Greg Fenton on China’s graphite export restrictions and Zentek’s Albany graphite deposit in Ontario

written by InvestorNews | October 26, 2023

In a recent InvestorNews interview with host Tracy Weslosky, Zentek Ltd.‘s (NASDAQ: ZTEK | TSXV: ZEN) CEO and Director, Greg Fenton, discussed China’s recent move to restrict graphite exports and its potential impact on global supply chains and the electric vehicle (EV) industry.

Concerns about China’s dominance in supplying critical minerals to the EV industry have prompted governments to identify this as a significant risk. Greg said that the recent restrictions on graphite exports highlight the importance of creating a North American battery supply chain. Greg underscored the potential for this situation to significantly alter the EV landscape. Foreseeing long-term growth, Greg discussed why electric vehicle manufacturers will need to diversify their supply chains away from China.

Greg believes these restrictions will shift the focus to North American graphite producers. Highlighting Zentek’s Albany graphite deposit in Ontario, Canada, as a promising source of high-purity graphite, Greg emphasized the need for government and industry investments in North American graphite projects.

Don’t miss other InvestorNews interviews. Subscribe to the InvestorNews YouTube channel by clicking here

About Zentek Ltd.

Zentek is an ISO 13485:2016 certified intellectual property technology company focused on the research, development and commercialization of novel products seeking to give the Company’s commercial partners a competitive advantage by making their products better, safer, and greener.

Zentek’s patented technology platform ZenGUARD™, is shown to have 99-per-cent anti-microbial activity and to significantly increase the bacterial and viral filtration efficiency of both surgical masks and HVAC (heating, ventilation, and air conditioning) systems. Zentek’s ZenGUARD™ production facility is located in Guelph, Ontario.

Zentek has a global exclusive license to the Aptamer-based platform technology developed by McMaster University which is being jointly developed Zentek and McMaster for both the diagnostic and therapeutic markets.

Disclaimer:Zentek Ltd. is an advertorial member of InvestorNews Inc.

This interview, which was produced by InvestorNews Inc. (“InvestorNews”), does not contain, nor does it purport to contain, a summary of all material information concerning the Company, including important disclosure and risk factors associated with the Company, its business and an investment in its securities. InvestorNews offers no representations or warranties that any of the information contained in this interview is accurate or complete.

This interview and any transcriptions or reproductions thereof (collectively, this “presentation”) does not constitute, or form part of, any offer or invitation to sell or issue, or any solicitation of any offer to subscribe for or purchase any securities in the Company. The information in this presentation is provided for informational purposes only and may be subject to updating, completion or revision, and except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any information herein. This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein.

Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. This presentation should not be considered as the giving of investment advice by the Company or any of its directors, officers, agents, employees or advisors. Each person to whom this presentation is made available must make its own independent assessment of the Company after making such investigations and taking such advice as may be deemed necessary. Prospective investors are urged to review the Company’s profile on SedarPlus.ca and to carry out independent investigations in order to determine their interest in investing in the Company.

Can the Western graphite and anode industry rise to meet China’s challenge?

written by Matt Bohlsen | October 26, 2023

China to impose some graphite and processed graphite materials ‘export permits’ from December 1, 2023

Last week it was reported that China, the world’s top graphite producer plans to curb exports of key battery material by implementing export permits for some graphite products from December 1 to protect national security. Another report stated: “China graphite export restrictions could hinder ex-China anode development….if it lasts into the longer term, it is likely to accelerate the build-out of a localized graphite and battery anode supply chain outside China.”

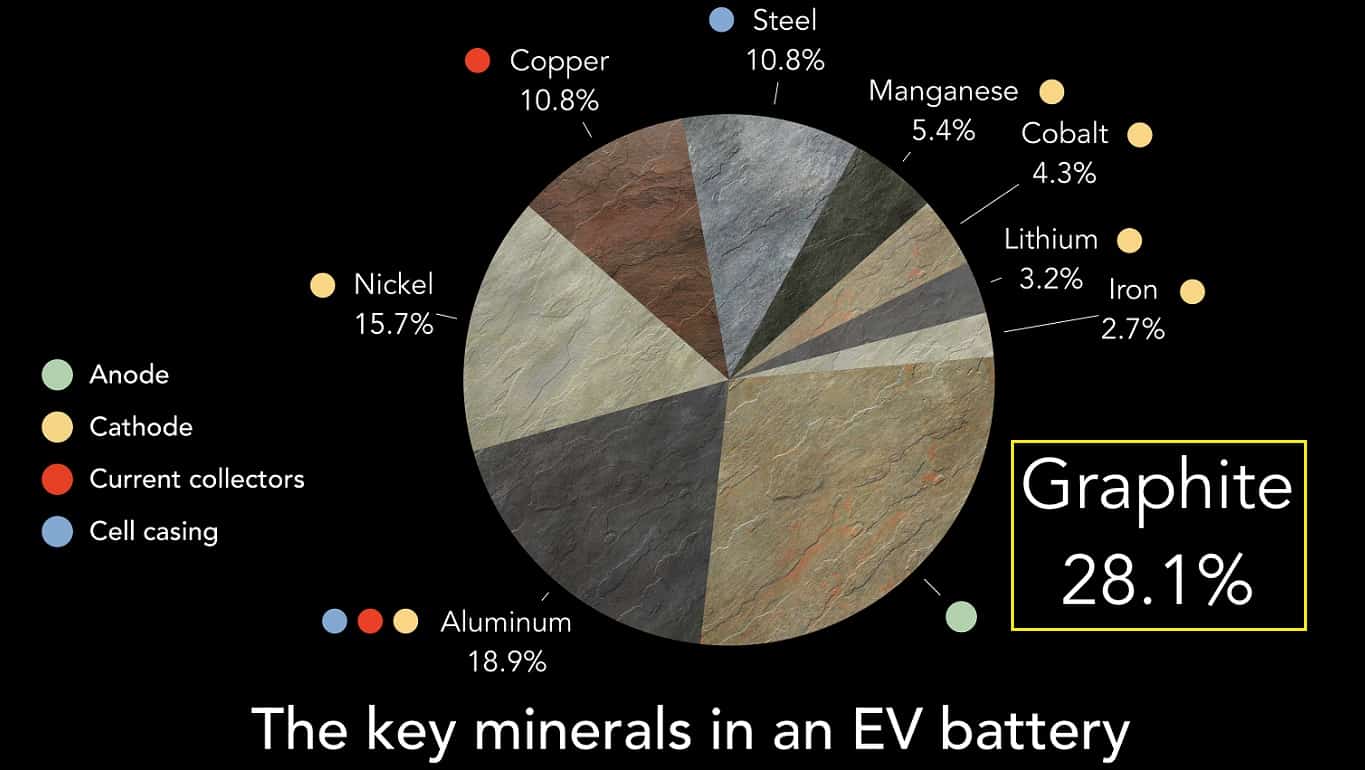

Graphite is the number one metal required for lithium-ion batteries making up about a 28% share. It is used in the anode.

