Albemarle Lithium Auction offers a bold move forward in pricing transparency in the critical minerals market

written by InvestorNews | March 20, 2024

In a notable development within the lithium industry, Albemarle Corporation (NYSE: ALB), the world’s largest producer of lithium, has announced its plan to host an auction for a significant quantity of lithium on March 26. This move marks a strategic attempt to address the persistent issue of price discovery in a market characterized by its lack of transparency and high volatility. Jack Lifton, Co-founder of the Critical Minerals Institute (CMI), offers insightful commentary on the implications of this event, tying it to the broader challenges facing the lithium market today.

The auction by Albemarle, according to a news story published on Reuters yesterday is a response to the dramatic shifts witnessed in the lithium sector, propelled by the electric vehicle (EV) revolution. Since 2007, lithium production has surged from less than 4,000 tons to 186,000 tons, underscoring the metal’s critical role in the transition towards electrification. Despite this growth, the industry has struggled with establishing a clear and stable pricing mechanism, a challenge that Lifton identifies as a major impediment to investment and development within the sector.

Historically, the pricing of lithium has been opaque, often negotiated privately between producers and buyers. This lack of clarity has been further complicated by the introduction of lithium contracts on Chinese exchanges, which, despite their potential, have failed to provide a global benchmark due to issues of transparency and accessibility for international market participants. Western attempts to establish futures trading for lithium, such as those by the London Metal Exchange (LME) and the Chicago Mercantile Exchange (CME), have also seen limited success, highlighting the disconnect between traditional commodity trading mechanisms and the unique dynamics of the lithium market.

Albemarle’s upcoming auction represents an innovative approach to tackling these pricing challenges. By opening up the sale of a substantial quantity of lithium to competitive bidding, the company aims to foster greater transparency and provide a more accurate reflection of current market valuations. This initiative not only seeks to bridge the gap in price discovery but also serves as a potential model for future transactions in the industry.

Lifton emphasizes the importance of this auction in the context of the lithium market’s evolution. The shift towards digital auctions and the potential for establishing more transparent pricing indices reflect the industry’s adaptability and its search for solutions that align with the realities of global lithium supply and demand. However, he also cautions that while this auction may offer valuable insights, it is not a definitive solution to the market’s overarching issues of volatility and unpredictability.

In conclusion, Albemarle’s decision to host an auction for its lithium products is a significant step towards addressing the critical challenge of price discovery in the lithium market. As Lifton notes, this approach represents a move away from traditional pricing mechanisms and towards a more transparent and dynamic model. While the long-term impact of this and similar initiatives remains to be seen, they underscore the lithium industry’s ongoing efforts to adapt to the complexities of a rapidly evolving global market.

World Renowned Critical Minerals Expert Constantine Karayannopoulos is Bullish on Lithium

written by InvestorNews | March 20, 2024

In an insightful interview with Tracy Weslosky of InvestorNews, Constantine Karayannopoulos, a renowned expert in the field of critical minerals, shared his perspectives on the current state and future prospects of the critical minerals market. Karayannopoulos highlighted the pivotal role of critical minerals such as rare earths, lithium, and nickel in the burgeoning sectors of battery technology and electric vehicles (EVs), underscoring the global buzz around these resources. He noted the current challenges faced by small companies in raising funds and the general market sentiment. Despite these hurdles, he expressed optimism, suggesting that the downturn in valuations and financing is temporary. “We’re at close to or at the bottom of the cycle with a lot of these commodities,” he stated, advising resilience for these firms in anticipation of a market rebound fueled by sustained demand for technologies reliant on critical minerals.

Karayannopoulos offered insightful commentary on the critical minerals market, particularly focusing on lithium and rare earths. With a bullish stance on lithium, he reminisced about the industry’s past pricing projections and observed the current market’s resilience despite recent price drops. “Lithium still is the workhorse in the battery space… for the next decade, lithium will be the workhorse of the EV battery,” he affirmed, advocating for strategic investments in this area during market lows. His observations extended to the rare earths market, noting its sensitivity to Chinese economic dynamics and the potential for price stabilization in the near term. Highlighting Brazil’s emerging role in diversifying the global supply of heavy rare earths, he emphasized the importance of exploring favorable mineralogy and environmental practices in new geographies. This strategic diversification, he argued, is crucial for addressing the geopolitical and social concerns associated with current heavy rare earths sourcing, primarily from Myanmar.

Don’t miss other InvestorNews interviews. Subscribe to the InvestorNews YouTube channel by clicking here

Revolutionizing Energy Storage with NEO Battery Materials’ Strategic Advances in Silicon Anode Technology

written by InvestorNews | March 20, 2024

NEO Battery Materials Ltd. (TSXV: NBM | OTCQB: NBMFF), a leader in the development of low-cost silicon anode materials, is at the forefront of a technological revolution that promises to redefine the lithium-ion battery landscape. As the demand for electric vehicles (EVs) and renewable energy storage solutions grows, the quest for more efficient and cost-effective batteries has become more critical than ever. NEO’s strategic initiatives and recent achievements reflect its commitment to driving innovation in this space, amidst a broader industry shift towards silicon anodes over traditional graphite.

Since the commercial debut of lithium-ion batteries three decades ago, the technology has seen vast advancements, including a significant drop in price and improvements mostly on the cathode side. However, the graphite anodes used in these batteries have seen little innovation, until now. Silicon, capable of holding up to 10 times as many lithium ions by weight as graphite, has emerged as a promising alternative, despite its initial challenges, including volume expansion and material fracture.

NEO’s recent strategic moves, including increasing its ownership in its South Korean subsidiary, NBM Korea, and filing its 9th patent for a major silicon anode manufacturing innovation, underscore its role in this evolving market. The company’s efforts to overcome silicon’s historical challenges signify a major leap towards the commercialization of silicon anodes, which are essential for the next generation of lithium-ion batteries. These batteries promise longer ranges, faster charging times, and reduced costs for EVs, positioning silicon as a critical material in the global push towards electrification.

The significance of NEO’s advancements cannot be overstated in the context of the broader industry’s pivot towards silicon anodes. Companies like General Motors are already integrating silicon anodes into their products, signaling a market ready for change. Furthermore, the recent influx of nearly half a billion dollars in investments towards commercializing silicon anode materials, including significant contributions from the U.S. Department of Energy, highlights the strategic importance of this technology.

Silicon anodes not only offer the potential for longer-range and faster-charging EVs but also promise to alleviate supply chain constraints associated with graphite anodes, nearly all of which are processed in China. By reducing reliance on overseas graphite and leveraging silicon, the most abundant metal in Earth’s crust, companies like NEO are paving the way for a more sustainable and efficient future for batteries.

In its comprehensive strategy for 2024, NEO Battery Materials outlines a multi-faceted approach to commercialization, emphasizing operational execution, capital efficiency, and risk mitigation. The company’s vision extends beyond mere technological innovation; it aims to optimize the electrochemical performance and cost competitiveness of its silicon anode material, NBMSiDE®, to establish advanced commercial agreements and expand its global supply chain network.

As NEO and other industry players continue to advance silicon anode technology, the promise of more affordable, efficient, and sustainable lithium-ion batteries becomes increasingly tangible. This shift not only supports the growing demand for EVs but also contributes to the global effort to transition to renewable energy sources, marking a significant milestone in the quest for greener and more sustainable energy solutions.

The NEO Battery Materials Ltd. (TSXV: NBM | OTCQB: NBMFF) market cap for Thursday, February 22, 2024 is CAD$28.70M.

