Energy Fuels’ Strategic MOU with Astron: Shaping the Future of the U.S. Rare Earths Supply Chain

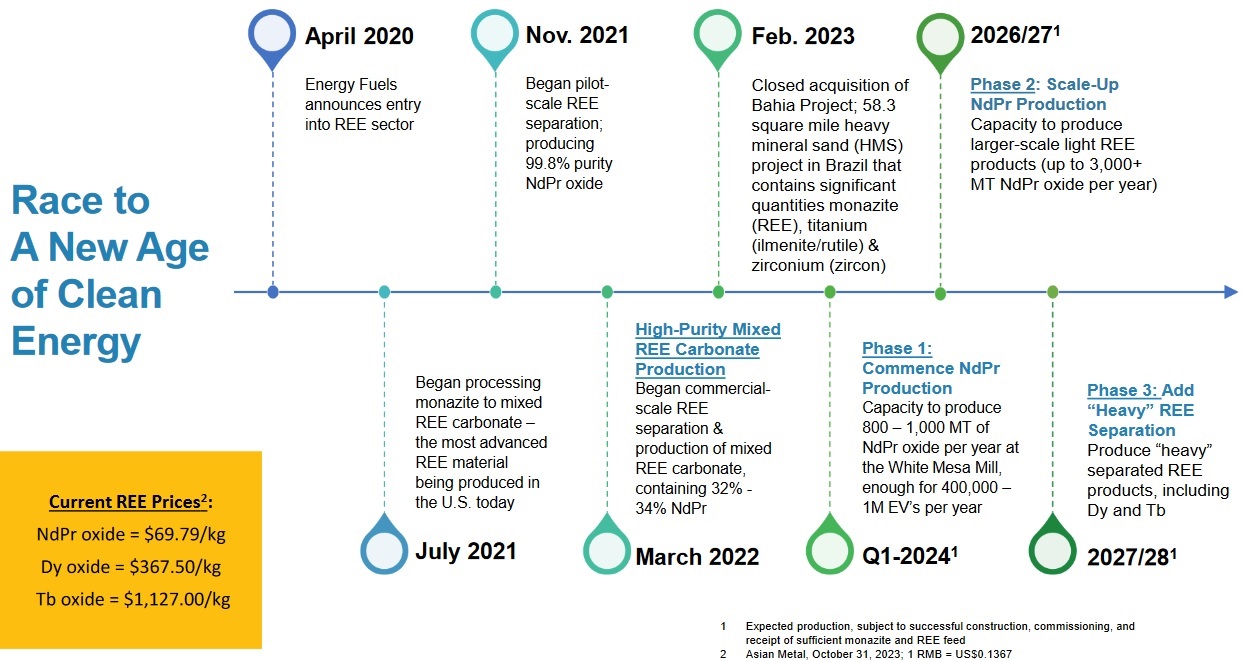

In a recent interview with Tracy Weslosky of Investor.News, Mark Chalmers, President, CEO, and Director of Energy Fuels Inc. (NYSE American: UUUU | TSX: EFR), discusses their recently announced Memorandum of Understanding (MOU) with Astron Corporation Ltd. (ASX: ATR) for the joint venture development of the Donald Rare Earth and Mineral Sands Project in Victoria, Australia. This MOU, announced on December 27, 2023, is a key milestone in establishing a U.S.-centric rare earths supply chain, which is crucial for the country’s future needs.

