Westwater Resources Solidifies Position in the Graphite Anode Market

Westwater Resources, Inc. (NYSE American: WWR), an American graphite miner and manufacturer based in Colorado, recently made significant strides in solidifying its position in the graphite anode market. On February 5th, Westwater Resources inked a conditional offtake agreement with South Korean firm SK On Co., Ltd. securing a deal to supply up to 34,000 metric tons of natural graphite anode products to support SK On’s battery manufacturing operations across the United States.

SK On is a subsidiary of the SK Group, South Korea’s second-largest conglomerate which currently operates two electric vehicle (EV) battery plants located in Georgia and is working with both Ford Motor Co. and Hyundai Motor Group to construct two additional battery plants.

This move is part of Westwater’s strategic approach to vertically integrate the graphite anode supply chain, ensuring a steady and reliable source of graphite for key industries such as electric vehicles, military applications, and energy storage systems. Westwater Resources provides a compelling investment opportunity, as the company looks to capitalize on emerging geopolitical and macroeconomic factors contributing to increased graphite demand from domestic miners and producers.

About the Company

Founded in 1977 and headquartered in Colorado, Westwater Resources is a prospective graphite miner and producer with two graphite mining properties and a future anode production facility located in Alabama. The flagship Coosa Graphite Project is the largest graphite deposit in the lower United States and is located in the heart of the Alabama Graphite Belt, an area renowned for significant historic graphite production. The property covers 42,000 acres and contains 4.5 million metric tons of inferred and indicated graphite concentrate.

Alongside hosting graphite, the Coosa project hosts prospective vanadium mineralization, another critical mineral in the energy transition. Westwater is currently in the process of constructing one of the United States’ premier graphite processing facilities located in Kellyton, Alabama, which is planned to be online and producing 12,500 metric tons of graphite anode products by 2026 and will produce 50,000 metric tons of graphite anode products per year once operating at full capacity in 2028. The company’s vertical integration positions Westwater Resources as a key player in meeting industry needs while maintaining a balanced approach to growth and innovation.

Geopolitical and Macroeconomic Factors

Through strategic acquisitions and deal-making, Westwater now finds itself with a competitive advantage to become one of the United States’ premier graphite miners and producers by 2028. Geopolitical and macroeconomic developments have contributed to the urgency of the US government to take action in supporting the development of graphite mining and production infrastructure. Recent Chinese export controls on graphite underscore the national security concerns associated with a lack of graphite mining and processing within the United States. China – which already produces 70% and refines 90% of the world’s graphite supply – will now force exporters to seek permits for the shipment of two categories of materials, encompassing high-purity, high-hardness, and high-intensity synthetic graphite material, along with natural flake graphite and its associated products.

In the following months of the enactment of this policy, Chinese graphite exports slumped over 91% signaling tough times for foreign importers of the product. On the US side, graphite miners have recently lobbied the Office of the United States Trade Representative to include graphite on the list of Section 301 tariffs originally imposed by the Trump administration and further expanded by the Biden administration. This would see a 25% tariff added onto Chinese graphite. These policies leave Westwater Resources with the strategic advantage to capitalize on the US “friendshoring” initiatives which aim to produce and obtain raw materials either domestically or from a coalition of nations that uphold common principles and beliefs.

Management’s ability to develop a vertically integrated supply chain, will result in synergies which sees the graphite go from the ground to the manufacturer, affording the company the opportunity to fully capitalize on each stage of the production process without having to turn to third party miners or processors. The recent deal signed with SK On is the first step in ensuring Westwater will take advantage of this shift to domestic production and processing. As the company continues to penetrate the domestic graphite supply market, Westwater can ensure a consistent and stable access to essential graphite resources, reducing dependency on foreign sources and mitigating risks associated with geopolitical uncertainties.

Graphite Supply Deficits

Graphite demand is steadily increasing, and is estimated to grow by 70% over the next five years. It is assumed that by 2025 graphite demand will overtake supply and supply deficits will begin to take hold of the market. While previously mentioned geopolitical ramifications will only contribute to supply constraints. These price dynamics will inevitably result in a supply deficit as demand continues to outpace supply. The United States has already enacted import controls on other key battery materials, and any further escalations in US-Sino trade disputes would potentially see an even tighter squeeze on the graphite market, from both the Chinese and American side.