The key metals and minerals in a battery of an electric vehicle

The world is very dependent upon China to supply processed graphite material and anodes for Li-ion batteries

The reason why this is huge news in the graphite world is that China produces 67% of global natural flake graphite supply and refines more than 90% of the world’s graphite into active anode material (typically spherical graphite). If China were to deny or delay permits for spherical graphite it will cause major problems for anode manufacturers outside China, such as those in South Korea, Japan, or North America.

China currently produces ~77% of global lithium-ion batteries and 75-80% of global electric cars, thereby completely dominating the industry. If the West is shut out from sourcing processed EV battery materials from China then they will have a major problem producing their own EVs. China plans to prioritize EV battery materials for their own needs. This is why President Biden introduced the Inflation Reduction Act (IRA) and the EU introduced the EU Critical Raw Materials Act. Both are designed to address the shortages in the EV supply chain and the forecast shortages of future supply of critical raw materials. The problem is the IRA has done little to address the supply of raw materials and the EU Critical Raw Materials Act is woefully inadequate and targets fall way short of what will be needed.

Which western graphite companies can rise to meet the challenge to establish an ex-China graphite supply chain

The leading western graphite companies that are working to establish an ex-China supply chain for flake graphite, synthetic graphite, and spherical graphite include:

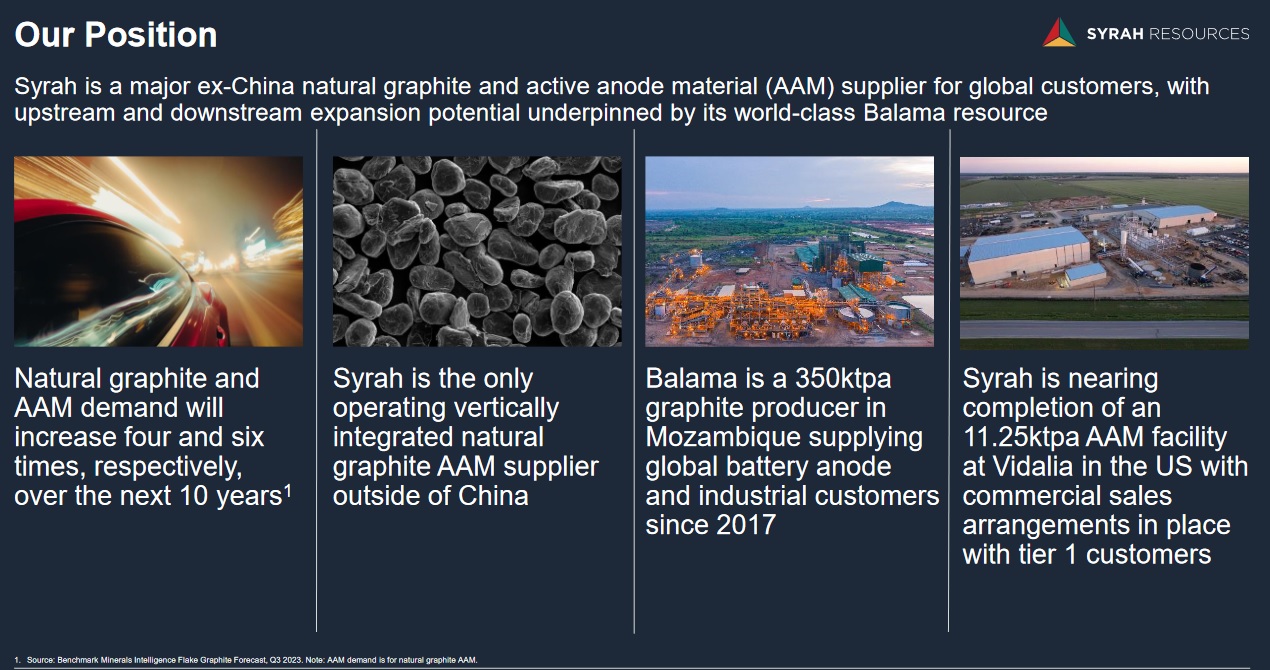

Syrah Resources Limited (ASX: SYR) – Largest western flake graphite producer with their 350,000tpa flake graphite capacity Balama Mine in Mozambique. Currently constructing the Vidalia spherical graphite facility in Louisiana, USA with Stage 1 production plans to produce 11,250tpa of spherical graphite. Longer term they plan to expand to 45,000tpa in 2026 and then to >100,000tpa by 2030 with an Europe/Middle East facility. Syrah already has an off-take agreement with Tesla (NASDAQ: TSLA). Syrah’s stock price has surged ~80% higher the past week following the release of the China export permits news.

Nouveau Monde Graphite Inc. (NYSE: NMG | TSXV: NOU) – Is rapidly progressing their plans for their Matawinie Graphite Mine and Bécancour Battery Anode Material Plant in Quebec, Canada. The company is working with Panasonic to qualify their graphite anode material. Panasonic supplies Tesla with batteries.

Northern Graphite Corporation (TSXV: NGC | OTCQB: NGPHF) – Owns graphite producing and past producing mines in Quebec, Canada and Namibia. They also own the Bissett Creek graphite Project in Ontario, Canada. The Company state that they are “North America’s Only Significant Natural Graphite Producer”. The Company plans to develop one of the world’s largest battery anode materials facilities in Baie-Comeau Québec with 200,000tpa of capacity.

NextSource Materials Inc. (TSX: NEXT | OTCQB: NSRCF) – A new graphite producer from their Molo Graphite Mine in Madagascar with Phase 1 capacity of 17,000tpa of flake graphite production and plans to expand to 150,000tpa. The Company’s short term plan is for a Battery Anode Facility in Mauritius and longer term for similar facilities in USA/Canada, UK, EU.

