRC’s net asset value at C$1,061 million.

LRC looks like a good quality royalty play on lithium. The key will be lithium prices and how the underlying portfolio of companies perform. Stay tuned.