The Critical Minerals Institute Report (12.27.2023): Politics Driving Marketable Commodities into 2024

written by Matt Bohlsen | March 20, 2024

Welcome to the December 2023 Critical Minerals Institute (“CMI”) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the CMI List of Critical Minerals or click here to visit the CMI Library.

Global macro view

December 2023 saw a further fall in U.S. inflation from 3.2%pa in October to 3.1%pa in November. As expected the U.S. Fed left interest rates unchanged at their December meeting. Even more significant was the Fed indicated that there are potentially ‘3 interest rate cuts coming’ in 2024. This was an early Christmas present for U.S. equity markets which continued their recent rally. Year to date, as of December 26, 2023, the S&P 500 is up 25.75% and the NASDAQ is up an amazing 43.25%. Of course, this follows heavy falls in 2022.

In late December China signaled a possible early 2024 interest rate cut when they reduced bank deposit rates. As a result China 30 year government bond yields hit their lowest level since 2005. All of this recent support for China’s economy and property market looks likely to set up a potential China recovery story in 2024. If China starts to recover in 2024 it would be a positive for commodity markets including the critical minerals.

The Russia-Ukraine war drags on through the European winter. There are some very early signs that both sides may be willing to end the war in 2024. We will see. Meanwhile, the Hamas-Israel war has been contained for now. We can only hope for peace in 2024.

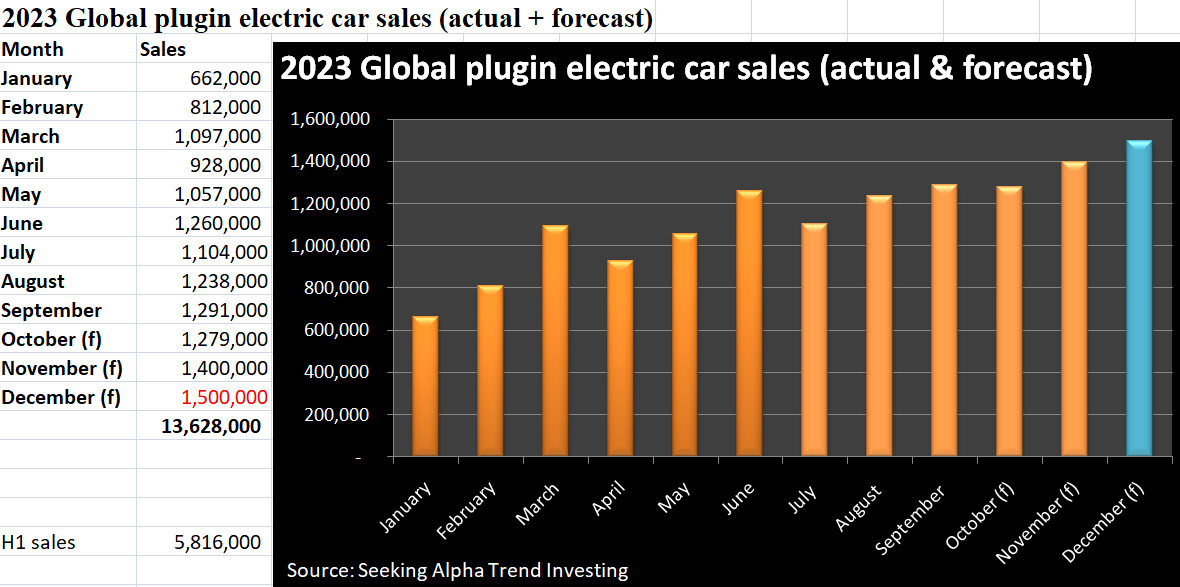

Global plugin electric vehicle (“EV”) update

Global plugin electric car sales were 1,279,000 in October 2023 (the second-best month ever), up 37% YoY. November global sales reached 1.4 million. December should be even better. CPCA expects China’s NEV (New Energy Vehicle) retail sales in December 2023 to reach a record 940,000 units (41.4% market share), up 46.6% YoY. That should mean December global EV sales will be around 1.5 million.

This means that 2023 global plugin electric car sales should end up close to 13.6 million (~17% market share), for a growth rate of ~29% YoY (a significant slowdown from the 56% growth rate in 2022).

In other EV related news, in December Germany announced an abrupt ending to their EV subsidy. The subsidy was originally intended to apply until the end of 2024.

We also heard news that the U.S. is considering raising tariffs on Chinese EVs and Chinese solar products. The White House plans to complete a tariff review in early 2024. Chinese EVs entering the USA already have a 25% tariff. This follows the EU’s probe into China subsidies for EVs. All of this has come about due to the fact that about 60% of all global plugin EV sales are in China and the fact that China completely dominates the EV market and EV supply chain. This is now leading to a flood of compelling Chinese electric cars being exported to global markets where Western manufacturers (excluding Tesla Inc. (NASDAQ: TSLA)) are struggling to compete with China.

Finally, in December it was announced that Canada will require all new cars and trucks to be zero-emissions vehicles by 2035. The Canadian government stated: “The Standard will ensure that Canada can achieve a national target of 100 percent zero-emission vehicle sales by 2035. Interim targets of at least 20 percent of all sales by 2026, and at least 60 percent by 2030.”

Global critical minerals update

In December we got a key U.S. political announcement that will impact EV sales and critical minerals demand in 2024 and beyond.

U.S. Foreign Entity of Concern (“FEOC”) proposal

The U.S. DoE releases proposed interpretive guidance on Foreign Entity of Concern (“FEOC”) rules. FEOC’s include China, Russia, North Korea, and Iran. Key proposals include:

Beginning 2024, companies that have >25% ownership or control by a FEOC will not be eligible for tax credits available under the Inflation Reduction Act (IRA).

Beginning in 2024, an eligible clean vehicle (for IRA credits) may not contain any battery components that are manufactured or assembled by a FEOC.

Beginning in 2025, an eligible clean vehicle may not contain any critical minerals that were extracted, processed, or recycled by a FEOC.

These rules are quite strict and it is looking like the majority of EVs sold in the USA will not qualify in 2024 and hence not receive the subsidy of up to US$7,000 per vehicle. For example, the Tesla Model 3 and Model Y base range EVs use Chinese made LFP batteries, making them both ineligible to meet the FEOC rules. Things will only get harder in 2025. Of course, this is designed to motivate auto and battery OEMs to hurry up and build a new western battery supply chain, independent of FEOC.

The FEOC proposal follows last month’s news of new guidelines for the EU Critical Raw Materials Act (“CRMA”) as discussed here. A key ruling was that “not more than 65% of the Union’s consumption of each strategic raw material comes from a single third county.”

U.S. proposal to create a ‘Resilient Resource Reserve’ for key critical minerals

As reported in December, the U.S. select committee has recommended the creation of a critical mineral reserve to protect domestic industry. The Fastmarkets report stated:

“The adoption of such a reserve is intended to “insulate American producers from price volatility and (the People’s Republic of China’s) weaponization of its dominance in critical mineral supply chain. Such a reserve would be used to sustain the price of a critical mineral when prices fall below a certain threshold and would be replenished through contribution from companies when prices are “significantly” higher”…The fund would target critical metals where there is high price volatility, low US domestic production and import dependence on China. Cobalt, manganese, light and heavy rare earths, vanadium, gallium, graphite, germanium and boron are critical minerals that fall under that category, according to the report…”

Note: Bold emphasis by the author.