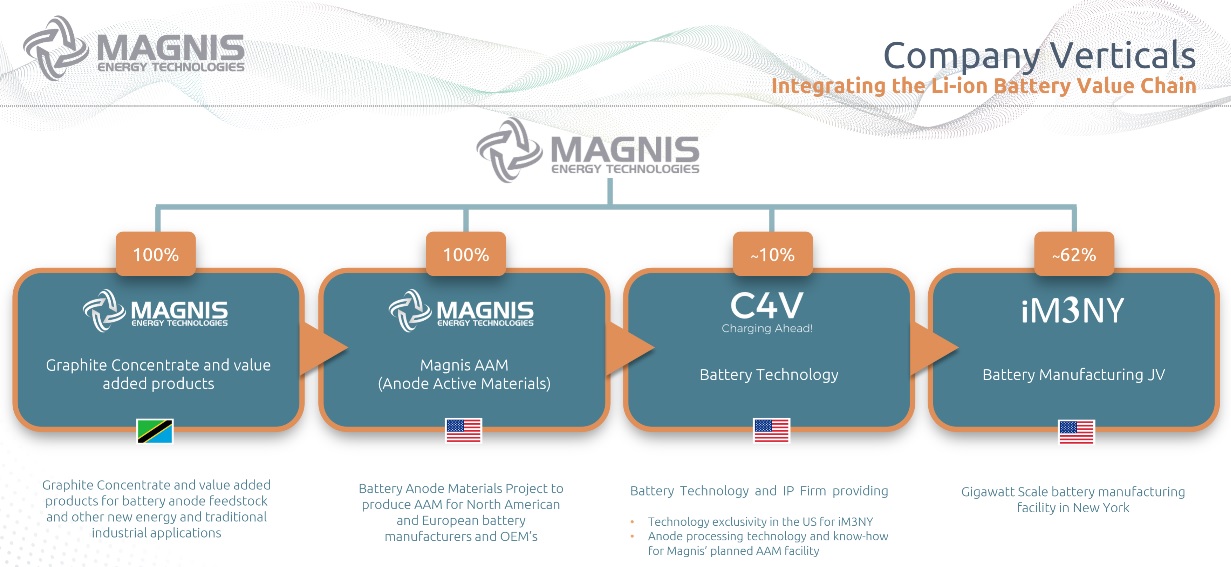

Magnis Energy Technologies Ltd. (ASX: MNS | OTCQX: MNSEF) – Magnis aims to produce high performance anode materials utilising ultra-high purity natural flake graphite from their Nachu Graphite Project in Tanzania. Magnis’ partially owned U.S.-based subsidiary Imperium3 New York, Inc (“iM3NY”) operates a gigawatt scale lithium-ion battery manufacturing project in Endicott, New York.

Talga Group Ltd. (ASX: TLG) – Own the integrated mine to anode Vittangi Graphite Project in Sweden. In September 2023 Talga broke ground on their 19,500tpa anode facility, stating “the refinery is projected to be the first commercial anode production in Europe for electric vehicle Li-ion batteries”.

Novonix Limited (NASDAQ: NVX | ASX: NVX) – Has a production capacity target of up to 20,000 tpa of synthetic graphite anode material from their Tennessee facility in the USA.

Magnis Energy Technologies is working towards becoming a graphite producer, anode materials producer and is already a small scale JV battery producer in the USA

The Western world received a loud wake-up call the past week. The China graphite products ‘export permits’ may only serve to restrict or slow down some anode material supply from China, but it puts the West on notice of how dependent they are upon China.

Given the world is rapidly moving to electric vehicles, the West must urgently build up its EV materials supply chains or risk being left behind in the global EV race.

The USA is making some bold moves and the companies discussed in this article are moving in the right direction. Let’s just hope that the western EV supply chain build out accelerates rather than stalls like GM’s latest electric pickup truck plans. I think Americans will want U.S.-branded electric cars and I know Europeans will want European branded electric cars. If we are not careful our only choice one day might be Tesla and Chinese electric cars. Stay tuned.

Nouveau Monde’s Eric Desaulniers on China’s Decision to Restrict the Export of Graphite

written by InvestorNews | October 26, 2023

In a recent episode of InvestorNews, Tracy Weslosky sat down with Eric Desaulniers, MSc, Géo, President & CEO of Nouveau Monde Graphite Inc. (NYSE: NMG | TSXV: NOU), to discuss China’s surprising decision to implement export permits for certain graphite products starting December 1st. Eric remarked, “Waking up to this news was unexpected, but not entirely surprising. China’s decision to restrict the export of battery materials, starting with graphite, comes sooner than many experts anticipated.”

With the booming demand for electric vehicles, which require five times more graphite than any other critical mineral, Tracy delved into the implications of China’s move on graphite supply. Eric highlighted China’s dominant position, controlling nearly 100% of natural graphite processing. “This strategic decision by China impacts many companies in the U.S. that are scaling up cell production,” he said. He was proud to mention that Nouveau Monde stands out, developing one of the largest and most sophisticated natural graphite operations outside of China.

The changing dynamics are also influencing Nouveau Monde’s partnerships, particularly with giants like Panasonic. The recent developments have intensified their ongoing discussions. As Eric pointed out, the challenge will be detaching from China’s supply chain, especially amid skyrocketing cell production demand. “Our goal is to be a viable alternative, and this current pricing scenario outside China underscores the need for that,” Eric emphasized.

Don’t miss other InvestorNews interviews. Subscribe to the InvestorNews YouTube channel by clicking here

About Nouveau Monde Graphite Inc.

Nouveau Monde Graphite is striving to become a key contributor to the sustainable energy revolution. The Company is working towards developing a fully integrated source of carbon-neutral battery anode material in Québec, Canada, for the growing lithium-ion and fuel cell markets. With enviable ESG standards, NMG aspires to become a strategic supplier to the world’s leading battery and automobile manufacturers, providing high-performing and reliable advanced materials while promoting sustainability and supply chain traceability.

To know more about Nouveau Monde Graphite Inc., click here

Disclaimer: This interview, which was produced by InvestorNews Inc. (“InvestorNews”), does not contain, nor does it purport to contain, a summary of all material information concerning the Company, including important disclosure and risk factors associated with the Company, its business and an investment in its securities. InvestorNews offers no representations or warranties that any of the information contained in this interview is accurate or complete.

This interview and any transcriptions or reproductions thereof (collectively, this “presentation”) does not constitute, or form part of, any offer or invitation to sell or issue, or any solicitation of any offer to subscribe for or purchase any securities in the Company. The information in this presentation is provided for informational purposes only and may be subject to updating, completion or revision, and except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any information herein. This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein.

Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. This presentation should not be considered as the giving of investment advice by the Company or any of its directors, officers, agents, employees or advisors. Each person to whom this presentation is made available must make its own independent assessment of the Company after making such investigations and taking such advice as may be deemed necessary. Prospective investors are urged to review the Company’s profile on SedarPlus.ca and to carry out independent investigations in order to determine their interest in investing in the Company.

5 Stocks on the Radar Amid China’s Graphite Export Ban

written by Tracy Weslosky | October 26, 2023

Recent developments from China’s Ministry of Commerce concerning export permits on critical graphite products have sent ripples through the financial markets. Graphite, indispensable for electric vehicle (EV) batteries, is now under tighter control by China, a country that dominates its global production.

“Graphite content in an electric vehicle exceeds the demand for any other critical mineral fivefold. We’ve observed China make similar business maneuvers with rare earths, germanium, gallium, and now graphite. This trajectory was anticipated. While I concur with CMI’s Jack Lifton on lithium or cobalt possibly being next, we shouldn’t overlook vanadium.”

