Technology Metals Report (02.23.2024): Yellen to Visit Chile for Critical Minerals and Biden’s EV Dreams Are a Nightmare for Tesla

Welcome to the latest issue of the Technology Metals Report (TMR), brought to you by the Critical Minerals Institute (CMI). In this edition, we compile the most impactful stories shared by our members over the past week, reflecting the dynamic and evolving nature of the critical minerals and technology metals industry. From the Inflation Reduction Act’s challenges for the American EV industry to China’s lithium market developments and Treasury Secretary Janet Yellen’s strategic visit to Chile, our report covers a wide array of developments crucial for stakeholders. The unveiling of Tesla Inc.’s (NASDAQ: TSLA) lithium refinery in Texas, alongside CATL’s confirmation of its lithium mine’s normal operations, paints a picture of the industry’s efforts to navigate through pricing volatilities, supply chain complexities, and geopolitical tensions. Moreover, the significant moves by major financial institutions in the uranium market and Gecamines’ strategic overhaul in the DRC underline the shifting paradigms in the mining and investment landscapes of technology metals.

This TMR report also highlights the broader implications of these developments on the global stage, including efforts to diminish reliance on China for essential metals, the impact of Tesla’s pricing strategies on the used EV market, and the strategic dialogues around rare earths markets. The visit by US Treasury Secretary Janet Yellen to Chile is spotlighted as a key initiative to bolster ties around critical minerals, emphasizing the urgency of diversifying supply chains amid growing demands for green transition materials. Additionally, the narrative around the challenges posed by the Inflation Reduction Act for Tesla and the US car industry, coupled with BHP’s cautionary stance on the Australian nickel sector, illustrates the complex interplay between policy, market dynamics, and strategic resource management. As we delve into these stories, our aim is to provide a comprehensive overview that informs and stimulates discussion among policymakers, industry leaders, and stakeholders, navigating the intricate pathways towards a sustainable and competitive future for critical minerals and technology metals.

MP Materials swings to quarterly loss on falling rare earths prices (February 22, 2024, Source) — MP Materials Corp. (NYSE: MP) reported a fourth-quarter loss, attributed to declining rare earths prices and increased production costs, despite expectations of a larger deficit. Amidst unsuccessful merger discussions with Lynas Rare Earths Ltd. (ASX: LYC) and competition from Chinese firms, CEO Jim Litinsky emphasized the potential for mutual learning and cost reduction among companies. Despite a 2.7% drop in shares on Thursday, a slight recovery was observed in after-hours trading. The company experienced a significant shift from previous year’s profit to a $16.3 million loss. Sales of rare earths concentrate to China decreased by 34% due to lower production at its Mountain Pass mine, exacerbated by facility issues. However, MP is advancing in refining rare earths domestically, with ongoing projects in California and Texas, and has initiated production in a new facility in Vietnam.

