Top 3 best valued lithium juniors, as lithium prices near a bottom

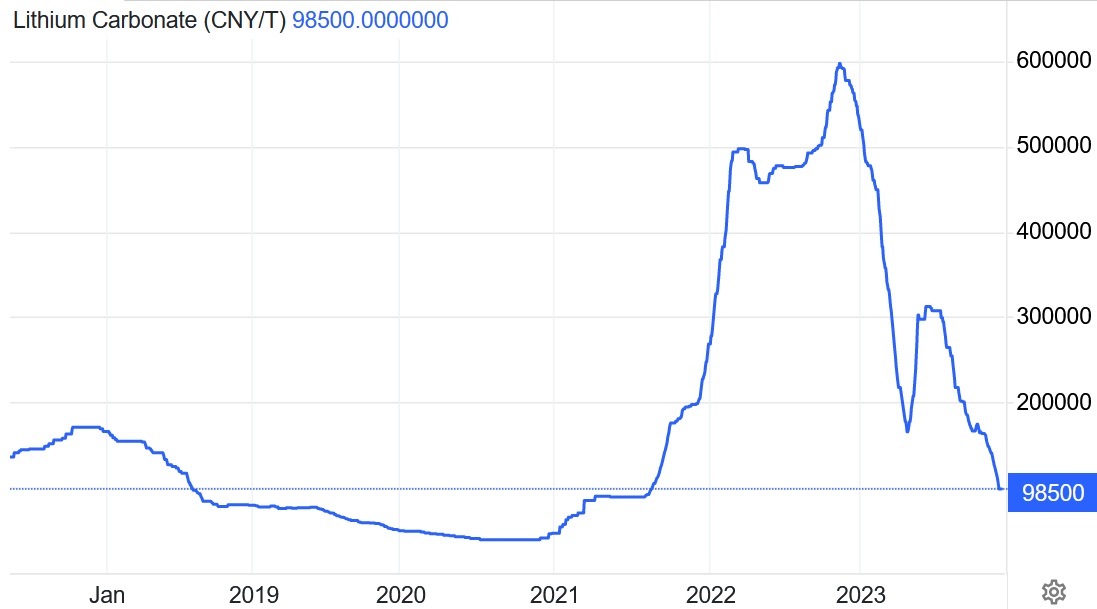

Following an incredible 2022, the lithium sector has had a horrible 2023; however soon the pain should be over. The China lithium carbonate spot price is down 82.5% in the past year and is now below the marginal cost of production, meaning the lithium price fall should end very soon. This assumes the marginal cost producers continue to stop production and that EV sales continue to grow in 2024.

This means it’s now time to take a fresh look at the beaten down lithium stocks as we approach 2024. Today we look at 3 very well valued lithium juniors with high quality lithium projects likely to make it to production before 2027.

China lithium spot price 5 year chart showing the lithium price bottom has been reached or it should bottom very soon

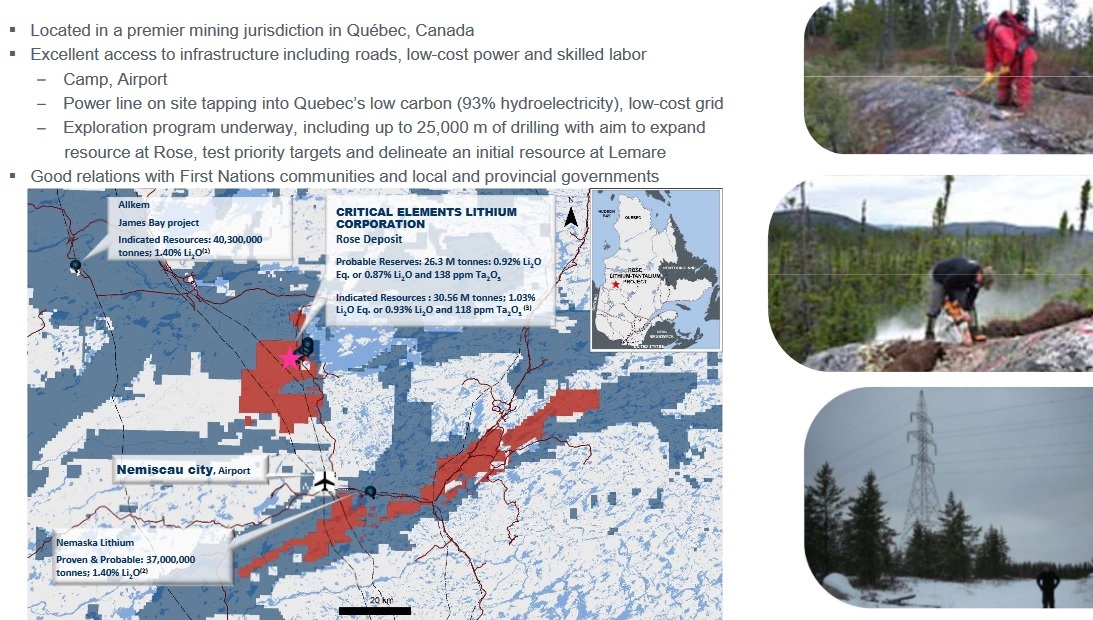

Critical Elements Lithium Corporation (TSXV: CRE | OTCQX: CRECF)

