Riding the EV Revolution Rollercoaster Amid the West’s Electric Car Climbdown

written by Tracy Weslosky | February 5, 2024

Embarking on the electric vehicle (EV) revolution journey has felt like being on a rollercoaster filled with surprising developments, especially when we consider the insights from Jack Lifton, the Co-Chairman of the Critical Minerals Institute (CMI), who recently shared his thoughts on the opinion published in The Telegraph titled The West’s humiliating electric car climbdown has begun. Lifton’s sharp analysis pierces through the prevailing chatter, offering a lucid view of the EV market’s complex trajectory. He navigates us through the shifting sands of government and auto manufacturers’ strategies, the intensifying competition from the East, and the shifting tides of consumer demand. Lifton’s insights serve as a guiding light for deciphering the intricate forces shaping the EV landscape.

The recent shifts in the electric vehicle (EV) industry, as observed by Jack Lifton, Co-Chairman of the Critical Minerals Institute (CMI) and a notable expert in the field of technology metals, illuminate the complex interplay of government policy, market dynamics, and consumer preferences. Lifton’s insights provide a nuanced understanding of the challenges and potential misalignments within the EV sector, particularly as it pertains to the impact of government strategies, competition, and market dynamics, and the role of consumer demand in shaping the industry.

Impact of Government Strategies on the EV Market

Lifton critiques the effectiveness of state-led industrial strategies in the rapidly evolving EV market, highlighting the retreat of major manufacturers like Renault and Volvo from their ambitious EV initiatives. This move, compounded by a reduction in government support, raises questions about the foresight and adaptability of such strategies. Lifton notes, “It shows that, as always, the invisible hand of the market rules… the automotive companies have suddenly discovered the market’s supply demand… government doesn’t dictate markets.” This observation underscores the limitations of state intervention in forecasting and influencing market demands and suggests a need for more market-responsive approaches.

Competition and Market Dynamics

The competition from Chinese manufacturers has significantly influenced the trajectory of the Western electric vehicle industry. Lifton points out the stark reality facing Western EV manufacturers, stating, “The cost of making electric vehicles in the United States is too high… People are buying a Chevrolet EV for $50,000. That car cost $100,000 to make.” This price disparity, alongside the aggressive expansion of Chinese EV manufacturers into global markets, underscores the challenges Western companies face in maintaining competitiveness. The scenario posits a crucial reflection on the sustainability of the current business models and the need for innovation and efficiency improvements.

The Role of Consumer Demand in Shaping EV Industry

Lifton’s commentary on the shift in consumer preference back to petrol models reveals a significant misalignment between the production of EVs and actual market demand. He remarks on the sudden interest in hybrids by companies like General Motors, indicating a rapid strategic pivot to align with consumer preferences for efficiency and practicality. Lifton argues, “Hybrids… maximize the efficiency of electric and internal combustion and therefore will allow us to have the longest supply of fuels.” This perspective highlights the importance of flexibility in product offerings and the need to closely monitor and adapt to consumer demand trends.

Jack Lifton’s insights offer a candid reflection on the electric vehicle industry’s current state, pointing towards a future where adaptability, market intelligence, and innovation are paramount. His observations remind us that success in the EV market is not solely about ambitious government strategies or manufacturing prowess but about understanding and responding to the nuanced dance of supply, demand, and the global competitive landscape. As we consider the path forward, Lifton’s analysis underscores the importance of striking a balance between visionary goals and the pragmatic realities of consumer needs and market dynamics. The electric vehicle revolution is far from over, and its success will hinge on the industry’s ability to navigate these challenges with agility and foresight.

Curtis Moore on Energy Fuels’ competitive advantage in the North American rare earths market

written by InvestorNews | February 5, 2024

In an InvestorNews interview, Tracy Weslosky spoke with Curtis Moore, Senior VP of Marketing & Corporate Development at Energy Fuels Inc. (NYSE American: UUUU | TSX: EFR). Curtis discussed Energy Fuels’ focus on monazite sand, highlighting its high neodymium-praseodymium (NdPr) content, which provides a cost processing advantage over other rare earths bearing ores like bastnaesite. He explained that monazite’s value is enhanced by its higher concentration of NdPr, essential for permanent rare earth magnets used in EVs and wind turbines, and its higher concentration of heavy rare earths. Curtis noted that while monazite has higher uranium and thorium levels than bastnaesite, Energy Fuels can efficiently process these elements at their uranium mill. He emphasized Energy Fuels’ unique advantage in handling the naturally occurring uranium and thorium in rare earth bearing ores, a significant challenge for other companies. This capability allows them to potentially monetize these elements, especially as thorium markets mature.