Lithium

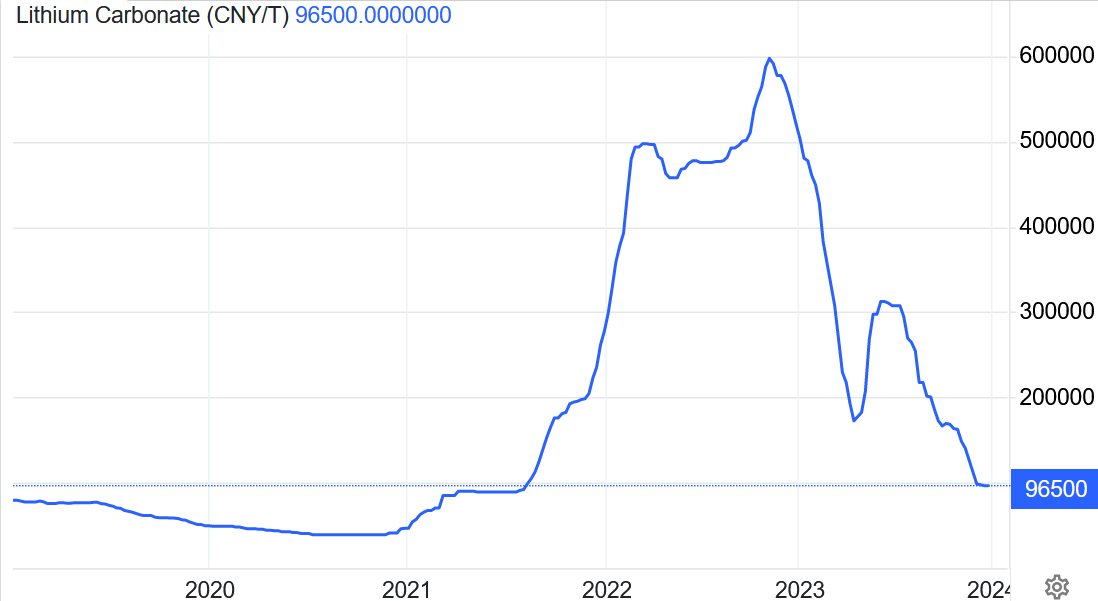

China lithium carbonate spot prices fell again in December 2023, with the price now at CNY 96,500/t (USD 13,505/t) and down 82% over the past year. Prices are now below the marginal cost of production, meaning a bottom should be found very soon (assuming EV sales hold up in 2024).

Industry participants are increasingly calling a likely bottom. For example, China Futures Co. analyst, Zhang Weixin, forecasts China’s lithium carbonate spot to bottom out between CNY 80- 90,000/t (US$11,200-US$12,600/t). Goldman Sachs is a little more bearish with a 1 year price target for China’s spot lithium carbonate of US$11,000/t.

The negative price action has not deterred SQM and Gina Reinhart’s Hancock Prospecting (private) who recently increased their bid to A$3.70 per share to takeover Australia’s Azure Minerals Limited (ASX: AZS).

In December we saw shareholders approve the Allkem Limited (ASX: AKE | TSX: AKE) – Livent Corporation (NYSE: LTHM) ‘merger of equals’ which is now expected to close by January 4, 2024. The new company is to be known as Arcadian Lithium PLC (NYSE: ALTM | ASX: LTM).

Finally, in December we got news that free markets supporter Javei Milei was elected as the new Argentina President. This is good news for those companies with mining projects in Argentina, of which there are many lithium projects under development.

The lithium carbonate spot price collapsed in 2023 and is now below the marginal cost of production and expected to form a bottom very soon

Neodymium prices fell in December to CNY 560,000/t almost 1/3 the price of the February 2022 peak. The one year outlook remains quite weak; however, this will largely depend on how China’s economy performs in 2024. A strong pickup in EV sales in 2024 could quickly change the market dynamics.

The big news in December in the rare earths market this month was China’s announcement to ban the export of rare earth processing technology. As discussed in an InvestorNews article, Western companies have been efficiently separating rare earths for some time, so this ban has minimal implications. CMI Co-Chair and rare earths expert, Jack Lifton, states: “Solvent extraction separation is a long-established practice everywhere. The issue is the production of rare earth metals and alloys and from them of rare earth permanent magnets. This is where China’s massive lead in manufacturing technology may be insurmountable. Time will tell.”

Of course, the trend for Western auto OEMs is concerning, especially following China’s recent introduction of export license permits on graphite products (including synthetic graphite, flake graphite, and spherical graphite).

Cobalt, Graphite, Nickel, Manganese, and other critical minerals

Cobalt prices (currently at US$12.91/lb) were lower the past month and continue to be very depressed. China’s slowdown and the slowdown in global electronics sales have suppressed cobalt demand at the same time as new supply from the DRC and Indonesia has risen.

One glimmer of hope for the Western cobalt producers is that the U.S. government announced in December the creation of a critical mineral ‘Resilient Resource Reserve’ (as discussed above).

Flake graphiteprices also remain very weak with prices near the marginal cost of production. Following the introduction of Chinese export license permits in December 2023 there has been some increased signs of buying activity and a slight graphite price improvement. However, the main concern for flake and spherical graphite is that lower energy input costs in China have lowered the cost of producing synthetic graphite, thereby dampening demand for flake and spherical graphite. Despite this, there are several analysts now forecasting graphite deficits to begin as soon as 2024/25 as you can read in a recent InvestorNews article here.

Nickel prices fell slightly in December to US$16,279/t. The 1 year outlook for nickel remains poor due to oversupply concerns from Indonesia. A recovering global economy and Chinese property sector will be needed to help balance the nickel market, which is currently in oversupply.

Manganeseprices also fell slightly in December and are now at CNY29.20/MTU.

2023 has been a tough year for many critical mineral prices (except for gallium, germanium, tellurium, indium, tin, and uranium – a critical mineral in Canada) as a slowing China and global economy weighed down demand at a time where supply increased. Uranium was the standout performer in 2023 with a gain of over 75%. You can read an article here from back in April 2023 where we highlighted the coming rise of uranium.

The key to watch in 2024 will be if we see lower interest rates in China trigger a China property and economy recovery. A stronger U.S. and Europe in 2024 would also help boost the global economy and demand for critical minerals. Lower interest rates in 2024 could potentially make it a great year for the auto sector and EV metals.

Wishing you all a safe and prosperous 2024 from the Critical Mineral Institute (“CMI”).

CMI Masterclass: Securing North America’s Future, A Conversation on the Critical Minerals Supply Chains with Jack Lifton

written by InvestorNews | March 20, 2024

In an insightful interview conducted by Brandon Colwell, the Director and Government Relations Liaison for the Critical Minerals Institute (CMI), with CMI Co-Chairman Jack Lifton, the focus is on the burgeoning challenges and strategic responses related to critical mineral supply chains in North America, especially in the context of China’s dominance. Jack, a veteran in the field with over 60 years of experience, points out the significant gap in subject matter expertise within the governments of the United States and Canada. This gap, he argues, hinders the effective development and implementation of policies in the mineral sector. He emphasizes the complex and time-consuming process of converting a mineral discovery into an economically viable mining project, underscoring the need for more informed and strategic decision-making in governmental investments and policy development in this domain.

Jack also delves into the recent fiscal commitments by the U.S. and Canadian governments towards critical minerals and battery manufacturing, expressing skepticism about their impact due to the governments’ limited understanding of the industry. He advocates for the inclusion of industry specialists in policy-making processes, especially in evaluating and financing mining projects. Jack raises concerns about the potential misallocation of government funds, stressing the importance of directing these investments towards those with genuine expertise and experience in the industry.