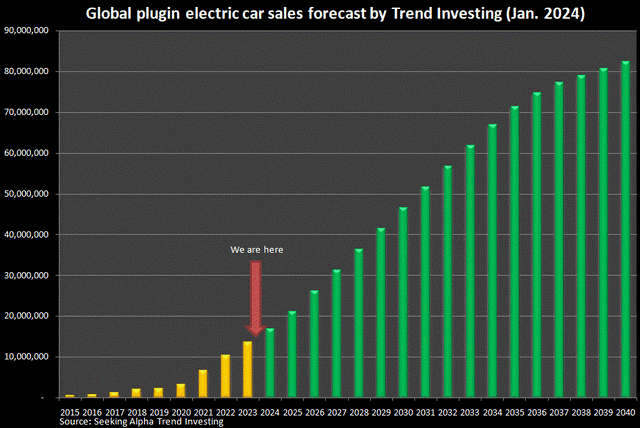

Stalling the American EV Industry: The Unintended Consequences of the Inflation Reduction Act’s Attempt to Bypass China for Critical Minerals (February 22, 2024, Source) — The Inflation Reduction Act (IRA), integral to President Joe Biden’s environmental strategy, seeks to transition the American automotive industry towards a US-centric electric vehicle (EV) supply chain, reducing reliance on Chinese materials. This shift, exemplified by initiatives like Tesla Inc.’s (NASDAQ: TSLA) lithium refinery in Texas, aims to enhance the competitiveness of American-made EVs. However, the IRA’s stringent requirements for sourcing materials domestically or from approved countries by 2024 pose significant challenges, complicating efforts by major manufacturers to maintain affordability and quality. Jack Lifton, an expert in the field, highlights the complexity of creating a new EV supply infrastructure and the strategic challenges of overtaking China’s advanced position in the EV sector. The article emphasizes that realizing the IRA’s vision demands innovation, strategic foresight, and time, presenting both obstacles and opportunities for the U.S. automotive industry in its quest for sustainability and energy independence.

Battery factories: Europe’s mechanical engineering companies are lagging behind (February 22, 2024, Source) — The report “Battery Manufacturing 2030: Collaborating at Warp Speed” by Porsche Consulting and the German Engineering Federation (VDMA) highlights the expansion of battery factories, with around 200 set to be constructed worldwide in the next decade, predominantly in Europe. Despite this growth, European mechanical engineering firms are trailing behind their Asian counterparts, particularly in supplying high-tech equipment for these factories, with only 8% of such technology currently coming from Europe. This low market share limits Europe’s influence on technical development in the battery sector. The study suggests that to avoid technological dependency and enhance their market position, European companies must aim for at least a 20% market share, requiring significant growth and collaboration to offer integrated factory solutions competitive with turnkey plants from China. The study emphasizes the potential for growth and the critical need for European firms to innovate and collaborate to secure a substantial stake in the rapidly expanding battery production technology market, estimated at 300 billion euros by 2030.

“This is a very important article, because it illustrates that the EV battery manufacturing industry has become technologically dependent upon Chinese manufacturing technology for efficient and economical production. Is this the beginning of the end for any attempt by the non-Chinese world to catch up? No, we’ve already reached that point, and what other manufacturing industries in the West are circling the drain?” – Jack Lifton, CMI Co-Chair & Co-Founder

