The Critical Minerals Institute Report (01.25.2024): U.S. government bans Pentagon battery purchases from major Chinese companies starting October 2027

Welcome to the January 2024 Critical Minerals Institute (CMI) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the CMI List of Critical Minerals or visit the CMI Library.

Global macro view

January 2024 saw a slight rise in U.S. inflation reported from 3.1%pa in November to 3.4%pa in December 2023. This has led market commentators to suggest the proposed 2024 interest rate reductions may be pushed out to H2, 2024, or be smaller in nature.

The next U.S. Fed rates announcement is due on January 31, 2024, and no changes in rates are expected. Year to date, as of January 21, 2024, the S&P 500 is up 2.04%. U.S. GDP looks set to slow in Q4, 2023 (announcement due 25 January 2024) with forecasts for 2% annualized growth, which would result in a 2023 GDP of ~2.7%. 2024 U.S. GDP is forecast to be ~2.2%. The U.S. consumer remains resilient with U.S. employment very strong.

China continues its property led slowdown with 2023 GDP recently reported at 5.2% annualized. China’s December new home prices fell at the fastest pace in almost 9 years. Despite this the Chinese Central Bank left rates unchanged, defying expectations for a 0.1% cut.

The Russia-Ukraine war continues as does the Hamas-Israel war which last month spread to include the U.S. and UK forces bombing Iran-backed Houthis over their attacks in the Red Sea. The Middle East is a hotbed ready to explode.

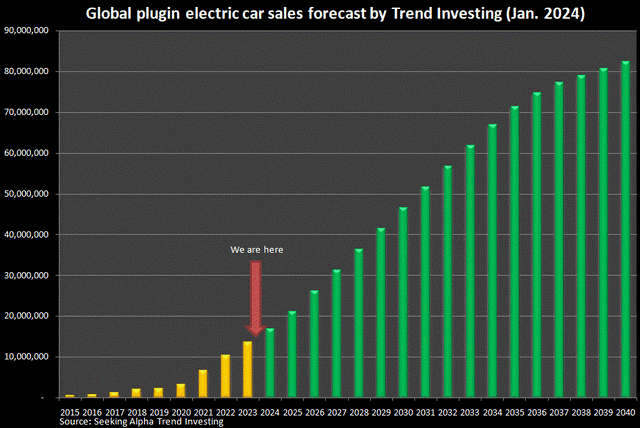

Global plugin electric vehicle (“EV”) update

December 2023 saw the usual seasonal upswing in global plugin electric car sales reaching a record ~1.5 million. China led the way with a stellar result of 1.191 million units, up 46% YoY.

Global plugin electric car sales ended 2023 at 13.6 million units (~16% market share), for a growth rate of 31% YoY (a significant slowdown from the ~60% growth rate in 2022).

- Trend Investing forecast for 2024 is 17 million units (20% market share), for a growth rate of 25% YoY.

- BloombergNEF forecast for 2024 is 16.7 million units (~20% market share), for a growth rate of 21% YoY.

We are still at the very early stage of the EV boom.

In early January, news was released that a record 1.2 million EVs were sold in the U.S. in 2023, according to estimates from Kelley Blue Book. The report noted that U.S. market share reached 7.6% in 2023 and that 55% of EV sales were attributable to Tesla (NASDAQ: TSLA).

The UK announced that their Zero Emission Vehicle (ZEV) mandate to increase electric car sales has become law. Key rules include:

- “ZEV Mandate demands makers up share of electric car sales to 22% in 2024.

- Electric vehicles currently make up around just 18% of all registrations in the UK.

- Mandate thresholds rise annually to an 80% share in 2030 – and 100% by 2035.

- Failure to meet the ZEV mandate sales targets can result in huge fines for auto makers of £15,000 per model below the required threshold.”

EV battery news

The U.S. government continues to tighten the screws towards developing their own EV supply chain independent of Foreign Entities Of Concern (“FEOC”). On January 20 Bloomberg reported: “US to ban Pentagon battery purchases from China’s CATL, BYD”. The ban will commence from October 2027 and include 4 other Chinese battery makers (Envision Energy Ltd., EVE Energy Co., Gotion High Tech Co., and Hithium Energy Storage Technology Co).

