Uranium Prices at a 17-Year High, Energy Fuels Rapidly Increases Uranium Production in 2024

As shown in the chart below, the uranium spot price remains at its highest level since 2007, currently at US$106/lb. A combination of supply cutbacks from major uranium producers (Kazatomprom etc) and increased demand has led to a uranium deficit, and higher uranium prices.

The longer term outlook for uranium got a boost in December 2023, when more than 20 countries signed a declaration at COP28 that they would triple their nuclear energy capacity by 2050. Reuters quotes: “Global nuclear capacity now stands at 370 gigawatts, with 31 countries running reactors. Tripling that capacity by 2050 would require a significant scaling up in new approvals – and finance.“

Also of interest is that 118 governments pledged to triple the world’s renewable energy capacity by 2030.

Uranium spot price – 25 year chart

Source: Trading Economics

Energy Fuels is a potential winner as they can rapidly grow their uranium production in the USA

Energy Fuels Inc. (NYSE American: UUUU | TSX: EFR) is the leading uranium producer in the USA and according to the Company have “produced 2/3 of all U.S. uranium since 2017”.

Energy Fuels state their goal as: “To create a profitable, high-margin U.S. critical mineral company –centered on uranium – that produces advanced materials needed for the clean energy transition.” Energy Fuels already produces uranium, vanadium, and rare earths (via processing).

Short-term uranium production plans

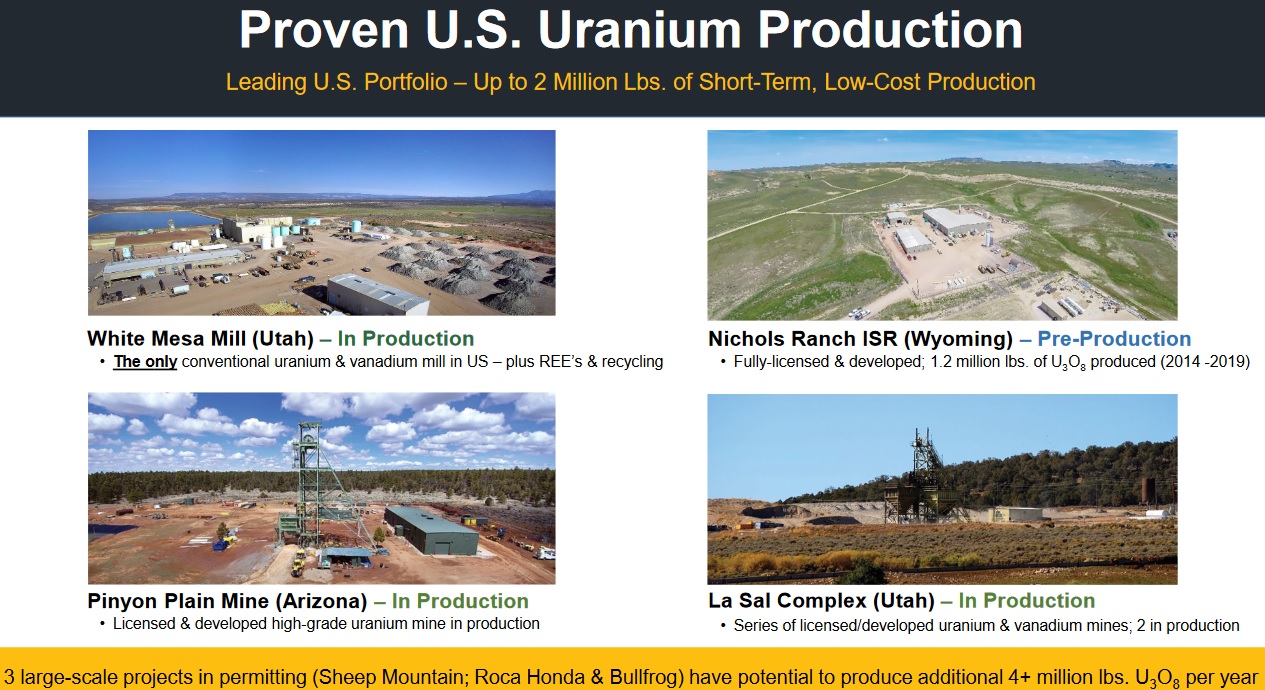

As announced on December 21, 2023, in response to strong uranium market conditions, Energy Fuels has commenced uranium production at 3 of its permitted and developed uranium mines located in Arizona and Utah (Pinyon Plain Mine, La Sal Mine at La Sal Complex, and Pandora Mine at La Sal Complex). Energy Fuels targets a run rate of 1.1 – 1.4 million lbs. of U3O8 pa from these mines by the end of 2024.

Next Energy Fuels is preparing 2 additional uranium mines for production, including the Whirlwind Mine (Colorado) and the Nichols Ranch ISR Facility (Wyoming) within 1 year; which combined have short-term potential to produce an additional 300-600,000 lbs. of U3O8 pa.

Energy Fuels is targeting to reach total uranium production of over ~2 million lbs. of low-cost production in the short-term (in 2025).

Energy Fuels is also evaluating total finished uranium production in 2024 from alternate feed materials of an additional 100-400,000 lbs. of U3O8 pa.

Energy Fuels targets to reach over 2 million lbs of low cost uranium production in 2025

Source: Energy Fuels company presentation

Energy Fuels is guiding that they expect 200,000 lbs. of U3O8 sales in 2024 under long-term contracts, plus potential to sell additional uranium on spot market.

Looking out a bit further, Energy Fuels has 3 large scale projects in permitting (Sheep Mountain, Roca Honda, Bullfrog) that have the potential to produce an additional 4+ million lbs. U3O8 pa in the mid-term.

Closing remarks

Energy Fuels is clearly set to have a huge year in 2024 as they focus to significantly ramp up uranium production (and commission Phase 1 of their NdPr production). In regards to uranium pricing, Energy Fuels uses a pricing formula which maintains exposure to the upside, while limiting downside and adjusting for inflation. They are also seeking additional spot sales and long term contracts as prices rise. Longer term Energy Fuels say they have licensed capacity to reach “over 10 million pounds of U3O8 per year” which is more capacity than any other U.S. company.

Energy Fuels trades on a market cap of US$1.075 billion and a PE ratio (TTM) of 10.31.