Lastly, Jack addresses the specific challenges within the critical mineral supply chain, particularly highlighting the processing segment as the most critical and challenging area. He notes the decline in North American capabilities in this area due to historical outsourcing and a lack of sustained investment in processing technologies. Jack contrasts this with China’s significant progress and dominance in processing technologies, presenting a significant challenge for North America in its bid to rebuild a competitive and independent critical mineral industry. He underscores the need for substantial investment in education and the development of expertise in process engineering and metallurgy. In conclusion, Jack discusses the broader implications for industries dependent on these minerals, such as the automotive industry, and the potential impact of government policies and market dynamics on these sectors.

The Critical Minerals Institute Report for September 2023

written by Matt Bohlsen | March 20, 2024

Welcome to the mid-September 2023 Critical Minerals Institute (“CMI”) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the IEA list of Critical Minerals.

Global critical minerals and electric vehicle (“EV”) update

Early September 2023 saw several major global events that impacted critical minerals.

The EU raised interest rates by 0.25% to a new 22 year high of 4.5%, signaling this may be the peak in rates. The US Fed is set to meet on September 20 with most analysts expecting a pause (at the current 5.5% rate, also a 22 year high), despite this week’s 3.7% CPI number, up from 3.2% the previous month. Rising interest rates in the West is slowing the economy which slows demand for most critical minerals. This has been a trend in 2023 with most critical minerals prices falling.

China announced a rate decrease last month and a decrease in the reserve rate ratio this week, all of which is starting to boost their sluggish economy. This is important as China is a key driver of critical mineral prices.

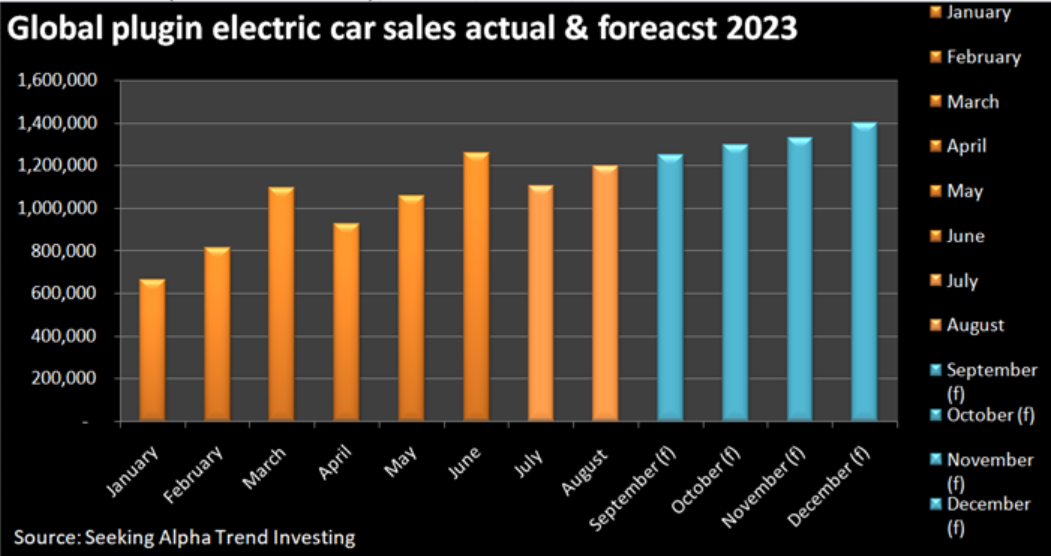

Global plugin electric car sales have generally been improving each month of 2023 after a slow start in Q1. Global EV sales reached 1.2 million units in August 2023, up 39% YoY, bringing YTD sales to 8.2 million. Sales in China have grown by 35% YTD, in EU and EFTA and UK by 30%, and in the US and Canada by 59%. 2023 sales look set to finish at ~13.5 million and 17% market share, which would be a 28% increase on 2022 (10.522 million and 13% market share). BYD Co. Ltd. (OTC: BYDDF) and Tesla Inc. (NASDAQ: TSLA) are dominating EV sales as you can read here in an article by CMI Director Matt Bohlsen.

Global plugin electric car ‘monthly’ sales in 2023 (source)

In mid-September we heard news that the Saudis and the US are in talks to secure critical metals in Africa needed to help the US with their energy transition. CMI Co-Chair Jack Lifton and CMI Director Melissa Sanderson shared their views on this controversial topic here. The Chinese have a long track record of mining in Africa, so it will be interesting to see what happens now they have sovereign wealth funds, such as that from Saudi Arabia, as competition. Glencore PLC (LSE: GLEN | OTC: GLCNF | HK: 805) has also increased its DRC activity with the recently announced backing of Tantalex Lithium Resources Corp.‘s (CSE: TTX | OTCQB: TTLXF) DRC lithium project.