Global critical minerals update

There is an enormous amount of doom and gloom surrounding the EV and battery metals sector as we commence 2024. A key theme in recent months has been very depressed prices for many of the critical minerals, especially those related to the EV segment. A combination of the slowing EV growth rate in 2023 from ~60% in 2022 to ~31% in 2023, combined with an excess of battery inventory from 2022 and new EV metals supply has left most EV metal markets in surplus with prices collapsing.

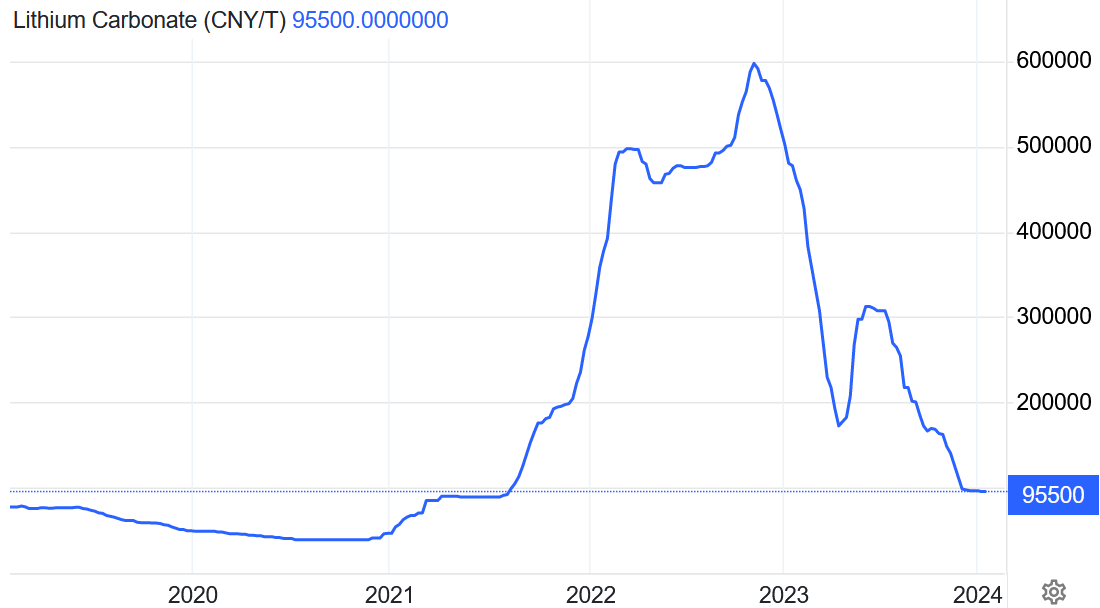

Lithium

China lithium carbonate spot prices were flat the past month, with the price now at CNY 95,500/t (USD 13,275/t). After an ~80% fall from the high, lithium prices appear to have finally stabilized. This is logical given that prices are now at or below the marginal cost of production, especially for the higher cost China lepidolite producers.

Industry participants have been calling for a price bottom in recent months, with China Futures Co. analyst, Zhang Weixin, forecasting lithium prices to bottom out between CNY 80- 90,000/t and average CNY 100,000/t in 2024.

The other key recent trend in the lithium sector has been several announcements from lithium producers either stopping production or reducing their expansion plans. Core Lithium (ASX: CXO) announced on January 5, 2024 it will temporarily suspend mining operations. Then on January 17, 2024, Albemarle Corporation (NYSE: ALB) announced “actions to preserve growth, reduce costs, and optimize cash flow”. This includes deferring plans to build a fourth lithium hydroxide processing train at their Kemerton LiOH facility.

The China lithium carbonate spot price has stabilized near the marginal cost of production