Curtis also addressed a key question he wishes people would ask more often: why Energy Fuels is likely to succeed in the rare earth sector where many others have failed? He attributed their potential success to their inherent advantages in processing rare earth bearing ores and producing advanced materials. These advantages include their experience with solvent extraction, a technology crucial for producing separated rare earth oxides, and their existing infrastructure at the White Mesa Mill in Utah. Curtis highlighted their $25 million investment in a rare earth separation circuit at the mill, which is expected to be operational in the first quarter of 2024, with a capacity to produce about 1000 metric tons of NdPr oxide per year, enough for 500,000 to 1,000,000 EVs annually. He expressed high confidence in their ability to succeed in the rare earth industry due to these factors.

Don’t miss other InvestorNews interviews. Subscribe to the InvestorNews YouTube channel by clicking here

About Energy Fuels Inc.

Energy Fuels is a leading US-based critical minerals company. The Company, as the leading producer of uranium in the United States, mines uranium and produces natural uranium concentrates that are sold to major nuclear utilities for the production of carbon-free nuclear energy. Energy Fuels recently began production of advanced rare earth element (“REE“) materials, including mixed REE carbonate, and plans to produce commercial quantities of separated REE oxides in the future. Energy Fuels also produces vanadium from certain of its projects, as market conditions warrant, and is evaluating the recovery of radionuclides needed for emerging cancer treatments. Its corporate offices are in Lakewood, Colorado, near Denver, and substantially all its assets and employees are in the United States. Energy Fuels holds two of America’s key uranium production centers: the White Mesa Mill in Utah and the Nichols Ranch in-situ recovery (“ISR“) Project in Wyoming. The White Mesa Mill is the only conventional uranium mill operating in the US today, has a licensed capacity of over 8 million pounds of U3O8 per year, and has the ability to produce vanadium when market conditions warrant, as well as REE products, from various uranium-bearing ores. The Nichols Ranch ISR Project is on standby and has a licensed capacity of 2 million pounds of U3O8 per year. The Company recently acquired the Bahia Project in Brazil, which is believed to have significant quantities of titanium (ilmenite and rutile), zirconium (zircon) and REE (monazite) minerals. In addition to the above production facilities, Energy Fuels also has one of the largest NI 43-101 compliant uranium resource portfolios in the US and several uranium and uranium/vanadium mining projects on standby and in various stages of permitting and development.

Disclaimer: Energy Fuels Inc. is an advertorial member of InvestorNews Inc.

This interview, which was produced by InvestorNews Inc. (“InvestorNews”), does not contain, nor does it purport to contain, a summary of all material information concerning the Company, including important disclosure and risk factors associated with the Company, its business and an investment in its securities. InvestorNews offers no representations or warranties that any of the information contained in this interview is accurate or complete.

This interview and any transcriptions or reproductions thereof (collectively, this “presentation”) does not constitute, or form part of, any offer or invitation to sell or issue, or any solicitation of any offer to subscribe for or purchase any securities in the Company. The information in this presentation is provided for informational purposes only and may be subject to updating, completion or revision, and except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any information herein. This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein.

Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. This presentation should not be considered as the giving of investment advice by the Company or any of its directors, officers, agents, employees or advisors. Each person to whom this presentation is made available must make its own independent assessment of the Company after making such investigations and taking such advice as may be deemed necessary. Prospective investors are urged to review the Company’s profile on SedarPlus.ca and to carry out independent investigations in order to determine their interest in investing in the Company.

The Critical Minerals Institute Report (CMI 11.2023): Neodymium price is down 33% over the Past Year, Record Plug-In EV Car Sales for September

written by Matt Bohlsen | February 5, 2024

Welcome to the November 2023 Critical Minerals Institute (“CMI”) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the CMI list of critical minerals (CMI List of Critical Minerals) or visit the CMI Library where critical minerals expert Alastair Neill tracks the latest critical mineral lists worldwide.

Global macro view

High interest rates (and cost of living increases) in most Western countries continue to be a drag on the global economy. Europe, in particular, continues to struggle. Last month saw a welcome fall in US inflation to 3.2%pa suggesting the US Fed may not need to raise rates at their December 12-13 meeting.

China has been ramping up support for their beaten down property sector and economy. The key hope for 2024 is that China’s property market stabilizes and their economy improves. Some early positive signs are appearing.

The Russia-Ukraine war continues as does the Hamas-Israel war. The outcomes of these conflicts can impact oil prices and hence inflation, meaning they are key events to monitor as we head into 2024.