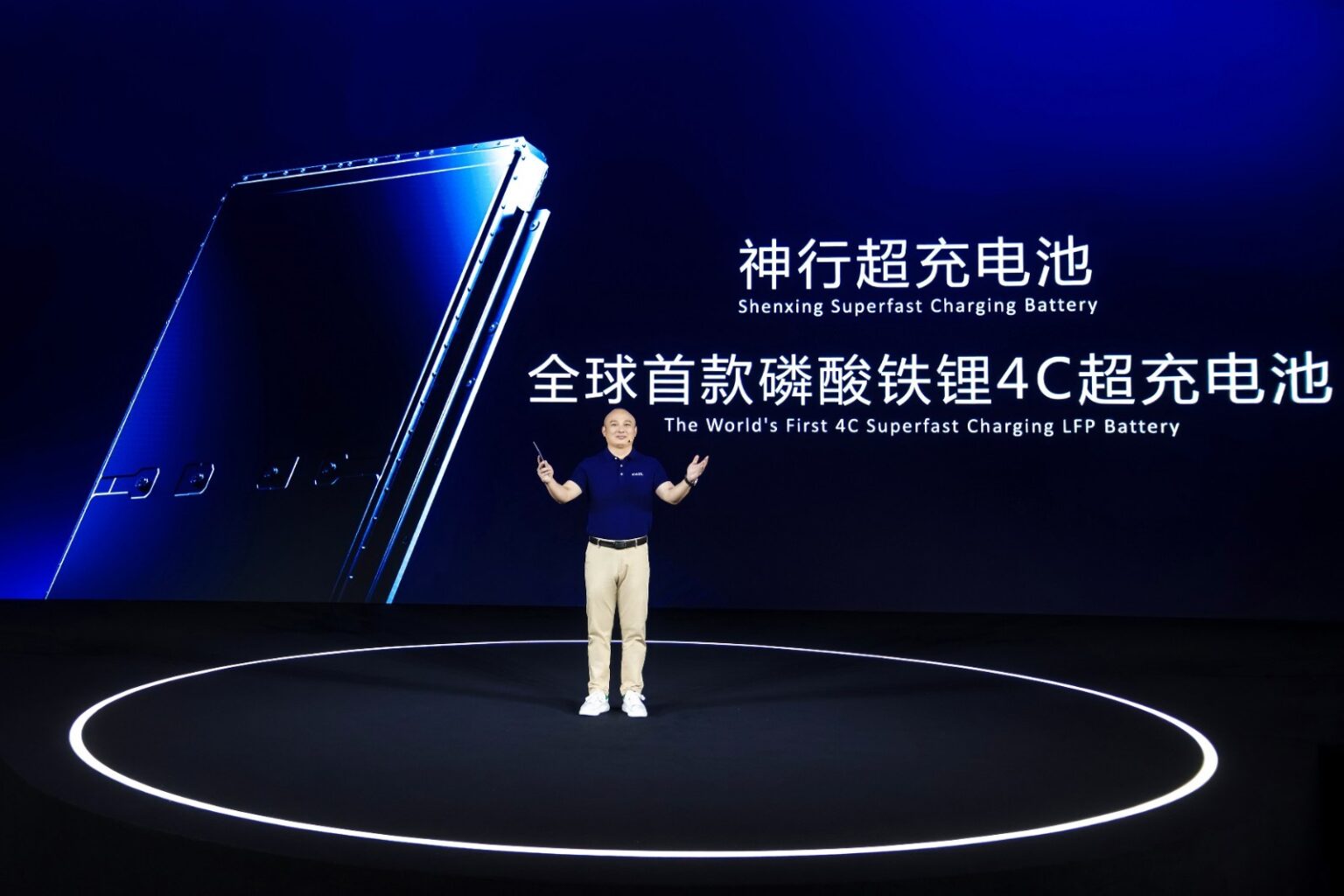

Battery news – CATL has a new superfast charging battery that can revolutionize fast charging

In some groundbreaking battery news, Contemporary Amperex Technology Co. (“CATL”) the world’s leading battery manufacturer, recently announced a new ‘superfast charging’ lithium iron phosphate (“LFP”) battery. It is reported that the new 80kWh battery, named Shenxing, is “capable of delivering 400 km of driving range with a 10-minute charge as well as a range of over 700 km on a single full charge.”

Now that’s impressive, especially given current batteries typically take about 3x longer to charge. It certainly has the potential to revolutionize fast charging speeds.

CATL has a new superfast charging LFP battery, named Shenxing (source)

Lithium

Lithium chemical spot prices fell so far in September 2023, with China lithium carbonate spot at CNY 186,500 (US$ 26,022). Prices now look to be close to reaching a bottom due to being close to the current marginal cost of production of ~US$ 25,000/t. News out of China has reported that some marginal lepidolite producers have recently been halting production.

The good news is that lower material prices have led to battery cell prices falling below the magical US$ 100/kWh for the first time in 2 years. At this price, electric cars potentially reach purchase price parity with internal combustion engines as we are now seeing in China, where almost 2 out of every 5 new cars purchased are EVs (July was 38% and 2023 YTD is 36% market share).

Of interest in September it was reported that the Australian Government said “tax breaks for lithium are ‘on the table’”. Australia is already the world’s largest supplier of lithium ore but has ambitions to grow its lithium chemicals production and to value add in other areas.

We also had a most interesting report that quotes leading lithium industry expert stating: “Mr Lithium says he’ll ‘be dead’ before the lithium market is oversupplied.”

September also saw an interesting report stating: “The world’s largest deposit of lithium may have been discovered inside a US supervolcano”. The report is referring to a study conducted by Lithium Americas Corp. (TSX: LAC | NYSE: LAC), which hypothesizes that the McDermitt Caldera contains 20 to 40 million metric tons of lithium.

Rare Earths

Neodymium (“Nd”) prices showed some strong recovery so far in September 2023 after a rough 2023 which has seen prices fall ~33% YTD. Most of the other rare earths prices have also been struggling in 2023, weighed down by a slowing China.

In an interesting rare earths September market update titled “The Chinese Rare Earths Monopoly Saga Continues”, leading global expert Jack Lifton stated: “China is doubling the size of its rare earth permanent magnet industry. It is said that this will happen by 2025. This means that China needs more, much more of the magnet precursor rare earths and all of the heavy rare earths, in particular, that it controls.”

The interesting part is that the West, boosted by the U.S Inflation Reduction Act (“IRA) and the EU Critical Raw Minerals Act (“CRMA”), is also working to rapidly build up their own supply chains of key critical metals, notably the magnet rare earths.

One such development in this direction is by Neo Performance Materials Inc. (TSX: NEO”) (“Neo”), who recently held their groundbreaking for a new permanent magnet plant in Estonia, Europe. The new plant targets Phase 1 production to reach 2,000/t pa in 2025, with Phase 2 targeting production of 5,000 tonnes/year (to support the manufacturing of ~4.5 million electric cars). The new plant will be fed by Neo’s rare earth oxide feed to come from Neo’s existing rare earth separations plant in Estonia. Another company Energy Fuels Inc. (NYSE American: UUUU | TSX: EFR) is also making great strides at developing a US supply chain for critical rare earths as you can read here. There are also several other junior rare earths companies, notably in Canada and Australia looking to supply the sector in future years.

Cobalt, Graphite, Nickel, Manganese and other critical minerals

Cobalt prices (currently at US$ 14.84/lb) continue to be very depressed in 2023, not helped by the slowdown in the global electronics sector. Some reports that China may be starting to pick up as well as some strength in superalloys (used in aerospace & military) demand gives a glimmer of hope.

Flake graphiteprices are also very weak with prices near the marginal cost of production. Flake graphite is forecast by Macquarie and others to start heading into deficit from about 2024. Leading western graphite producer Syrah Resources Limited (ASX: SYR) has been slowing production. Syrah announced in September that they had received a US$150 million conditional loan commitment for Balama approved by United States International Development Finance Corporation. The US government is supporting Syrah as they are well advanced towards construction of an active anode materials (spherical graphite) plant in the USA, which happens to have an off-take deal with Tesla (NASDAQ: TSLA).

Nickelprices have remained quite strong the past 3 years; however, oversupply concerns from Indonesia and a slowing Chinese economy have taken their toll in 2023. A pickup in China stainless steel demand will be key to watch out for.

Manganeseprices continue to be weighed down by weak Chinese demand as the Chinese housing industry continues to rebalance after years of over construction and oversupply. On the positive side manganese is starting to be used in lithium manganese iron phosphate (“LMFP”) batteries, by both Gotion Hi-Tech and CATL’s Qilin battery.

Special Thanks to the Editor of The Critical Minerals InstituteMonthly Report, Matt Bohlsen who is a CMI Director.

About the Critical Minerals Institute: The Critical Mineral Institute (CMI) is an international organization for companies and professionals focused on battery materials, technology metals, defense metals, ESG technologies and practices, the general EV market, and the use of critical minerals for energy and alternative energy production. Offering an online site that features job opportunities that range from consulting roles to Advisory Board positions, the CMI offers a wide range of B2B service solutions. Also offering online and in-person events, the CMI is designed for education, collaboration, and to provide professional opportunities to meet the critical minerals supply chain challenges.

————————

The Critical Minerals Institute was created to offer education, collaboration, and an online resource to learn about critical mineral projects, emerging technologies, legislative initiatives, government funding, human capital needs, and capital market investment opportunities. There is no charge or sign up required for access to the Critical Minerals Institute website: www.criticalmineralsinstitute.com. A range of enhanced benefits are available to individual and corporate members of the CMI, including attendance at the CMI Summit, virtual events and additional resources. For details see: www.criticalmineralsinstitute.com/cmi-membership/.