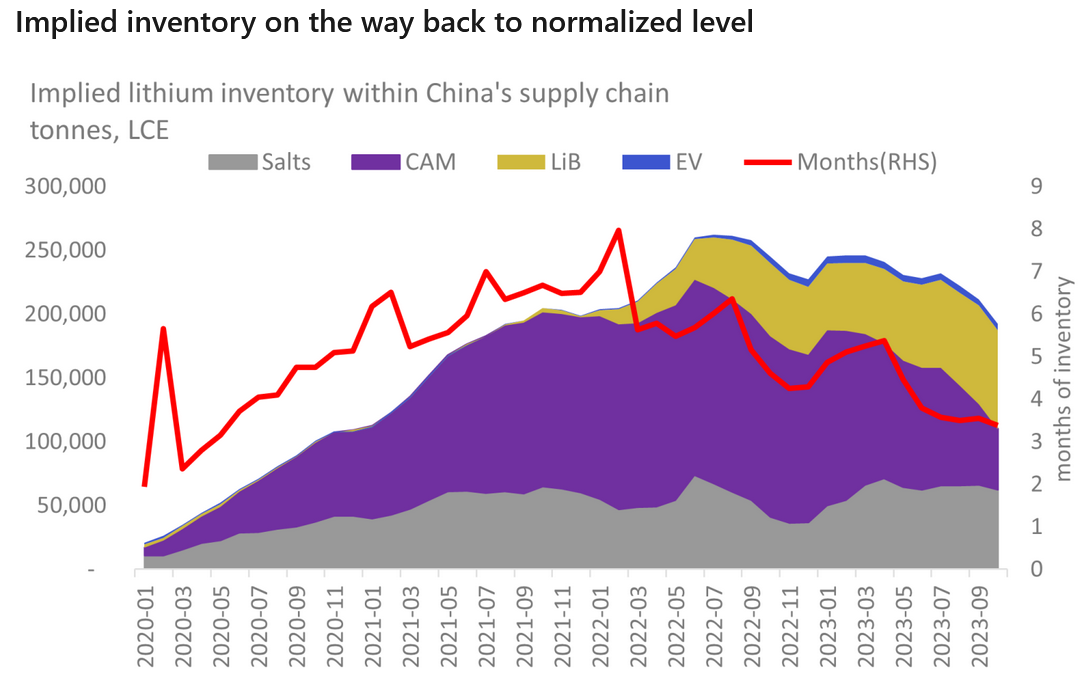

On the topic of when we might see some recovery in lithium prices. On January 19 Fastmarkets put out a report stating: “…We expect orders to start flowing upstream again either towards the end of the first quarter or early in the second quarter.” If this proves correct and EV demand remains solid, then we could expect some lithium price recovery late Q1, early Q2, 2024.

Fastmarkets reports China lithium inventory levels are now back to the pre-boom levels with ~3 months of supply (red line)

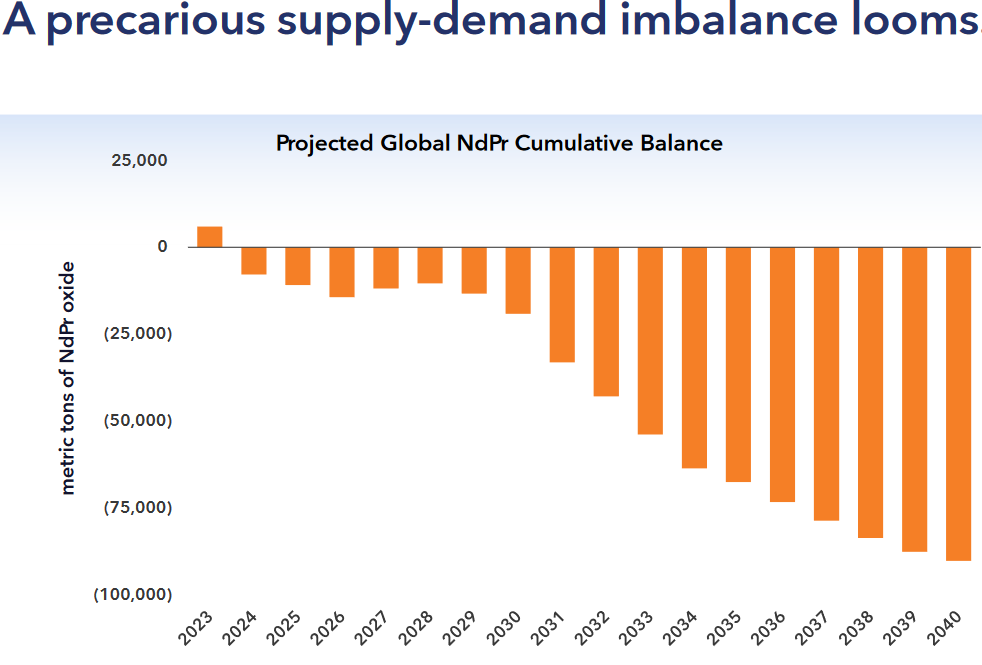

Magnet Rare Earths

Neodymium spot prices fell again the past month to CNY 505,500/t. Prices peaked in February 2022 at CNY 1,506,530 and have been trending lower ever since then.