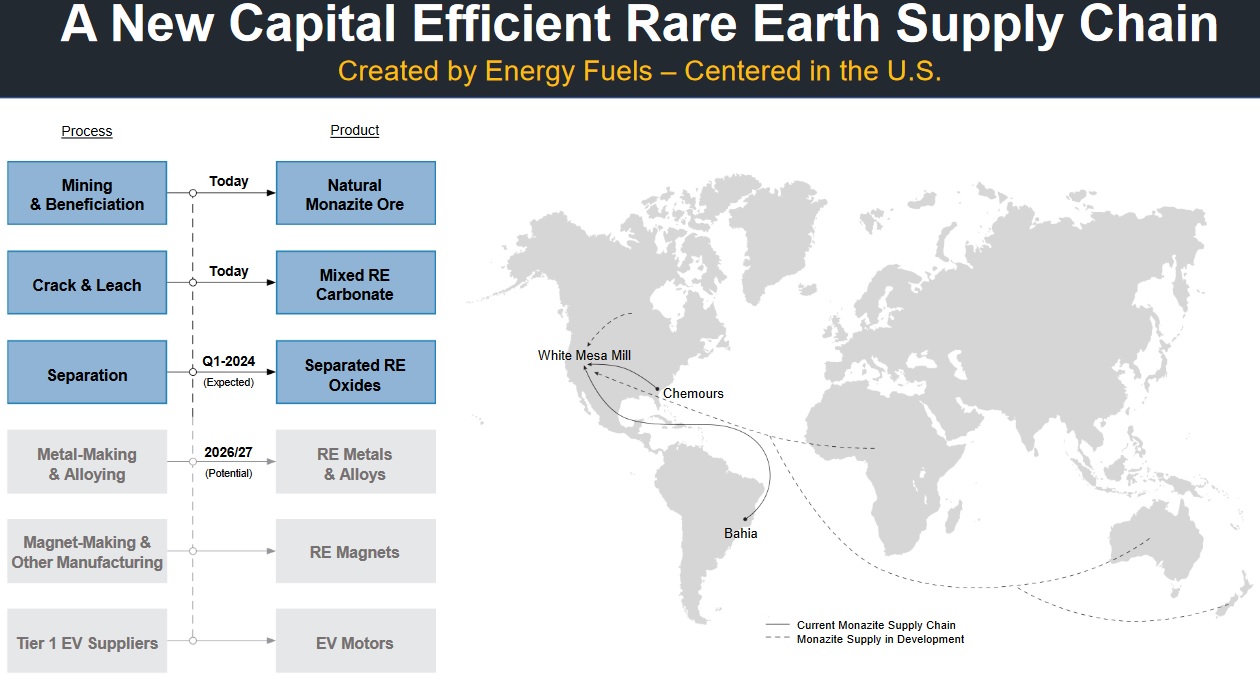

The Donald Project promises to supply Energy Fuels with 7,000 to 14,000 metric tons of rare earth concentrate, using monazite sand from the deposit. Energy Fuels plans to process this at their White Mesa Mill in Utah, where they can handle the radioactive elements in monazite and extract valuable components like uranium. This positions them as a leader in the critical minerals.

Energy Fuels’ approach is cost-effective, leveraging existing infrastructure and skilled workforce in Utah. The initial phase of the project aims to produce 800 – 1,000 metric tons of the magnetic materials, Neodymium-Praseodymium (NdPr) oxide by Q1 2024, with plans for future expansion.

The U.S. government’s policy, set to restrict critical minerals sourced from Foreign Entities of Concern from 2025, highlights the significance of Energy Fuels’ project. As a leading U.S. producer of uranium, vanadium, and rare earth elements, the company plays a vital role in reducing U.S. dependence on foreign sources, particularly China.

This venture is expected to have a major impact on the electric vehicle and clean energy sectors in the U.S., offering a sustainable, competitive, and independent supply chain for critical minerals, essential for national security and technological progress. To access the complete interview, click here

Don’t miss other InvestorNews interviews. Subscribe to the InvestorNews YouTube channel by clicking here

About Energy Fuels Inc.