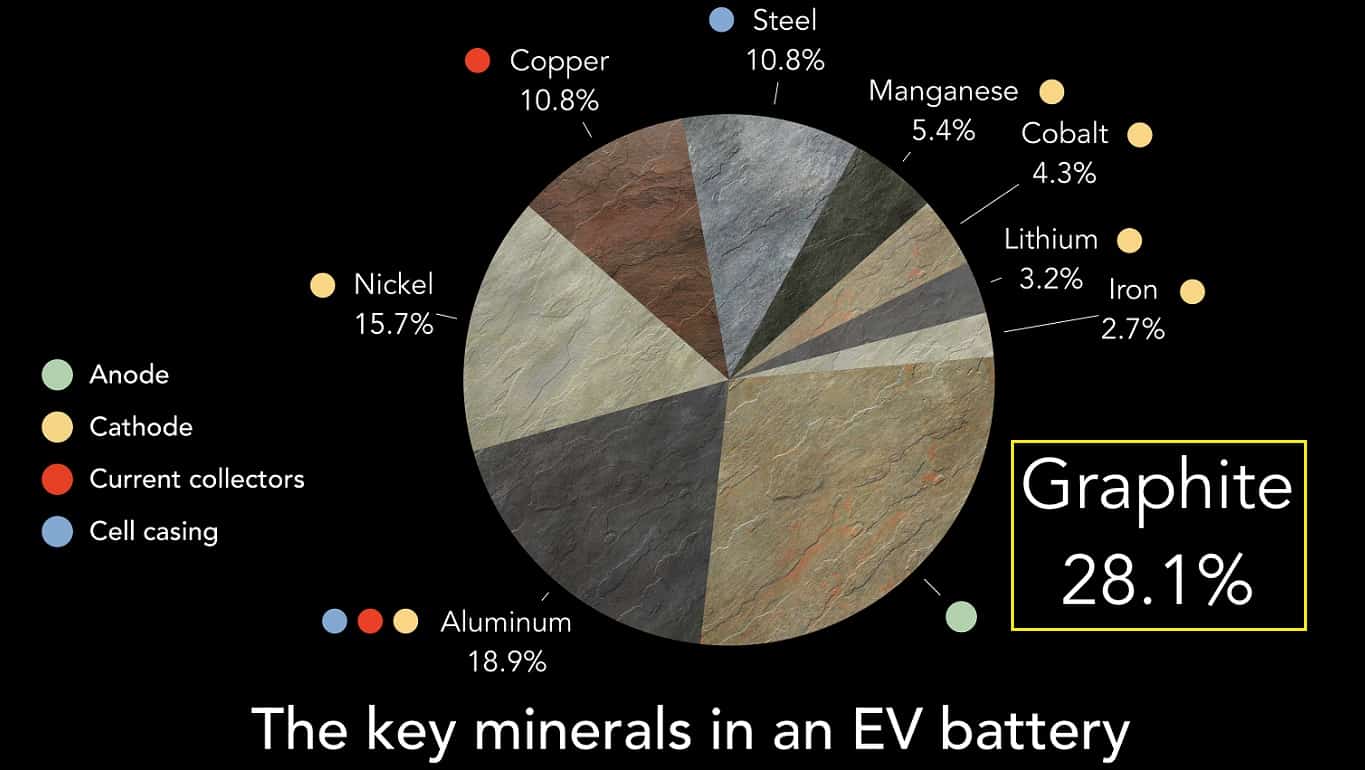

It is estimated that by 2030 the graphite supply of stable democracies – the key beneficiaries of ‘friendshoring’ policies – will face a 29,581 thousand metric ton shortfall, a cause for concern considering graphite currently composes approximately 30% of lithium-ion batteries and is the largest component by weight within the battery. Furthermore, graphite composes 95% of anode material used in lithium-ion batteries, making it a necessary anode component in any EV battery as currently there are no replacements. The necessity of graphite as an anode material in EV batteries ensures that Westwater’s graphite anode products will remain in high demand. Since Westwater plans to have both the Coosa Mine fully operational and their Kellyton Anode Plant operating at full capacity by 2028, the company will be able to benefit from the market shortfalls in an environment of increased demand and waning supply by being able to provide up to 50,000 metric tons per year of graphite anode to manufacturers.

Proprietary Production Process and Ultra High-Purity Graphite

Another strategic advantage that Westwater has is in its proprietary production process. The tailormade production process – which is currently patent pending – has resulted in lower production costs, decreased CO2 emissions, and increased product purity. Moreover, the process is significantly more environmentally friendly than traditional processing techniques which use toxic chemicals such as hydrofluoric and hydrochloric acid, neither of which are used in Westwater’s proprietary process.

The exclusion of these chemicals from the production process improves the overall footprint of the company while also decreasing the liability of dealing with these toxic chemicals. This production process results in an ultra high-purity product. Whereas battery manufacturers require 99.9% graphite purity for their batteries, Westwater will be able to produce anode products with 99.95% purity, putting it above the required purity for battery applications. Westwater will also be able to tap into expanding graphite markets such as military applications, and grid batteries which require ultra high-purity graphite. The ability to produce ultra high-purity graphite anode products coupled with the decreased environmental footprint ensures that Westwater upholds key Environmental, Social, and Governance (ESG) principles in line with industry standards without sacrificing product quality.

Ultimately, Westwater Resources’ ability to position itself as a vertically integrated graphite miner and producer has placed it in a prime position to take full advantage of emerging geopolitical and macroeconomic factors in the graphite market. Future graphite supply deficits ensure that demand for Westwater Resources’ graphite will remain elevated. Their proprietary production process enables the company to produce an ultra high-purity graphite anode product while maintaining environmental consciousness. Westwater’s market cap is approximately USD$28.78M and the WWR stock is trading at approximately $0.50 per share (recorded at 2:45 PM EST, May 7, 2024).