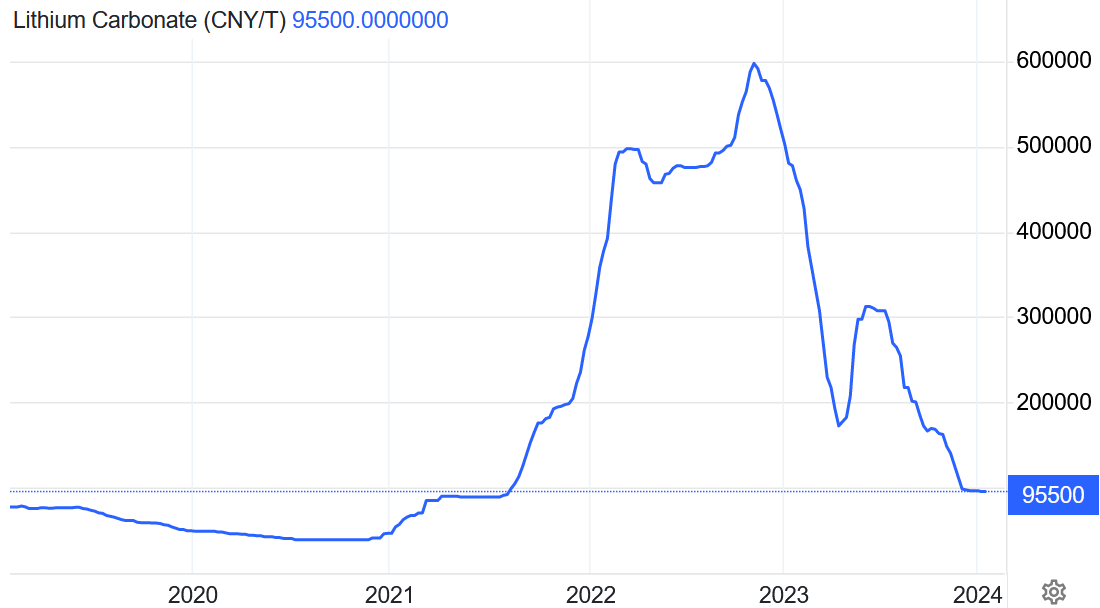

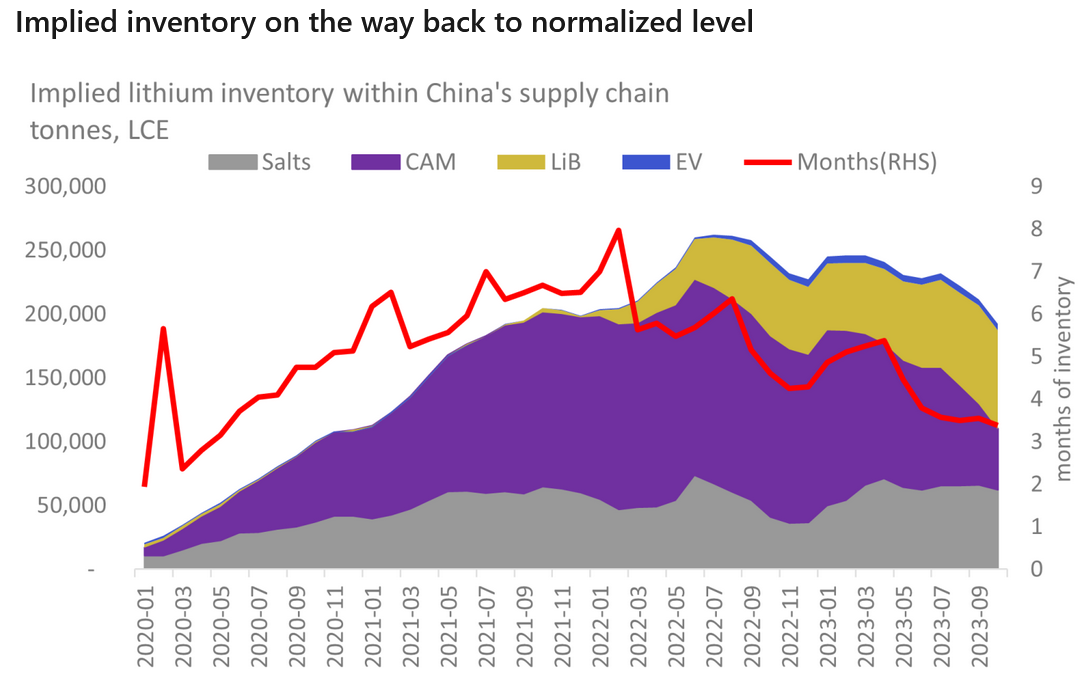

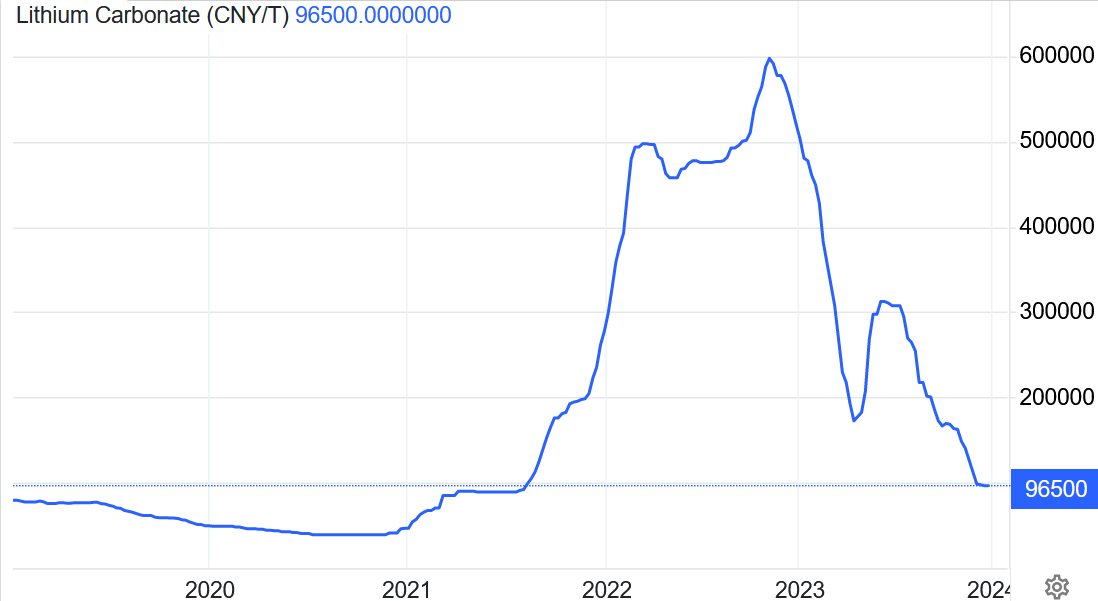

China’s CATL says its lithium mine operating normally (February 22, 2024, Source) — Chinese battery giant Contemporary Amperex Technology Co. (CATL) has confirmed that its lithium mine in Jiangxi province is operating normally, amidst market speculation of a halt due to falling lithium prices. The Jianxiawo mine, rich in hard rock lepidolite and a subsidiary of CATL, faced rumors of reduced or stopped production due to economic challenges. However, CATL asserts production is ongoing as planned, despite market rumors suggesting otherwise. After the Lunar New Year holiday, it was noted that only one of two production lines resumed operation. The mine, which began phase-one production recently, aims for a 200,000 tons capacity of lithium carbonate equivalent (LCE) upon completion of all phases. Despite high production costs compared to current market prices, analysts predict significantly lower output this year than initially expected, with potential delays in future expansion due to these costs. The speculation had earlier boosted Australian lithium stocks.

China’s lithium carbonate futures jump on talk of environmental crackdown (February 21, 2024, Source) — On Wednesday, China’s lithium carbonate futures prices experienced a significant rally, driven by market speculation regarding potential environmental inspections in a key production area. This speculation raised concerns about possible output restrictions, leading to a 6.35% increase in the most-active July contract on the Guangzhou Futures Exchange, reaching 99,600 yuan per