“The EV boom is creating a surge in demand for graphite… Each fully electric car battery has between 60-100kgs of graphite. China’s proposed ‘export permits’ will likely lead to a shortage of spherical and synthetic graphite outside of China, underscoring the world’s vulnerability to China’s supply disruption of critical minerals.”

Investors are now unquestionably watching stocks that might benefit the global market in light of the challenges presented by yet another China C Critical Mineral export ban. Here are five stocks that we were researching this morning (listed by market cap):

1: Syrah Resources Limited (ASX: SYR) – Market Cap: AUD$307.53M* — Syrah is an Australian Securities Exchange listed industrial minerals and technology company with its flagship Balama Graphite Operation in Mozambique and a downstream Active Anode Material Facility in the United States. Syrah’s vision is to be the world’s leading supplier of superior quality graphite and anode material products, working closely with customers and the supply chain to add value in battery and industrial markets.

2: Talga Group Ltd. (ASX: TLG) – Market Cap: AUD$353.53M* — Talga Group Ltd. is building a European battery materials supply chain to offer products critical to the green transition. Talga’s innovative technology and vertical integration of 100% owned Swedish graphite resources provides security of supply and creates additional value for stakeholders.

Zentek is an ISO 13485:2016 certified intellectual property technology company focused on the research, development and commercialization of novel products seeking to give the Company’s commercial partners a competitive advantage by making their products better, safer, and greener.

Zentek’s patented technology platform ZenGUARD™, is shown to have 99-per-cent anti-microbial activity and to significantly increase the bacterial and viral filtration efficiency of both surgical masks and HVAC (heating, ventilation, and air conditioning) systems. Zentek’s ZenGUARD™ production facility is located in Guelph, Ontario.

Zentek has a global exclusive license to the Aptamer-based platform technology developed by McMaster University which is being jointly developed Zentek and McMaster for both the diagnostic and therapeutic markets.

Zentek is also the 100% owner of Albany Graphite Corp. (AGC). AGC’s recently filed 43-101 Mineral Resource Estimate shows circa 1,000,000 tonnes of graphite in Ontario. Importantly, that graphite is volcanic of origin, and globally unique. It is expected that graphite from AGC will perform better in EV batteries than other materials because of the volcanic origin.

Nouveau Monde Graphite is striving to become a key contributor to the sustainable energy revolution. The Company is working towards developing a fully integrated source of carbon-neutral battery anode material in Québec, Canada, for the growing lithium-ion and fuel cell markets. With enviable ESG standards, NMG aspires to become a strategic supplier to the world’s leading battery and automobile manufacturers, providing high-performing and reliable advanced materials while promoting sustainability and supply chain traceability.

Northern is a Canadian, TSX Venture Exchange listed company that is focused on becoming a world leader in producing natural graphite and upgrading it into high value products critical to the green economy including anode material for Lithium-Ion batteries/EVs, fuel cells and graphene, as well as advanced industrial technologies.

Northern is the only graphite producing company in North America and will become the third largest producer outside of China when its Namibian operations come back online. The Company has the large scale Bissett Creek development project in Ontario that will be a source of continued production growth in the future. All projects have “battery quality” graphite and are located close to infrastructure in politically stable jurisdictions.

(*) Market cap figures were sourced from the ASX, TSX, and Yahoo Finance Boards as of market opening on Friday, October 20, 2023. The listed market caps are in millions.

Amid these market shifts, it is pivotal for investors to stay updated and understand the dynamics affecting graphite and related stocks in the critical minerals sector. As China tightens its control over graphite exports, these companies and the wider EV sector will be in sharp focus, making it a space to watch closely in the coming months.

China’s Tightening Control over the Global Graphite Market

written by Tracy Weslosky | October 26, 2023

China’s Ministry of Commerce has announced that, effective December 1, export permits will be mandated for specific graphite products, citing national security reasons. Graphite, a pivotal component for electric vehicle (EV) batteries, finds China at its epicenter, producing 67% of the global supply of natural graphite. Additionally, China refines over 90% of the world’s graphite, which is integral to almost all EV battery anodes.

This decision unfolds in a backdrop of escalating tensions and increasing scrutiny from foreign nations. The European Union is considering tariffs on EVs originating from China, attributing unfair advantages due to state-backed subsidies. Concurrently, the U.S. has broadened its restrictions on Chinese firms accessing semiconductors and has prohibited the sale of advanced AI chips by Nvidia to Chinese companies.

The new regulatory framework targets two primary graphite types for export permits: high-purity synthetic graphite and natural flake graphite. This is reminiscent of earlier controls over “highly sensitive” graphite products, which are now integrated into the updated regulations. Analogous constraints were previously placed on semiconductor metals, gallium and germanium, which witnessed a marked reduction in exports from China.

Even though the U.S. and Europe are venturing into the graphite domain to counteract China’s monopoly, experts forecast a formidable path ahead. The central graphite importers from China currently include Japan, India, and South Korea.

These developments occur as the EV market is on an upward trajectory, with sales surging past 10 million units the previous year and predictions hovering around 14 million for the current year. This booming sector has amplified the demand for graphite, with the global market for battery use expanding by 250% since 2018. China’s contribution was a colossal 65% of the total production in the past year.

The growing EV market accentuates the criticality of raw materials like graphite. As China further consolidates its hold on the graphite industry, potential ramifications for the global EV landscape are imminent.

Right after writing this summary, I was able to reach Jack Lifton, Co-Chairman of the Critical Minerals Institute, to delve deeper into the repercussions and intricacies of these developments.

Lifton’s perspective on China’s recent announcements was direct: “This isn’t fundamentally about national security. It’s a manifestation of China’s discontent with the West’s ongoing rhetoric of reducing dependence and risks associated with their supply chain.” Lifton highlighted China’s pivotal role in graphite anode processing, suggesting that the dream of a rapid shift to EVs in the West could remain elusive without China’s involvement.

Addressing the challenges to China’s manufacturing supremacy, Lifton commented, “For years, the West prioritized cost-cutting, and China emerged as the answer. Today, the tables have turned, and the West is waking up to the consequences of its over-reliance on Chinese supply chains.”

On the topic of recent restrictions, Lifton opined, “China is fortifying its position in the critical minerals sector. The reality is that with China’s stronghold, the anticipated rapid transition of the West to EVs is looking increasingly optimistic.”

When quizzed about what minerals might be next in line, Lifton’s prediction was clear: “Post rare earths and graphite, my money would be on lithium or cobalt. The West’s ambitions for the EV transition are simply too vast for its current resources without China’s involvement.”

The Critical Minerals Institute October Report: A slowing global economy continues to temper demand

written by Matt Bohlsen | October 26, 2023

Welcome to the October 2023 Critical Minerals Institute (“CMI”) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the IEA list of Critical Minerals.