Global electric vehicle (“EV”) update

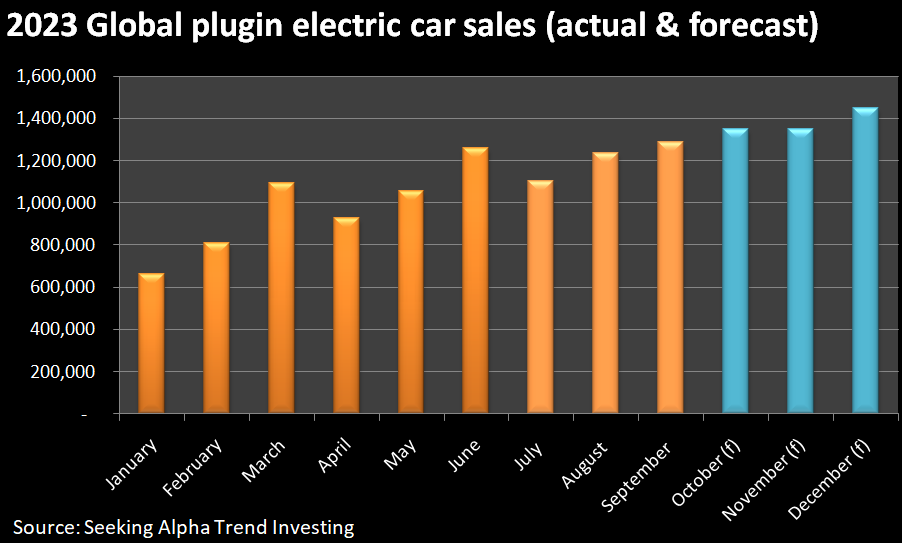

November 2023 saw strong EV sales reported for September 2023. Global plugin electric car sales for September were a record 1,291,000 up 23% YoY to 17% market share.

In September, China sales were up 22% YoY to 37% share. Europe sales were up 15% YoY to 25% share. USA sales were up 59% YoY to 9.9% share.

Results look very promising for October 2023 with global plugin electric car sales on track to reach or exceed ~1.35 million. China’s October sales have been announced and they hit a new record of 956,000 sales.

2023 sales look set to finish at ~13.6 million and 17% market share, which would be a 29% increase on 2022 (10.522 million and 13% market share). A 29% growth rate in 2023 would be a significant slowdown on the 56% growth rate achieved in 2022.

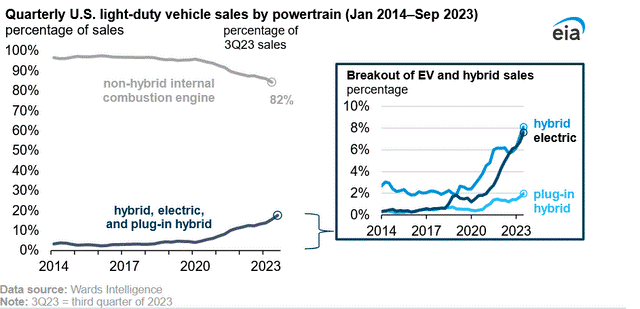

Regarding US Battery Electric Vehicle (“BEV”) car sales, the EIA recently reported that “BEV prices are now within $3,000 of the overall industry average transaction price for light-duty vehicles.”

Global plugin electric car ‘monthly’ sales in 2023 (source)

Finally, reports of a slowdown in US EV demand are ‘fake news’. US electric car sales are achieving record sales in 2023 as we saw in the US Energy Information (“EIA”) announcement on November 27, 2023. The chart below gives a good summary. The fact that Ford Motor Company (NYSE: F) and General Motors (NYSE: GM) are slowing down their EV production plans due to weak EV sales says more about their failure to produce well priced and desirable EVs rather than the US market as a whole. There is a similar situation with Volkswagen AG in Europe. Both BYD Company Limited (OTC: BYDDF) and Tesla Inc. (NASDAQ: TSLA) continue to rapidly expand their production and EV sales. Legacy automakers need to up their game or be left behind by the EV leaders Tesla and BYD who continue to go from strength to strength.

Electric vehicles and hybrids grow to a record-high 18% of U.S. light-duty vehicle sales (source)

Global critical minerals update

Western governments, led by the USA, have continued to ramp up support for a Western EV and battery supply chain. In November we had two key announcements:

On October 31 The Government of Canada announced: “Government of Canada to enhance critical minerals sector with launch of $1.5 billion Infrastructure Fund…“Our investments will help the mining industry develop important enabling and supporting infrastructure such as roads and energy facilities required prior to construction of mines.”