Critical Elements Lithium is arguably the most undervalued advanced lithium junior globally. The Company is in the project funding stage for their 100% owned Rose Lithium-Tantalum spodumene Project in Quebec, Canada.

The Rose Project August 2023 Feasibility Study resulted in an after-tax NPV8% of US$2.195 billion and an after-tax IRR of 65.7% with average price assumptions of US$4,699 per tonne technical grade lithium concentrate, US$2,162 per tonne chemical grade lithium concentrate, and US$150 per kg tantalum pentoxide (Ta2O5). Initial CapEx is estimated at US$471 million and OpEx at US$617/t spodumene.

The Project achieved its mining license in September 2023 and in October 2023 ordered its long lead equipment for the Project construction. To achieve project funding Critical Elements is evaluating what they state as “continued interest from blue-chip strategic partners”.

Management is top tier with development and operational lithium experience, including the former Rockwood Lithium CEO and CFO (Rockwood was sold to Albemarle Corporation (NYSE: ALB) for US$6.2 billion in January 2015).

Possible 2026 lithium spodumene producer. Critical Elements Lithium trades on a market cap of C$200 million.

Critical Elements Rose Project in Quebec, Canada

Source: Critical Elements Company presentation

Frontier Lithium Inc. (TSXV: FL | OTCQX: LITOF)