A slowing global economy continues to temper demand for critical minerals in 2023

High interest rates in most Western countries continue to be a drag on the global economy. Last month saw the U.S. Fed pause their interest rate hikes, with the reserve rate still at 5.5%. However, U.S. inflation has been rising again and the Fed has indicated rates will need to stay higher for longer. The September CPI was 3.7%, same as August’s 3.7%, but up on the July 3.2% figure. Long-term bond rates have adjusted higher leading to higher borrowing rates. All of this is slowing the U.S. and much of the global economy therefore not helping EV sales. China’s housing collapse is another negative drag on sentiment and has resulted in slower China EV sales growth in 2023.

Global critical minerals and electric vehicle (“EV”) update

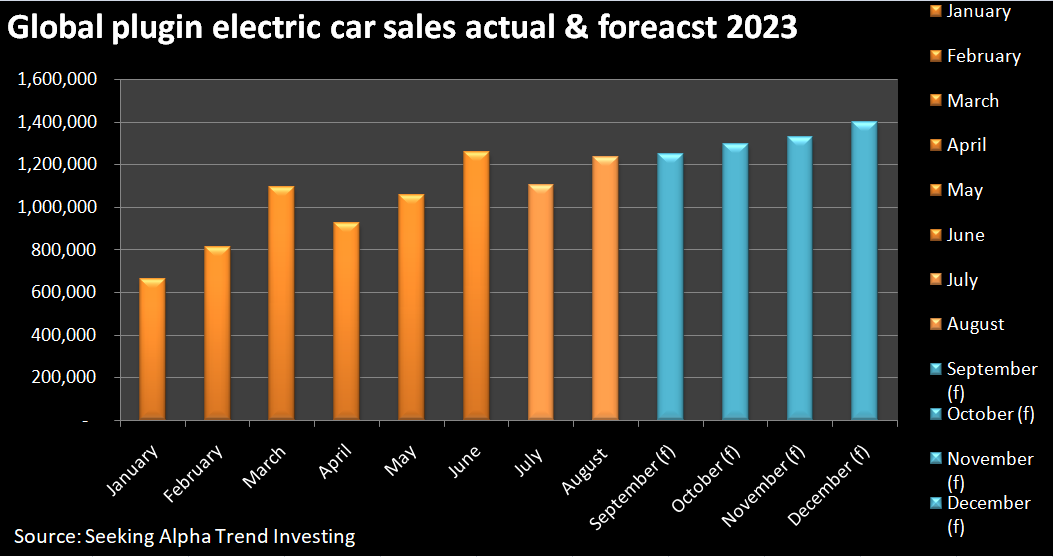

October 2023 saw some better results coming in for global plugin electric car sales which gives some hope that depressed EV metals prices may soon start to recover. Q4 is traditionally the strongest quarter for EV sales with December usually the best sales month of the year.

Global plugin electric car sales were 1,238,000 in August 2023, up 45% on August 2022 sales. Global plugin electric car market share in August was 18%, led by China with 39% share, Europe with 30% share, and USA with 9.51% share. Reports to date suggest that September sales look like being another strong month of about 1.25 million.

2023 sales look set to finish at ~13.5 million and 17% market share, which would be a 28% increase on 2022 (10.522 million and 13% market share). A 28% growth rate in 2023 would be a significant slowdown on the 56% growth rate achieved in 2022.

Global plugin electric car ‘monthly’ sales in 2023

The West is working hard to build up EV and battery capacity rather than being too dependent on China

One of the biggest news of the last month was that Quebec, Canada is in talks with battery makers and automobile companies looking to invest about C$15 billion (US$11 billion) in Quebec over the next three years to support EV supply chains. The report stated:

“Quebec has secured C$15 billion over the past three years and another C$15 billion is coming in the next three years…Over the past three years, Quebec has attracted investments from auto and battery makers such as General Motors, POSCO and Ford Motors. The biggest investment was announced on Thursday when Swedish battery maker Northvolt announced plans to build a $5.2 billion plant in the province.”

While this is good news for the EV and battery manufacturers it does nothing to support the mining industry. It is similar to the U.S. Inflation Reduction Act, where most funds are going to auto and battery companies and very little to the upstream miners. This will only boost demand for critical minerals needed to feed the EV and energy storage booms. Very little is being done to address the looming supply deficits of these critical materials in the second half of the decade.

For example, there are 18 gigafactories planned to be built in the USA this decade, requiring 715,000tpa of lithium, but only 180,000tpa is currently planned. Similar mismatches of supply and demand exist in the pipeline for several other critical metals. Europe’s critical minerals supply chain looks even more dire.

China continues to dominate the EV and battery manufacturing industry

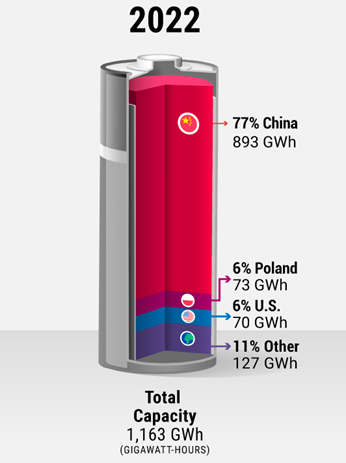

Many people might be unaware that China manufactures ~75-80% of all new global plugin electric cars and ~77% of global lithium-ion batteries. China’s BYD is the world’s largest seller followed by Tesla, who makes over 50% of their cars in China.

In 2022 China had 77% of the lithium-ion battery global capacity

China lithium carbonate spot prices fell so far in October 2023, with the price now at CNY 166,500/t (USD 22,781/t) and down 68% over the past year. At these prices, some of the marginal producers in China have begun shutting down. We did get a glimmer of hope for a bottom this week (mid October) as lithium carbonate futures contracts in Guangzhou jumped by 7% to limit up for the day.

Lithium takeovers and equity interests are a leading trend in mid 2023

The biggest news the past month in the lithium sector has been the fight for control of Australia’s Liontown Resources Limited (ASX: LTR), who 100% own the near production Kathleen Valley Lithium Project in Western Australia. U.S. lithium giant Albemarle Corporation (NYSE: ALB) is currently doing due diligence after upping their offer to A$3.00 per share, or about A$6.6 billion (US$4.23 billion) to purchase all of Liontown Resources. However, in recent weeks Australia’s richest woman, Gina Rinehart, via her controlled company Hancock Prospecting, increased its stake in Liontown to 19.9%. Rinehart’s motives are not yet known but it appears the iron ore magnate has become very interested in lithium.