Lithium Royalty Corp.: Poised for Success as More Affiliates Reach Production

written by InvestorNews | March 20, 2024

Lithium demand continues to surge each year, despite some year on year (“YoY’) volatility in demand and prices. In 2021 the IEA forecast lithium demand to increase from 13x to 42x from 2020 to 2040. Trend Investing forecasts lithium demand to increase 35x from 2020 to 2037 as we move to a 100% electric vehicle world. Rio Tinto Group (NYSE: RIO | LSE: RIO) forecasts that the world will need 60 new lithium mines the size of Jadar. BMI forecaststhat we will need 78 new lithium mines from 2022 to 2035.

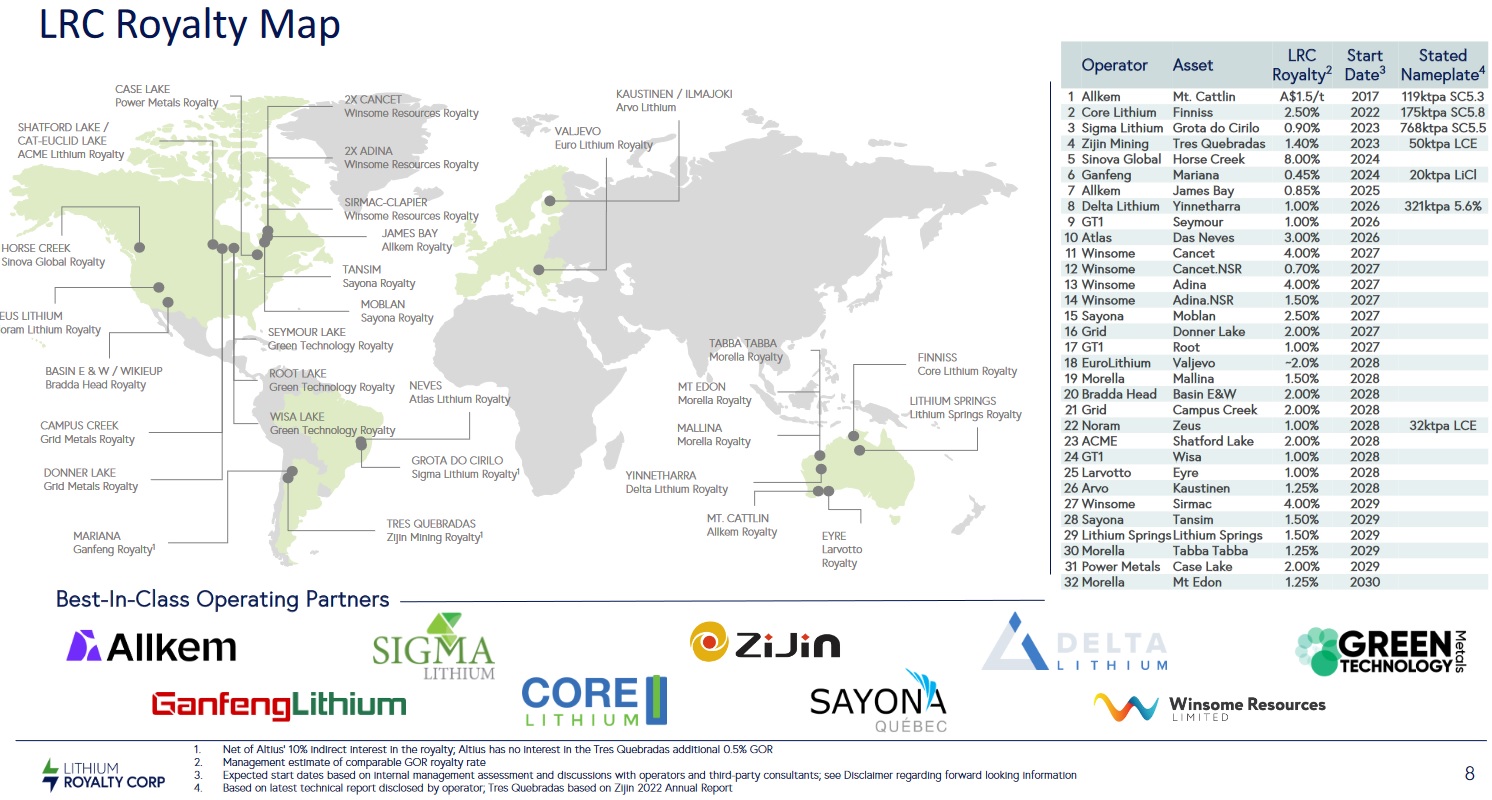

The massive demand wave coming for lithium makes for a perfect royalty play in the sector. The key advantage of royalty companies is broad exposure to many companies’ potential revenue streams. Today’s company gives investors exposure to 32 royalties across 7 countries.

Lithium Royalty Corp. (TSX: LIRC) (“LRC”)

LRC is a pure-play battery metal royalty company with a focus on lithium royalties. LRC has been steadily acquiring royalties since 2018 with a focus on safe mining jurisdictions. The large majority are lithium royalties in mines/projects located in South America, Canada, and Australia (see charts below).

Lithium Royalty Corp. (“LRC”) global portfolio of 32 royaltieswith afocus on lithium

LRC lithium royalty revenues with more set to potentially come online in the near term

Looking at the list in the chart above we see that LRC already has several revenue streams from key lithium producers including Allkem Limited‘s (ASX: AKE | TSX: AKE) Mt Cattlin Mine, Core Lithium Limited‘s (ASX: CXO) Finniss Mine, and SIGMA Lithium Corporation‘s (NASDAQ: SGML | TSXV: SGML) Grota do Cirilo Mine plus others potentially to follow in the near term including Zijin Mining Group‘s Tres Quebradas Project, Ganfeng Lithium Group‘s Mariana Project, and Delta Lithium Limited‘s (ASX: DLI) Yinnetharra Project.

Also, all going well, by ~2027 Winsome Resources Ltd.‘s (ASX: WR1) Cancet and Adina Projects (potential ~50Mt resource in the making) look very promising based on drill results so far, as does Sayona Mining Limited‘s (ASX: SYA | OTCQB: SYAXF) Moblan JV which already has a Total Resource of 51.4Mt @ 1.31% Li2O. Both projects are in Canada.