metric ton. Speculation centered around Yichun, a major lithium production city in Jiangxi province, facing environmental checks that could limit operations for producers failing to properly manage lithium slag. Despite these rumors, major producers in Jiangxi continued their operations as planned, with some undergoing scheduled maintenance. The price surge, reflecting concerns over supply constraints, followed a rally in Australian lithium stocks prompted by rumors that Chinese battery maker CATL had closed its Jianxiawo mine.

Yellen to Visit Chile in Push to Boost Ties on Critical Minerals (February 21, 2024, Source) — US Treasury Secretary Janet Yellen is scheduled to visit Chile next week as part of an effort to strengthen the United States’ ties with Chile, focusing on the South American nation’s significant role in the green transition through its contribution to renewable energy policies and as a supplier of critical minerals. This visit is a strategic move by the US to diversify its critical minerals supply chain and reduce its dependence on China, which currently leads the market for essential metals necessary for energy transition technologies. Chile, possessing one of the world’s largest lithium reserves, is seeking foreign investment to expand its capacity within the global battery supply chain. The visit, which follows Yellen’s attendance at a G20 finance ministers’ meeting in Sao Paulo, aims to deepen bilateral economic relations, particularly in the context of Chile’s potential to benefit from President Biden’s green stimulus program due to a free-trade agreement with the US, thereby supporting North American electric vehicle production.