Only 2-3 months back Albemarle bought a 6.4% stake in Canadian lithium junior Patriot Battery Metals Inc. (TSXV: PMET | ASX: PMT | OTCQX: PMETF). The purchase price paid was C$109 million and it was made just one day after Patriot Battery Metals announced their Maiden Resource of 109.2 Mt @ 1.42% Li2O Inferred, the largest lithium spodumene resource in the Americas. The interesting part is that Patriot Battery Metals market cap is only US$866 million, 4.7x lower than Liontown Resources market cap of US$4.068 billion. Liontown Resources resource is about 50% bigger (156Mt at 1.4% Li2O) and about 4 years more advanced than Patriot Battery Metals Corvette Project. Nonetheless, if Albemarle decides to back away from the Liontown Resources takeover bid then there is a very good chance Albemarle will turn their takeover attention towards Patriot Battery Metals.

Mineral Resources Limited (ASX: MIN) has also been very active in 2023 in the lithium space. In September it was confirmed that Mineral Resources is bidding for the liquidated Bald Hill Lithium Mine. Mineral Resources has also backed Develop Global’s takeover offer for Essential Metals Limited (ASX: ESS) for A$152.6 million (US$101 million), plus Mineral Resources has also bought equity stakes in Delta Lithium Ltd. (ASX: DLI) and Global Lithium Resources (ASX: GL1).

Chile’s SQM (NYSE: SQM) also recently made a takeover offer for Azure Minerals Limited (ASX: AZS) for US$585 million.

All of this takeover activity from the major lithium companies suggests that we are near a bottom in the lithium price cycle and that the mid to long term outlook for lithium remains very strong.

Rare Earths

Rare earths supply disruptions have led to some price improvements recently. Neodymium (“Nd”) prices continued their recent recovery so far in mid October 2023 after a rough 2023, currently sitting at CNY 650,000/t.

Rare earths prices have been falling for most of 2023; however recent supply disruptions in Myanmar have caused most rare earth prices to strengthen. There have also been some reports that Malaysia is developing a policy to ban exports of rare earths raw materials so as to boost their domestic industry. There is no date given yet as to when a ban may start. In any event, Myanmar is a much more important supplier than Malaysia.

This month Australian Strategic Materials Limited (ASX: ASM) announced some world-class test work results with their terbium (Tb) and dysprosium (Dy) heavy rare earth separation test work. Pilot plant test work produced “>99.99% for Tb and > 99.95% for Dy1, at steady state”. Results like this from their Dubbo Project ore should give some more impetus to getting the Dubbo Project financed with probable output of around 140tpa Dy and 20tpa Tb. ASM Managing Director, Miss Rowena Smith stated:

“These excellent results demonstrate the strength of ASM’s advanced technical capability…Terbium and dysprosium oxides are not only scarce commodities they are very difficult to separate at high purity. With the continued expertise of the team at ANSTO and the welcome support of the NSW Government, we are positioning the Dubbo Project to be at the forefront of Australia’s rare earth and critical minerals evolution.”

Dysprosium is a key rare earth used in nuclear reactor control rods and neodymium-iron-boron permanent magnets used in many EVs and wind turbines. Terbium is used in fluorescent lamps and television and monitor cathode-ray tubes.

Cobalt, Graphite, Nickel, Manganese and other critical minerals

Cobalt prices (currently at US$14.84/lb) remained flat the past month and continue to be very depressed. China’s demand for NMC cathode material for EVs has been weak, not helped by the popularity of LFP cathodes that don’t use nickel or cobalt.

Flake graphiteprices remain very weak with prices near the marginal cost of production. A combination of slower EV sales growth in 2023 and increased China graphite supply has led to a depressed graphite market. Macquarie and others forecast graphite to start heading into deficit from about 2024.

Nickelprices have recently weakened further due to oversupply concerns from Indonesia and a slowing Chinese property sector.

Manganeseprices remain weak mostly due to weak Chinese demand as the Chinese housing industry continues to rebalance after years of over construction and oversupply.

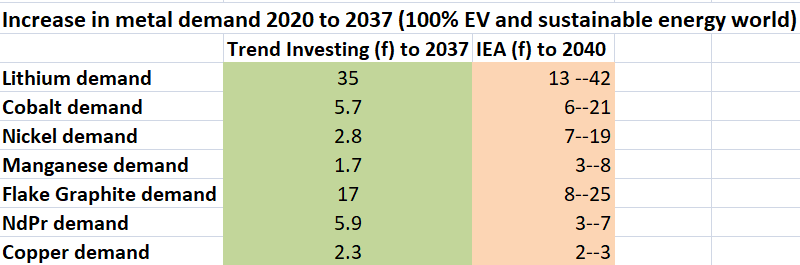

Longer term the outlook for the EV and energy stationary storage (“ESS”) sectors looks extremely strong. This is expected to lead to a huge surge in demand for the critical metals that supply these sectors.