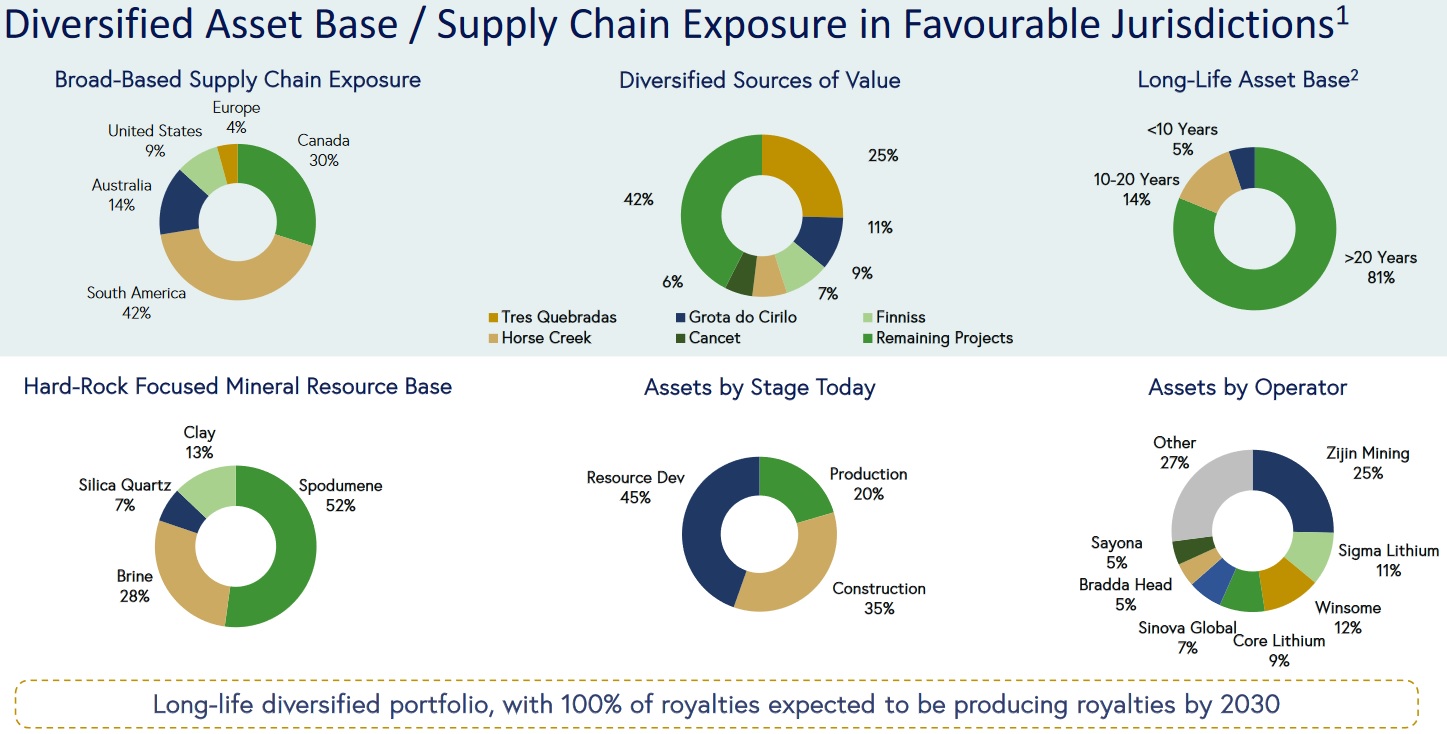

LRC’s portfolio is advancing well with 20% in production

LRC’s portfolio has grown since 2018 to now include 32 royalties.

Country exposure of the LRC portfolio is South America (42%), Canada (30%), Australia (14%), USA (9%), and Europe (4%). This would be considered a safe mix of countries, noting the South America exposure is mostly Argentina and Brazil.

Portfolio value is nicely diversified with 42% of the portfolio in the others category. The largest holding by value is the Zijin Mining’s Tres Quebradas Project (25%); however, the next largest is only at 11%.

Hard rock spodumene assets dominate the portfolio at 52% which is seen as a positive considering they are usually faster and cheaper to bring into production than other lithium projects.

20% of the LRC royalty portfolio is already in production, 35% are in the construction stage, and 45% are in the development stage.

The overall quality of the portfolio looks solid with most companies standing a good chance at being producers by 2030.

A summary of LRC’s royalty portfolio characteristics

Some advantages of royalty companies include – Diversification across a large portfolio is much lower risk than just owning a few lithium miners and exposure to the underlying commodity price (lithium) with minimal project execution risk.

LRC’s Q2, 2023 financial results

LRC announced Q2, 2023 results on August 14, 2023, which included royalty revenue up 98%, gross profit up 280%, and a small loss of C$0.02 per basic share. LRC’s royalty income for Q2 was C$838k. The announcement gives a lot more details on their royalty portfolio, including the newer acquisitions, and mentions a new credit agreement with the National Bank of Canada for C$25 million.

Closing remarks

The lithium boom looks to be very well established and still has about 2 decades to run as the world transitions to sustainable energy (energy storage with Li-ion batteries) and electric vehicles.

Buying a lithium royalty portfolio is a safer way to gain broad exposure to a number of companies. The main risk is that if the royalty portfolio companies don’t make it to production. Valuation is not an easy task so investors may need to rely on analyst’s price targets.

Lithium Royalty Corp. trades on a market cap of C$688 million. The August 2023 company presentation stated LRC’s net asset value at C$1,061 million.

LRC looks like a good quality royalty play on lithium. The key will be lithium prices and how the underlying portfolio of companies perform. Stay tuned.

Elcora Ramps Up Manganese Sales with Vanadium Prospects on the Near-Term Horizon

written by InvestorNews | March 20, 2024

Elcora Advanced Materials Corp. (TSXV: ERA) (“Elcora”) is a relatively new manganese ore producer and has other battery material projects containing vanadium, graphite, and copper located in Morocco and Canada. Elcora also has exposure to anode materials and graphene. Demand for manganese remains strong both for the steel industry, but also for lithium-ion batteries containing manganese, typically used for electric vehicles.

Elcora’s goal is to be a globally competitive extractor and processor of battery-grade minerals and metals. They plan to do this by becoming a vertically integrated battery materials company and use their cost-effective process to purify high-quality battery metals and minerals that are commercially scalable.

How Elcora is anticipating and responding to the Global Energy Revolution

Manganese production has started in Morocco and new orders are rolling in

As announced in June 2023, Elcora delivered its first manganese order of 500 metric tons of 37%+ high-quality manganese from their Morocco Mine. Elcora owns theAtlas Fox Project in Morocco, which includes the Beni Mellal Manganese Deposit/Mine and the Ouarzazate Project (includes the Omar Mine). Elcora plans to rapidly ramp up their manganese production from these projects with an 8-12 month production target of 20,000 tonnes per month of 37% manganese ore.

As announced on July 6, 2023, Elcora has secured two more orders for a total of 1,500 metric tons of 37%+ manganese ore set to be delivered by the end of July 2023, thereby securing sales revenue for the second month in a row for Elcora.

Vanadium production plans with sales potentially as soon as only 6 months away

Elcora is currently developing their Atlas Lion Vanadium Project in Morocco.

Elcora announced in June 2023 the completion of the first phase of vanadinite comminution testing. The result was 8.9% vanadium concentrate. Elcora then began shipping bulk samples for trial tests in smelters in Asia and Europe, and if results come back positive Elcora say they could potentially have concentrate sales revenue in as quick as 6 months.

The short-term plan is to build a semi-mobile concentrator plant to produce a 46% lead (“Pb”) and 9%+ vanadium (“V”) concentrate, with a ramp up to 2,500t/month of concentrate production. Elcora’s mid-term plan is to build a hydrometallurgical plant scheduled to produce 1,500 t/year of 99.99% V and 15,000t/year 99.99% Pb.

Elcora’s graphite products

In addition to manganese, vanadium and lead; Elcora has developed the technology to produce flake graphite, advanced natural graphite anode powder and graphene. Elcora states:

“Elcora has developed a unique low-cost effective process to make commercially scalable graphite nanomaterials ranging from micro-graphite to graphene.”

Flake graphite and anode powder are in growing demand for electric vehicles and energy stationary storage where the graphite is used in the anode part of the battery. Graphene has numerous potential uses and is known as a new wonder material.

“Elcora has been structured to become a vertically integrated graphite & graphene company that mines, processes, refines graphite, and produces both the graphene and end graphene applications. Elcora’s graphene production system is suitable for use with many different graphite sources and has produced industry-leading quality graphene.“

Closing remarks

Elcora is executing well on their plans to become a vertically integrated battery materials company. Elcora already has a strong history within the flake graphite, anode powder, and graphene sectors.