Tesla’s price cuts are driving down car values so much that EV makers are sending checks to leasing firms to compensate them (February 21, 2024, Source) — Tesla’s price reductions have significantly lowered the resale value of used electric vehicles (EVs), prompting automakers to issue compensation to leasing companies like Ayvens to cover these losses. This adjustment comes as the industry is pushed to sell more EVs to avoid fines, with leasing firms seeking protections against further depreciation in the $1.2 trillion second-hand car market. The demand for used EVs fell due to Tesla’s price cuts, affecting companies that play a vital role in the corporate car market. To mitigate risks of depreciation, negotiations for buyback agreements and re-leasing options are underway. Regulatory pressures for lower fleet emissions compound the issue, as unstable used-EV pricing challenges the transition to electric mobility by 2035. Corporate shifts, like SAP SE discontinuing Teslas for employees, underscore the broader impacts of volatile EV pricing on the industry.

Biden’s EV Dreams Are a Nightmare for Tesla and the US Car Industry (February 20, 2024, Source) — The Inflation Reduction Act (IRA), initiated by President Joe Biden to foster a US-centric electric vehicle (EV) supply chain and reduce reliance on Chinese components, poses significant challenges for Tesla and other American car manufacturers. Despite Tesla’s initial steps towards compliance, including sourcing batteries from within the US and building a lithium refinery in Texas, the company’s substantial procurement of Chinese lithium-ion batteries underscores the complexity of shifting away from China’s supply network. The IRA mandates stringent sourcing requirements for battery components and raw materials, aiming to cut China’s dominance in the EV sector. However, these measures have compelled carmakers to navigate a difficult transition, risking the affordability and competitiveness of EVs. As Tesla, GM, Ford, and others strive to adapt to these evolving standards and develop alternative supply chains, they face the daunting task of balancing economic, environmental, and strategic objectives in a rapidly changing global market dominated by geopolitical tensions and the strategic distribution of critical minerals.

Goldman, hedge funds step up activity in physical uranium as prices spike (February 20, 2024, Source) — Investment banks Goldman Sachs and Macquarie, along with some hedge funds, are increasingly engaging in the uranium market, driven by a spike in uranium prices to 16-year highs. While many banks remain cautious, these institutions are actively trading physical uranium and, in Goldman’s case, its options. This shift is fueled by utilities’ need for new supplies amid shortages. The interest in uranium is also growing among hedge funds and financial institutions, a notable change after the sector’s stagnation post-Fukushima disaster. Uranium prices have doubled over the past year, reaching $102 a pound, prompted by production cuts from top producers and a renewed interest in nuclear energy as a means to reduce carbon emissions. Goldman Sachs has also introduced options on physical uranium for hedge funds, marking a significant development in the market. This increased activity reflects a broader appeal of uranium to financial investors, with notable investments in physical uranium as well as equities related to the sector.

Gecamines plans overhaul of mining JVs in world’s top cobalt supplier (February 20, 2024, Source) — Gecamines, the state miner of the Democratic Republic of Congo, is seeking to renegotiate terms of its copper and cobalt joint ventures to increase its stakes and gain more control. Aiming to leverage global demand for minerals essential for the green energy transition, Gecamines plans to secure better off-take contracts and ensure local representation on venture boards for improved asset management. The strategy addresses past oversights, focusing on rectifying prolonged indebtedness and insufficient investment by some partners. Recent deals, like the one with China’s CMOC Group, exemplify Gecamines’ efforts towards securing equitable terms, demonstrating a push for enhanced returns, community benefits, and transparency in the world’s top cobalt supplier and a leading copper producer.