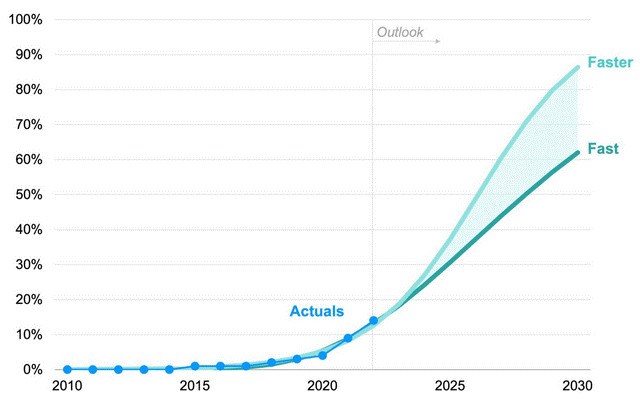

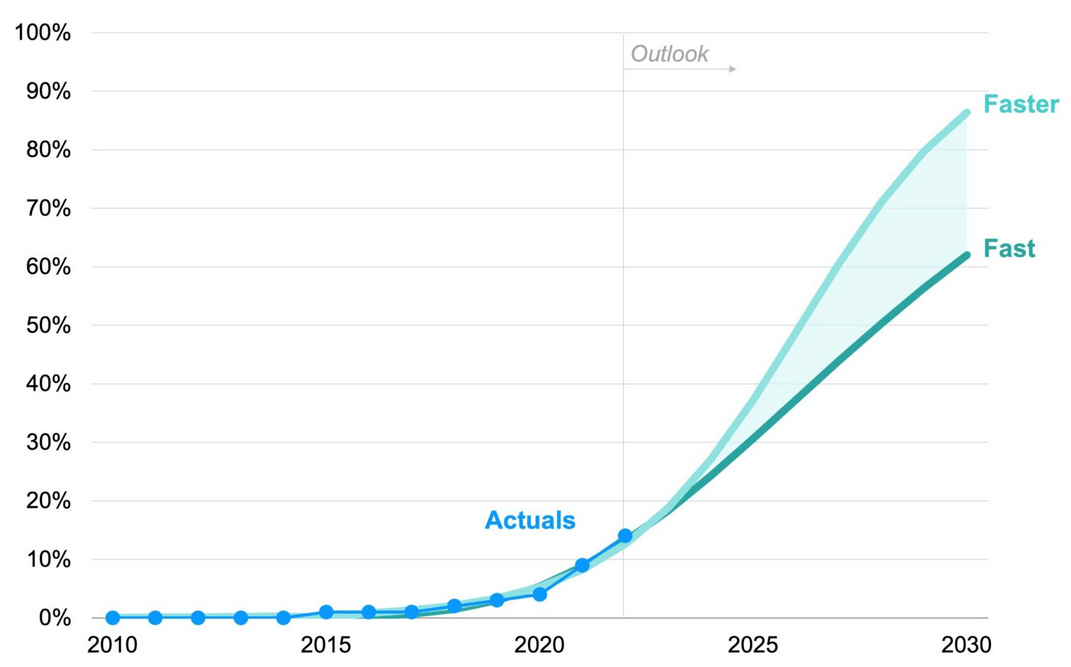

EV sales are forecast to increase to somewhere between62% and 86% market share of global car sales by 2030

Friday October 20, 2023 – CMI Masterclass: Critical Minerals in the Congo. Details and event tickets here.

Elcora order is just the beginning of its journey in the manganese market

written by InvestorNews | October 26, 2023

Manganese is becoming a key part of the lithium-ion battery market, traditionally used in nickel, manganese, cobalt (“NCM”) batteries; but now it is also used in lithium manganese iron phosphate (“LMFP”) batteries. This new battery type offers greater energy density (and hence EV range) than the standard LFP battery. Manganese is still largely used in steel, but the battery demand looks set to grow much faster. Overall the global manganese market is expected to grow at a CAGR of 5.5% from 2023 to 2027.

LMFP batteries containing manganese are the latest development to improve lithium-ion batteries

As announced last month Gotion High-tech Co Ltd. (SHE: 002074) has developed a breakthrough LMFP battery that offers a “range of up to 1,000kms for a single charge and could last two million kms”. Their new battery pack will go into mass production in 2024.

In 2022 it was reported that “CATL will soon mass produce LMFP batteries”. Contemporary Amperex Technology Co., Limited (SHE: 300750) (“CATL”) is the world’s largest lithium-ion battery manufacturer by far with 37% market share and is a leading supplier of Tesla Inc. (NASDAQ: TSLA). At Tesla Battery Day in 2020, Elon Musk pointed out that Tesla targets to use manganese in its batteries for long-range electric cars.

At Tesla Battery Day 2020, Tesla targets to use nickel and ‘manganese’ batteries for long range vehicles where vehiclemass is not too large

Note: Red oval done by the author to highlight manganese

Today’s company made a key announcement this week regarding commencement of manganese ore sales.

Elcora Advanced Materials Corp.

Elcora Advanced Materials Corp. (TSXV: ERA | OTCQB: ECORF) (“Elcora”) is working towards becoming a vertically integrated battery material company. Elcora has developed a cost-effective process to purify high-quality battery metals and minerals that are commercially scalable.

Elcora’s key projects have graphite, manganese, and vanadium. Elcora also has exposure to anode materials and graphene.

“has received its first monthly order for 1000 metric tons of 37% + manganese ore. The delivery of the first part of the order is scheduled before the end of June 2023. The order was placed by a leading European customer looking for a long-term supply relationship and marks a significant milestone for Elcora’s mining division.“

The order is not large but it marks the beginning of what can be a good business for Elcora if they can achieve large-scale production. Manganese ore (37% Mn grade) currently trades at about US$3.13/ dmtu (Dry Metric Tonne Unit) FOB Port Elizabeth.

“The recurrence of orders is expected to generate significant revenue for Elcora Advanced Materials Corp, further strengthening its position in the industry. With the increasing demand for manganese ore, the company is well-positioned to meet the needs of its customers...Elcora Advanced Materials Corp is well-positioned to benefit from this growing demand, and this order is just the beginning of its journey in the manganese market.”

Elcora’s Atlas Fox Project in Morocco – Beni Mellal Manganese Deposit/Mine and the Ouarzazate Project (including the Omar Mine)

Elcora’s Atlas Fox Project in Morocco is rich in manganese. It is comprised of the Beni Mellal Manganese Deposit/Mine and the Ouarzazate Project (including the Omar Mine).

At the Beni Mellal concessions, Elcora has a 10-year Exploitation License. This manganese concession contains a surface deposit mine that operated during French colonial times. Elcora plans to leverage on-site infrastructure with ore ready for processing. In Q4 2023 Elcora plan to build a gravimetric concentrator to upgrade raw ore content (30% Mn) to 50% Mn and increase mine production to 2,500 to 3,000 t/month of 50% Mn concentrate.

At the Ouarzazate Project Omar Mine, Elcora has acquired exclusive mining rights and an option to purchase the 16 km² manganese mining concession. The concession contains both a surface deposit and underground mine. Elcora is leveraging on-site infrastructure and has existing manganese ore piles of approximately 6,000 tonnes that are ready for processing. Elcora plans to ramp up mining production to 2,500 tons per month at the Omar Mine.

Elcora’s overall manganese ore production capacity is targeted to be more than 5,000 metric tonnes per month from the above concessions.

Atlas Lion Vanadium Project in Morocco

Elcora owns the Atlas Lion Vanadium Project (304 Km2) concessions in Morocco. Elcora plans to further explore and develop these concessions with the goal of producing vanadium.

Elcora’s next steps for mining manganese and vanadium in Morocco

In total, Elcora currently owns seventeen polymetallic (vanadium, lead, other), one manganese (and one option to purchase) and one copper licences/concessions in Morocco.

Elcora is making strong progress on its goal to become an integrated battery metals producer. The Company already has the technology and facilities to purify high-quality battery metals (notably spherical graphite, graphene, and anode powder) and is now working on the mining side with manganese and vanadium (noting they already have a graphite mine). The Atlas Fox Projectin Morocco has commenced stockpiled manganese ore sales and plans to ramp up manganese ore production from its concessions to 5,000/t per month. Following this will be development work and potentially production from the Atlas Lion Vanadium Project, also in Morocco.

Elcora Advanced Materials Corp. trades on a market cap of only C$18 million, suggesting this may potentially be just the beginning for Elcora.

Jamie Tuer of Fjordland Provides Updates on its South Voisey’s Bay Deal and Graphite Prospects

written by InvestorNews | October 26, 2023

In this InvestorIntel interview, Tracy Weslosky talks with Fjordland Exploration Inc.’s (TSXV: FEX) CEO, President, and Director Jamie Tuer about the opportunity for it to focus on its South Voisey’s Bay (SVB) nickel project in Labrador now that Ivanhoe Electric (TSX: IE | NYSE American: IE) has dropped its investment agreement.