As discussed in a recent InvestorNews article, the consensus of industry experts is for 2024 to be a consolidation year. The article states: “2024 should see a year of consolidation for the rare earths sector as some experts are telling me. Some forecasts are for NdPr supply deficit to begin as early as 2024; however, this will largely depend on China demand, the global economy, EV sales, and new NdPr supply hitting the market.”

One interesting news item that emerged in January was of Rainbow Rare Earths Limited (LSE: RBW) (“Rainbow”) and their Phalaborwa Project in South Africa. The key aspect being that the Project consists of gypsum waste piles that contain large quantities of the magnet rare earths. Rainbow CEO Bennett stated: “We’ve got no mining cost, no crushing, no milling, no flotation. I saw the advantages to lead to a low capital intensity and low operating cost environment project.” Rainbow targets first production for 2026.

Some analysts are forecasting deficits ahead for NdPr rare earths driven by strong EV and wind energy demand

Cobalt, Graphite, Nickel, Manganese and other critical minerals

Cobalt prices (currently at US$12.90/lb) were flat the past month and remain at very depressed levels. The cobalt market is suffering from excess cobalt supply from the DRC which combined with a global slowdown in demand has led to cobalt prices dropping by almost 2/3 since their April 2022 peak. With LFP batteries gaining in popularity (no cobalt required) and a weak global consumer electronics market, there appears to be no short term turnaround for cobalt. Leading cobalt producer Glencore PLC (LSE: GLEN | OTC: GLCNF) has been stockpiling their excess material. At current prices, there is limited incentive for western producers to expand or enter the market.

Cobalt has lost two-thirds of its value since a recent peak in 2022

Flake graphite prices remain very weak with prices near the marginal cost of production and down ~2% over the past month.

A January 2024 Bloomberg report noted that natural flake graphite shipments slumped 91% in December from November 2023. Of course, sales surged prior to the Chinese export license permits being implemented in December 2023. December exports were 3,973 tons compared to the past monthly average of ~17,000t, so still a very significant fall.

Despite the spate of recent bad news, graphite is one of the EV metals with the largest demand profiles ahead this decade. Several groups are forecasting deficits ahead this decade starting from 2024/25 for the various types of graphite including flake, spherical, and synthetic. You can read more on the graphite outlook here.

Nickel prices fell again last month to USD 15,799/t. The 1 year outlook for nickel remains poor due to oversupply concerns from Indonesia. As a result of low nickel prices we saw the collapse of Panoramic Resources (ASX: PAN) in December and then on January 22, 2024, it was reported that BHP Group (ASX: BHP | NYSE: BHP) plans “to put parts of Kambalda nickel concentrator in Australia on care and maintenance” from mid-2024. This was caused by Wyloo Metals, which supplies ore to the plant, announcing a pause in mining operations due to low nickel prices.

Manganese prices were flat the past month and are now at CNY 29.25/MTU.

Uranium prices have been the exception to the rule the past year as they continue to rise, now at US$106/lb.

Uranium 5 year price chart

Conclusion

The biggest trend that looks to be emerging in Q1, 2024 for the EV metals sector is a negative supply response from producers. Producers are cutting CapEx, scaling back expansion, and in some cases reducing or stopping production. Expect to see a lot more of this in H1, 2024.

They say “the cure for low prices is low prices”. Well that’s exactly where we are now in the cycle. The next 3-6 months is likely to see the washout phase, where many miners collapse, reduce production or put their mine into care and maintenance. There is no point running a mine and selling a limited resource and making no profit. I will end with three well known sayings:

- “Bear markets are the author of bull markets”

- “Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.”

- “You have suffered through the pain, now hang around for the gain.”

Given the EV metals markets have been in a bear market for the past 15-18 months the end is near, and we should expect some recovery during H2, 2024, assuming EV sales can grow at a reasonable rate.