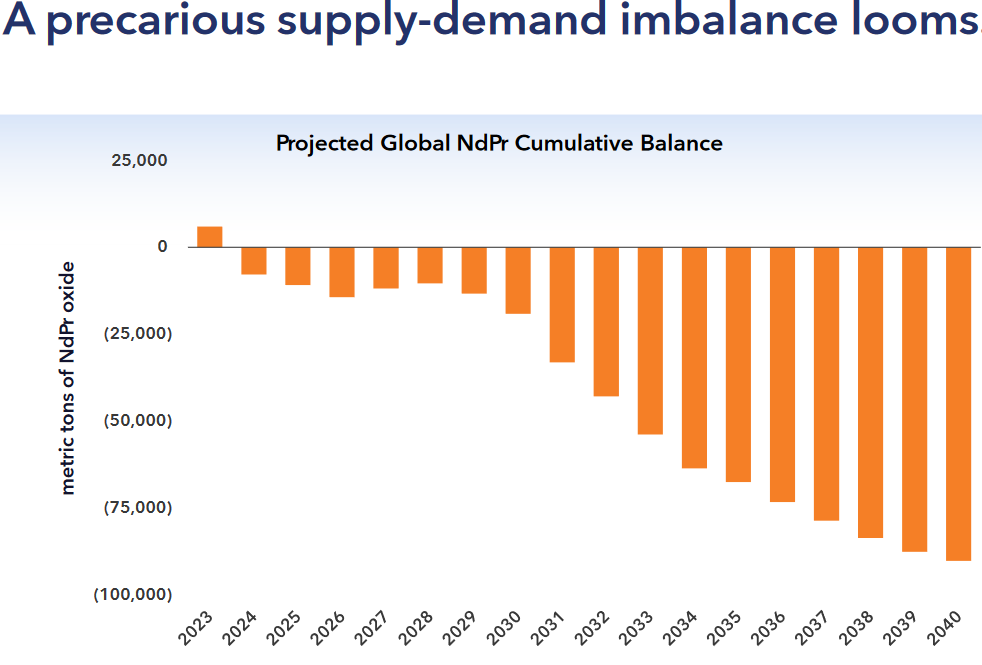

Industry Leaders Lifton and Karayannopoulos China’s Influence on Rare Earth Prices and Markets Today (February 19, 2024, Source) — In an insightful interview, Jack Lifton and Constantine Karayannopoulos delve into the complexities of the rare earths market. Karayannopoulos, wary of current market trends, notes a decline in prices for key elements like neodymium and praseodymium and maintains a cautious outlook due to the industry’s cyclical nature. Lifton points out the impact of China’s economic struggles on low rare earth prices, advocating for strategic investments in mining and processing at this juncture. Both experts discuss the discrepancy between market expectations and reality, particularly in the context of China’s economic growth and the slower-than-anticipated expansion of its magnet industry, vital for electric vehicle production. They emphasize the significance of investing in raw materials and processing to navigate and leverage China’s market dominance effectively, offering a comprehensive view on economic trends, geopolitical strategies, and investment opportunities in the rare earths sector.

BHP says Australian support for nickel miners ‘may not be enough’ to save industry (February 19, 2024, Source) — BHP Group (ASX: BHP | NYSE: BHP) warned that Australian government efforts to support the nickel industry might not suffice amid challenges, as a write-off in its nickel operations led to a nearly 90% drop in first-half net profit. The crisis in Australia’s nickel industry is due to a price collapse from a supply glut in Indonesia. Despite government measures like production tax credits and royalty relief, BHP’s CEO, Mike Henry, suggested these might be inadequate due to structural market changes. BHP, facing a $3.5 billion pre-tax impairment charge on its Nickel West operation, is contemplating suspending its activities there, despite healthy nickel demand from the electric vehicle sector. However, Henry highlighted copper, potash, and iron ore as stronger growth areas for BHP. The company announced a higher-than-expected interim dividend, reflecting robust copper and iron ore performance, and anticipates stability in commodity demand from China and India.