The SVB project has had $30 to $40 million invested in it over the years and, with nickel in high demand for the batteries in electric vehicles (EVs), Jamie explains how this could be an opportunity for Fjordland to attract a partner that is interested in developing nickel, which he said is “hot right now.”

Jamie also discusses the potential for graphite at their Renzy Nickel Copper project in Quebec. Fjordland has sent some previous drill core sample to SGS Canada’s lab in Lakefield, Ontario for analysis. He mentions the high-quality nature of the graphite mineralization and that it could be suitable for use in lithium-ion batteries for EVs.

To access the full InvestorIntel interview, click here.

Subscribe to the InvestorIntel YouTube channel by clicking here.

About Fjordland Exploration Inc.

Fjordland Exploration Inc. is a mineral exploration company that is focused on the discovery of large-scale economic metal deposits in Canada.

In collaboration with Commander Resources Ltd., Fjordland is exploring the SVB “Pants Lake Intrusive” target which is in a geologic setting analogous to the nearby nickel-cobalt-copper Voisey’s Bay deposit. Fjordland has earned a 75% interest in the project.

Fjordland also owns a 100% interest in the Renzy nickel project located near Maniwaki, Quebec. The project encompasses the former Renzy Mine where, during the period from 1969 to 1972, 716,000 short tons were mined with average grades of 0.70% nickel and 0.72% copper. Fjordland has staked additional claims to increase the size of the project to 530 sq. km.

As well, Fjordland has two copper-gold properties in the Quesnel Trough of central British Columbia, The West Milligan copper-gold project is a joint venture with Northwest Copper Corp. located within 4 km of Centerra’s Mount Milligan copper-gold mine. The 103 sq. km. Witch copper-gold project is located another 35 km west of the Milligan mine.

To know more about Fjordland Exploration Inc., click here.

Disclaimer: Fjordland Exploration Inc. is an advertorial member of InvestorIntel Corp.

This interview, which was produced by InvestorIntel Corp., (IIC), does not contain, nor does it purport to contain, a summary of all the material information concerning the “Company” being interviewed. IIC offers no representations or warranties that any of the information contained in this interview is accurate or complete.

This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein.

Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Prospective investors are urged to review the Company’s profile on Sedar.com and to carry out independent investigations in order to determine their interest in investing in the Company.

If you have any questions surrounding the content of this interview, please contact us at +1 416 792 8228 and/or email us direct at [email protected].

With the graphite market currently being monopolized by China, Jack says that until battery-grade graphite, of a particular purity and shape, is mined and processed in North America, the market is going to be dependent on China. He adds, “…that’s an area [graphite] that North America can probably succeed in becoming self-sufficient.”

Jack goes on to discuss the recent popularity of Lutetium, the heaviest rare earth element, that can potentially be used in making a room-temperature superconductor. Speaking about the rarity and limited production of lutetium globally, Jack explains why mass production of room-temperature superconductors using lutetium is improbable.

Subscribe to the InvestorIntel YouTube channel by clicking here.

About The Critical Minerals Institute

The Critical Minerals Institute or CMI is an international organization for critical mineral companies and professionals focused on battery and technology materials, defense metals, and ESG technologies in the EV market. Offering a wide range of B2B service solutions, the Critical Minerals Institute hosts both online and in-person events designed for education, collaboration, and service solutions that address critical mineral challenges for a decarbonized economy.

To learn more about The Critical Minerals Institute, click here.

James Tuer of Fjordland Exploration Discusses Advancing Canadian Battery Metals Projects

written by InvestorNews | October 26, 2023

In this InvestorIntel interview during PDAC 2023, Chris Thompson talks with Fjordland Exploration Inc.’s (TSXV: FEX) CEO, President, and Director James Tuer about an update on Fjordland’s portfolio of battery metals projects in Canada. As a company focused on copper, nickel, cobalt, graphite, and lithium, James provides an update on their South Voisey’s Bay (“SVB”) Project in Labrador, Canada, on which, they have a partnership agreement with Robert Friedland’s Ivanhoe Electric (TSX: IE | NYSE American: IE).

With geologic settings similar to the nearby nickel-cobalt-copper Voisey’s Bay deposit operated by Vale S.A. (NYSE: VALE | BOVESPA: VALE3), James highlights the potential for finding high-grade nickel at their South Voisey’s Bay Project. James goes on to provide an update on their Renzy Nickel Copper Project in Quebec as it is exploring a past-producing mine, where the recent drill results showed a wide zone of graphite mineralization.

Finally, James mentions that the Company recently staked some ground in Quebec that was denoted on old maps as white pegmatite which is often composed of lithium-bearing spodumene.

To access the full InvestorIntel interview, click here.

Subscribe to the InvestorIntel YouTube channel by clicking here.

About Fjordland Exploration Inc.

Fjordland Exploration Inc. is a mineral exploration company that is focused on the discovery of large-scale economic metal deposits in Canada.

In collaboration with Ivanhoe Electric Inc. and Commander Resources Ltd., Fjordland is exploring the SVB “Pants Lake Intrusive” target which is in a geologic setting analogous to the nearby nickel-cobalt-copper Voisey’s Bay deposit. Fjordland has earned a 75% interest in the project.

Fjordland also owns a 100% interest in the Renzy nickel and copper project located near Maniwaki, Quebec. The project encompasses the former Renzy Mine where, during the period from 1969 to 1972, 716,000 short tons were mined with average grades of 0.70% nickel and 0.72% copper. Fjordland has staked additional claims to increase the size of the project to 530 square km.

In addition, Fjordland has 2 copper-gold properties in the Quesnel Trough of central British Columbia. The West Milligan copper-gold project is a joint venture with Northwest Copper Corp. (TSXV: NWST) located within 4 km of Centerra Gold’s (TSX: CG) Mount Milligan copper-gold mine. The Witch copper-gold project is 103 square km and located another 35 km west of the Milligan mine.

To know more about Fjordland Exploration Inc., click here.

Disclaimer: Fjordland Exploration Inc. is an advertorial member of InvestorIntel Corp.

This interview, which was produced by InvestorIntel Corp., (IIC), does not contain, nor does it purport to contain, a summary of all the material information concerning the “Company” being interviewed. IIC offers no representations or warranties that any of the information contained in this interview is accurate or complete.

This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein.

Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Prospective investors are urged to review the Company’s profile on Sedar.com and to carry out independent investigations in order to determine their interest in investing in the Company.

If you have any questions surrounding the content of this interview, please contact us at +1 416 792 8228 and/or email us direct at [email protected].

{kind=link}

{kind=link}