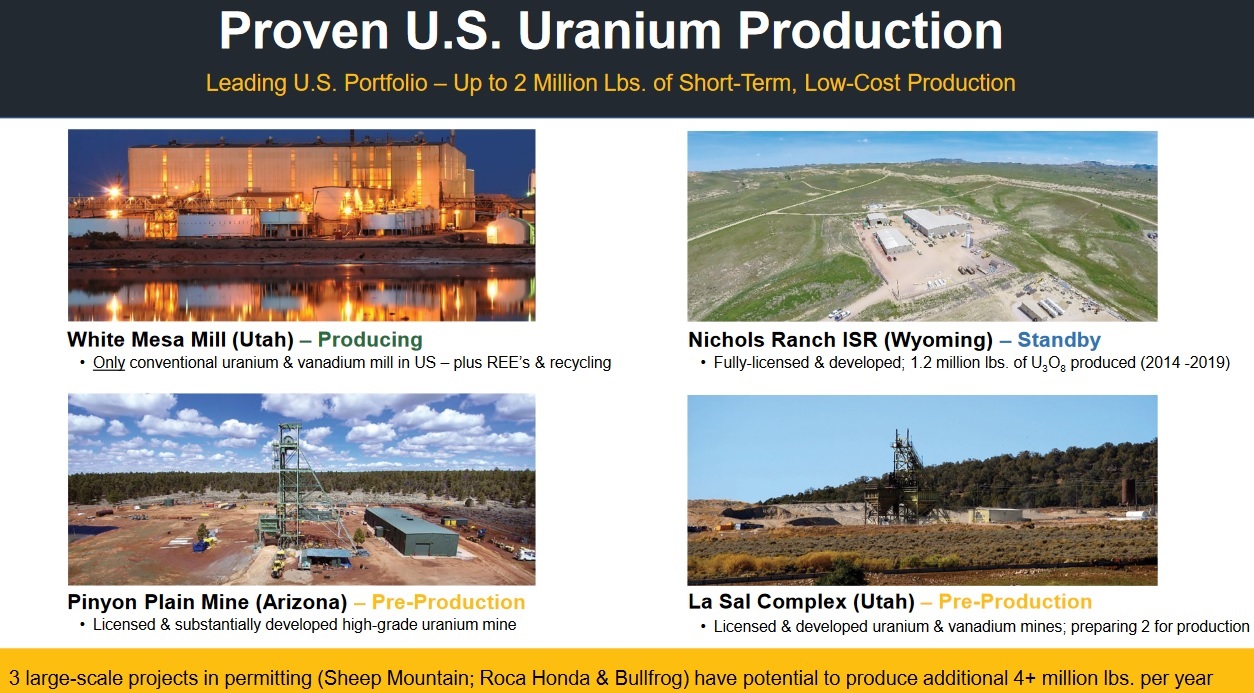

Energy Fuels is a leading US-based critical minerals company. The Company, as the leading producer of uranium in the United States, mines uranium and produces natural uranium concentrates that are sold to major nuclear utilities for the production of carbon-free nuclear energy. Energy Fuels recently began production of advanced rare earth element (“REE“) materials, including mixed REE carbonate, and plans to produce commercial quantities of separated REE oxides in the future. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is evaluating the recovery of radionuclides needed for emerging cancer treatments. Its corporate offices are in Lakewood, Colorado, near Denver, and substantially all its assets and employees are in the United States. Energy Fuels holds two of America’s key uranium production centers: the White Mesa Mill in Utah and the Nichols Ranch in-situ recovery (“ISR“) Project in Wyoming. The White Mesa Mill is the only conventional uranium mill operating in the US today, has a licensed capacity of over 8 million pounds of U3O8 per year, and has the ability to produce vanadium when market conditions warrant, as well as REE products, from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Company recently acquired the Bahia Project in Brazil, which is believed to have significant quantities of titanium (ilmenite and rutile), zirconium (zircon) and REE (monazite) minerals. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the US and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development.

To learn more about Energy Fuels Inc., click here

Disclaimer: Energy Fuels Inc. is an advertorial member of InvestorNews Inc.

This interview, which was produced by InvestorNews Inc. (“InvestorNews”), does not contain, nor does it purport to contain, a summary of all material information concerning the Company, including important disclosure and risk factors associated with the Company, its business and an investment in its securities. InvestorNews offers no representations or warranties that any of the information contained in this interview is accurate or complete.

This interview and any transcriptions or reproductions thereof (collectively, this “presentation”) does not constitute, or form part of, any offer or invitation to sell or issue, or any solicitation of any offer to subscribe for or purchase any securities in the Company. The information in this presentation is provided for informational purposes only and may be subject to updating, completion or revision, and except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any information herein. This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein.

Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. This presentation should not be considered as the giving of investment advice by the Company or any of its directors, officers, agents, employees or advisors. Each person to whom this presentation is made available must make its own independent assessment of the Company after making such investigations and taking such advice as may be deemed necessary. Prospective investors are urged to review the Company’s profile on SedarPlus.ca and to carry out independent investigations in order to determine their interest in investing in the Company.