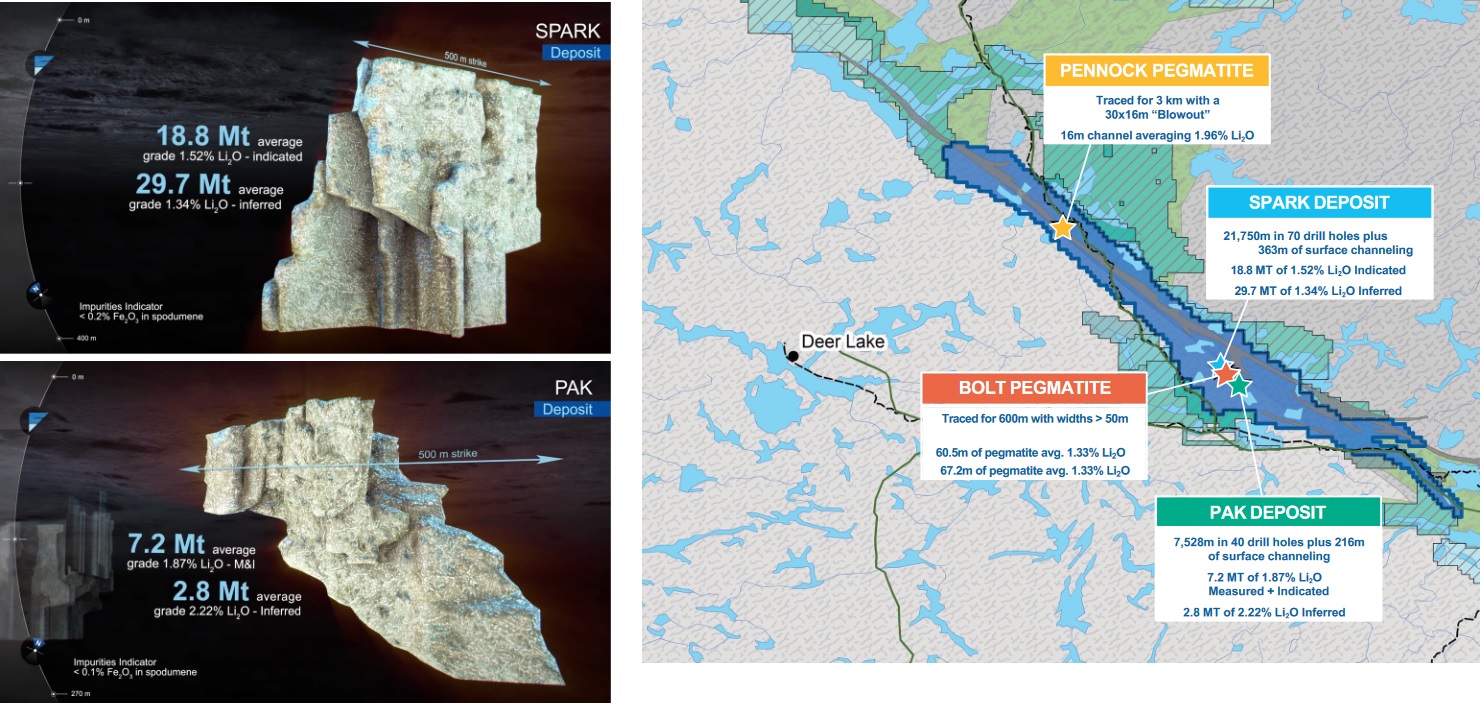

Frontier Lithium 100% owns the PAK Lithium Project in northern Ontario, Canada. The Project has a tier one total Resource of approximately 58.5 Mt at high grades spread across the Spark and PAK deposits, as shown below.

The PAK Project 2023 PFS resulted in a post tax NPV8% of US$1.74 billion, 24% IRR, based on a lithium hydroxide selling price of US$22,000/t. Phase 1 CapEx (Mine & Mill) was estimated at US$468 million and Phase 2 (expansion and LiOH refinery) at US$576 million.

A key positive for Frontier Lithium is they can sell high quality technical grade at a high price in the first stage of the project. Another positive is that the PAK Deposit has a very high-grade zone of 657kt at 3.59% Li2O. Road access to the Project remains the main issue; however, the upcoming 2024 DFS Phase 1 is advancing the option of building the mine and mill using a winter road and for transportation of spodumene concentrates.

Frontier Lithium is targeting to commence spodumene production in H1, 2027. Frontier Lithium trades on a market cap of C$161 million.

Frontier Lithium has a tier one lithium resource at their PAK Project in Ontario, Canada

Source: Frontier Lithium company presentation

Lithium Ionic Corp. (TSXV: LTH | OTCQX: LTHCF)

Lithium Ionic owns two lithium projects in Brazil – Itinga Project (100%) and Salinas Project (85%). Itinga is near Sigma Lithium Corporation’s (NASDAQ: SGML | TSXV: SGML) Grota do Cirilo Mine and Salinas is adjacent to Latin Resources Limited’s (ASX: LRS) Colina Project. The current Resource Estimate of the Itinga Project is a M&I Resource of 16.69Mt @1.41% Li2O and an Inferred Resource of 16.21Mt @ 1.34% Li2O.

At the Itinga Project, the 2023 PEA Initial Phase (Bandeira only) resulted in a post-tax NPV8% of US$1.6 billion and an IRR of 121% to produce 217,700tpa of spodumene over a 20 year mine life. Despite being an underground mine the CapEx estimate was only US$233 million and the OpEx was US$349/t spodumene.

In some exciting news released on December 12, 2023, Lithium Ionic reported: “Widest and Highest-Grade Lithium Intercept to Date; Drills 1.72% Li2O Over 53.7m, incl. 1.87% Li2O over 39.5m at Bandeira, Minas Gerais, Brazil. This is one of the better drill results all year globally. Lithium Ionic CEO, Blake Hylands, stated:

“These results continue to emphasize the robustness of the lithium deposit at Bandeira, which currently represents around 90% of our total resource tonnage but only ~1% of our total property size pointing to the immense potential and scalability of our projects in this lithium-rich region.”

Catalysts in 2024 include further drill results, an updated Bandeira Resource and FS due early 2024, and project construction approvals (mid 2024).

A possible 2026 lithium spodumene producer. Lithium Ionic trades on a market cap of C$203 million.

Closing remarks

Commodity prices go in cycles. For lithium, the 2022 price boom was due to a temporary deficit in the market as global plugin electric car sales surged 56% higher that year. In 2023 we are likely to see a slowdown to ~28% sales growth, which has allowed lithium supply to catch up again with demand, hence the huge lithium price fall in 2023. 2024 is open for debate. If we get similar global plugin electric car sales growth as 2023, then the lithium market should be reasonably balanced and lithium prices a lot more stable. Looking out to the second half of this decade it is hard to see lithium supply keeping up with demand as the EV boom takes off with ever increasing numbers of sales. This means lithium juniors that can make it to production after 2025 may enjoy a very favorable lithium market.

Our top 3 best valued quality lithium juniors with near term production potential are Critical Elements Lithium Corporation, Frontier Lithium Inc., and Lithium Ionic Corp. Let’s check back in 2027 and see how they are doing.