US Bid to Loosen China’s Grip on Key Metals for EVs Is Stalling (February 19, 2024, Source) — The U.S. is striving to diminish its reliance on China for crucial metals like gallium and germanium, vital for electric vehicles and military technology. Efforts have been hampered by the diminished efficacy of the U.S. National Defense Stockpile and budget cuts, revealing vulnerabilities to supply shocks. Despite the Biden administration’s initiatives to diversify metal sources through international deals and domestic projects, China’s control over the global metal supply remains strong. Recent legislative reforms aim to enhance strategic stockpiling and procurement flexibility, but challenges in establishing a coherent strategy and securing stable mineral supplies continue. The situation underscores the complex dynamics of global supply chains and the critical nature of these metals for technological and defense applications.

JPMorgan, State Street quit climate group, BlackRock steps back (February 15, 2024, Source) — JPMorgan Chase and State Street’s investment arms exited the Climate Action 100+ coalition, a global investor group advocating for reduced emissions, withdrawing nearly $14 trillion in assets from climate change initiatives. BlackRock scaled back its participation by shifting its membership to its international arm. These moves follow the coalition’s request for members to intensify actions against companies lagging in emission reductions. Despite political pressure from Republican politicians accusing financial firms of antitrust and fiduciary duty breaches, none cited politics as a reason for their departure. State Street cited conflicts with the coalition’s new priorities, which include engaging policymakers and public emission reduction commitments, as misaligned with its independent approach. BlackRock aims to maintain independence while prioritizing climate goals for its clients.

Investor.News Critical Minerals Media Coverage:

- February 22, 2024 – Stalling the American EV Industry: The Unintended Consequences of the Inflation Reduction Act’s Attempt to Bypass China for Critical Minerals https://bit.ly/3T8IpYE

- February 22, 2024 – Revolutionizing Energy Storage with NEO Battery Materials’ Strategic Advances in Silicon Anode Technology https://bit.ly/3T5rO80

Investor.News Critical Minerals Videos:

- Industry Leaders Lifton and Karayannopoulos China’s Influence on Rare Earth Prices and Markets Today https://bit.ly/3SNSuZk

Critical Minerals IN8.Pro Member News Releases:

- February 22, 2024 – American Rare Earths Announces A$13.5m Placement to advance Halleck Creek Project https://bit.ly/3wuU1fB

- February 22, 2024 – First Phosphate Project Receives Letter of Support from Mario Simard, Canadian Parliamentary Deputy for the Riding of Jonquière, Québec https://bit.ly/3SQAP3i

- February 21, 2024 – Nano One Adds 4 More Lithium Battery Manufacturing Patents in Asia – Boosts Total to 40 https://bit.ly/3I6EmFL

- February 21, 2024 – Power Nickel Expands on High Grade Cu-Pd-Pt-Au-Ag Zone 5km northeast of its Main Nisk Deposit https://bit.ly/433eJj3

- February 20, 2024 – American Clean Resources Group Acquires SWIS Community, LLC, an Environmental Water Technology Company https://bit.ly/3T6iSis

- February 20, 2024 – First Phosphate Provides Update on Plans for a Purified Phosphoric Acid Plant at Port Saguenay, Quebec https://bit.ly/4bINVs4

- February 20, 2024 – Western Uranium & Vanadium Receives over $4.6M from Warrant Exercises https://bit.ly/3UI3DxH

- February 20, 2024 – Appia Unveils Significant REE, Cobalt and Scandium Assay Results From 47 RC Drill Holes at the Buriti Target Within Its PCH IAC REE Project, Brazil https://bit.ly/3ST4GIG

- February 20, 2024 – Fathom Nickel Announces the Closing of Its Second and Final Tranche of Private Placement https://bit.ly/3wjSSr7

- February 20, 2024 – Canadian GoldCamps to Earn 50% of Murphy Lake for $10M Exploration Spend https://bit.ly/4bBbtz0

To become a Critical Minerals Institute (CMI) member, click here