Near-term catalysts will be further sales revenue of manganese concentrate from their Moroccan Mine and potentially good news on their vanadium concentrate smelting trials. Looking out a year or so from now Elcora should potentially have ramped up their vanadium concentrate production to 20,000t/month and vanadium concentrate to 2,500t/month. Beyond that, the plan is to potentially produce a final product via more processing thereby value adding to their current situation.

Elcora Advanced Materials trades on a market cap of only C$6 million. Exciting times for Elcora, especially if they can continue to execute well and bring in growing revenues in 2023.

Incompetent Experts: For Critical Minerals, this is not an Oxymoron.

written by Jack Lifton | March 20, 2024

I am often asked to introduce technology metals based ventures to the sourcing/purchasing activities of the OEM automotive industry, based in Detroit, where I have lived for most of my 83 years, and for which I was a supplier of production parts and engineered materials for more than 30 years.

I find an almost complete lack of understanding of marketing and sales to the OEM automotive industry to be common among technology metals miners and refiners, who are of course the anchor companies of any and all production parts’ supply chains.

In the past this has been of little interest to the OEM automotive industry due to its standard operating procedures of choosing preferred vendors, known in the industry as Tier One Vendors, who then became responsible for choosing their own vendors of parts and services, subject to the acceptance of the Tier One product by the end-use customer’s internal Production Part Acceptance Protocol (PPAP), and even then, subject to on-time delivery, in the agreed quantities, to the customer’s specification at the agreed pricing. Failure in any one of these required categories could, at the discretion of the OEM, result in the “desourcing” of the (approved otherwise) vendor. To ensure security and continuity of supply, the end-user normally would have a primary Tier One vendor and at least two alternates, each of which would normally get a small percentage of the total “buy” to keep it in the game. The alternates would be required to have the capability and the capacity to supplement or even replace the primary in the event of partial, or even total, non-performance by the primary.

Such Tier One Vendors are of course operating companies with an existing output or capability to produce the parts in question. They will have positive cash flow and, typically, are public companies with a listing on a major exchange and a substantial market cap. The core competency of each and every company in the total supply for the part chain would be required and it is understood to be guaranteed to the OEM by the Tier One.

Nowhere is the decay of proven, verifiable, competence as the sine qua non “standard” more apparent than in the, most likely to be, disastrous exemption of the PPAP standard in the OEM automotive industry for lithium-ion battery manufacturing. Rare earth permanent magnet motor manufacturing may soon be compromised by the same decay of standards.

The pathetic and jejune industry “experts” who not only analyze but, even worse, advise the OEMs on the sourcing of production parts based on critical metals are unified by their almost complete lack of practical experience, education and knowledge of the origin, processing, fabricating and manufacturing engineering at commercial scale of the total supply chains for the critical metals enabled devices upon which the motive power, “engine” management, and supply of information for the drivers of EVs depend.

Last week we were told by this “expert” class of journalists and advisors that both germanium and gallium were “rare earths” and that they were used in batteries. Both “expert” statements were completely wrong and misleading.

Earlier this year we were told and continue to be told by an “expert” firm that the economy needs “only 300” more lithium mines to meet the needs of a zero-carbon economy. Apparently, these fools think that there is not only a standard size lithium mine, but also a standard predictable demand for lithium. Mining engineers and mining company CFOs will be delighted to find out about this development.

I’m going to try from now on to list the Erroneous Critical Minerals Supply and Demand statement of the Week each Friday.

Attention manufacturing executives and policy makers: You need to do a due diligence review of your “experts,” before you act on their advice.

Hint: Make sure that their jobs don’t depend on always agreeing with you.

A final comment: Germanium and gallium are critical to chip manufacturing, LEDs, and military optics. The “CHIPs” act and the “IRA” pledged more than $50 billion in subsidies for domestic chip manufacturing and battery manufacturing, but not ONE CENT for domestic gallium or germanium production.

Is this how policy experts in Washington think we can become independent of Chinese dominance in critical minerals production and processing?

Consolidated Lithium Metals aims to help supply North America with the surging demand for lithium

written by InvestorNews | March 20, 2024

Demand for lithium-ion batteries (and hence lithium) in North America is set to surge 13.8 fold from 2022 to 2035. The US Inflation Reduction Act has led to a massive increase in planned battery manufacturing in North America to support a North American supply chain for electric vehicles and energy stationary storage.

The main problem now is supplying these planned battery factories with key raw materials, especially lithium. Today’s company is focused to fill that lithium supply gap.

NorthAmerican lithium-ion battery manufacturing is forecast to increase from 47 GWh in 2022 to 650 GWh in 2035(a 13.8x increase)

Consolidated Lithium Metals Inc.(TSXV:CLM | OTCQB: JORFF) (“CLM”) (formerly Jourdan Resources Inc.) is a North American hard rock lithium explorer and developer. CLM is focused on exploration in Quebec for hard rock spodumene lithium in the heart of the Abitibi Greenstone Belt.

CLM’s lithium projects are located ~30kms north of Val-d’Or with over 18,000 hectares of claims strategically located adjacent to the North America Lithium (“NAL”) (Sayona Mining Limited (ASX: SYA | OTCQB: SYAXF) 75%: Piedmont Lithium Inc. (Nasdaq: PLL | ASX: PLL) 25%) restarted lithium operation.

Location map showing CLM’s projects (red shading) 30kms north of Val-d’Or, Quebec, Canada

CLM’s 4 lithium projects have drill-ready targets with confirmed lithium bearing pegmatite already identified on two flagship projects, Vallée and Baillargé. The vast majority of claims are 100% owned by CLM.

CLM’s 4 lithium projects are:

Vallée JV (75% CLM: 25% SYA) & East Vallée (100% CLM) – The Vallée JV Project is located adjacent to and along strike of the NAL mining operation claims. The mineralized spodumene pegmatite dykes that NAL is mining continue directly onto the claims. A C$4 million, 14,000 meter, drill program is planned for 2023. Sayona can earn up to 50% interest by solely funding C$10 million in exploration in the next 3 years. East Vallée is at an earlier stage but also shows strong potential.

Baillargé(100% CLM) – Potential high-grade lithium in 3 dyke systems with several hundred meters of strike length and with a C$1.5 million, 4,500 metre, diamond drilling exploration program underway. A small drill program in 1955 encountered high-grade lithium averaging 2.48% Li2O over 2.19 metres.

Preissac-LaCorne – Hosts multiple lithium showings along the producing Vallée Lithium Trend. CLM state: “The Preissac-La Corne property covers three (3) underexplored prospective areas that include series of showings which host significant amounts of mineralization in Lithium (Li) Molybdenum (Mo), Cesium (Cs), Rubidium (Rb), Tantale (Ta), Niobium (Nb) and Berylium (Be) associated with granite and pegmatite.”

Duval – Early stage grassroots project with several historical lithium showings over a 6.5 km section of the highly prospective Vallée Lithium Trend.

CLM’s 4 lithium projects near the very large NAL lithium restarted mine and on, or near, the Vallée Lithium Trend

CLM is an exciting lithium junior with 4 very well located lithium projects adjacent and near the NAL lithium mine and operation claims in Quebec. CLM is actively exploring for lithium with over 18,000 metres of drilling planned and underway on CLM projects in 2023.

Consolidated Lithium Metals Inc. trades on a market cap of C$27 million and is in process of completing the last stage of an up to C$2 million flow through financing. The current drill program results are a key factor to watch in the near term. Any nice lithium drill hits should be very well received by the market given the region’s history and large NAL mine nearby. One to follow closely in 2023.