On November 15 Energy.govannounced: “Biden-Harris Administration announces $3.5 Billion to strengthen domestic battery manufacturing…As part of President Biden’s Investing in America agenda, the funding will create new, retrofitted, and expanded domestic facilities for battery-grade processed critical minerals, battery precursor materials, battery components, and cell and pack manufacturing…”

These are positive developments, however not enough is being done upstream to support the critical minerals ‘miners’ to get into production. The Canadian Government’s announcement above is reasonably well directed, but it is to be spread over 7 years and is nowhere near enough money for what is needed. The US Government’s effort is further supported on the back of previous announcements as part of the 2022 Inflation Reduction Act (“IRA”) which intends to spend US$369 billion in energy security and climate change programs over ten years. However, most of the funds so far are to support battery manufacturing and EV plants and subsidies. More funds need to be put to use to help support the critical mineral mining companies, particularly as key critical minerals such as lithium is the bottle neck to ramp up western production of EV’s and energy stationary storage.

The IRA has been extremely successful so far at bringing EV and battery investments to the USA. For example, in November we heard a report of yet another US factory being planned with Toyota planning to invest US$8 billion in a North Carolina battery plant to increase EV capacity.

Over in Europe, the EU Critical Raw Materials Act (“CRMA”) has progressed to the next stage with ‘provisional’ agreement achieved, noting the increased focus on recycling. On November 13, the European Union Council announced:

“The Council and the European Parliament today reached a deal on the proposed regulation establishing a framework to ensure a secure and sustainable supply of critical raw materials, better known as the Critical Raw Materials Act. The agreement is provisional, pending formal adoption in both institutions…The political agreement reached today keeps the overall objectives of the original proposal but strengthens several elements. It includes aluminium in the list of strategic and critical materials, reinforces the benchmark of recycling, clarifies the permitting procedure for strategic projects, and requires relevant companies to perform a supply-chain risk assessment on their sourcing of strategic raw materials…On the global stage, the regulation identified measures to diversify imports of critical raw materials ensuring that not more than 65% of the Union’s consumption of each strategic raw material comes from a single third country…The provisional agreement keeps the benchmarks of 10% for extraction of raw materials and 40% for processingbut increases the benchmark for recycling to at least 25% of EU’s annual consumption of raw materials…The provisional compromise also unifies the timings of the permit procedure. The total duration of the permit granting process should not exceed 27 months for extraction projects and 15 months for processing and recycling projects…Next steps. The provisional agreement reached with the European Parliament now needs to be endorsed and formally adopted by both institutions.”

Note: Bold emphasis by the author. Synthetic graphite was also added.

In November we did hear some more reports on sodium-ion batteries and how they can help meet the incredible battery demand needed for the green energy transition. Sodium-ion can help around the margin, but it will not replace lithium-ion. Sodium-ion batteries will be used for energy stationary storage and cheap (<US$10,000) low-end, low-range, small EVs. Beyond that, the sodium-ion battery as exists today will have limited demand. CATL is leading the way with sodium-ion battery manufacturing and is one to watch.

“A total of 388 new mines must be built to produce the metals required to meet international government mandates for electric vehicle…The International Energy Agency (IEA) suggests that to meet international EV adoption pledges, the world will need 50 new lithium mines by 2030, along with 60 new nickel mines, and 17 new cobalt mines…Historically, however, mining and refining facilities are both slow to develop and are highly uncertain endeavors plagued by regulatory uncertainty and by environmental and regulatory barriers. Lithium production timelines, for example, are approximately 6 to 9 years, while production timelines (from application to production) for nickel are approximately 13 to 18 years, according to the IEA…The risk that mineral and mining production will fall short of projected demand is significant, and could greatly affect the success of various governments’ plans for EV transition.”

Note: Bold emphasis by the author.

Lithium

China lithium carbonate spot prices fell significantly in November 2023, with the price now at CNY 126,500/t (US$ 17,870/t) and down 78% over the past year. At these prices, marginal cost lithium producers in China are shutting down and Albemarle Corporation (NYSE: ALB) and JV partners at the Greenbushes Mine are considering production cuts in H1, 2024. A bottom is likely to form soon at or above CNY 100,000/t assuming global EV sales hold up at current rates of about 30% growth in 2023 and 2024.

Lithium takeovers continue despite weak sentiment

Chile’s SQM recently increased their takeover offer for Azure Minerals Limited (ASX: AZS) to US$900 million. Meanwhile, Mineral Resources Limited (ASX: MIN) has been building an equity stake in Azure Minerals as well as buying a 19.85% equity interest in Wildcat Resources Limited (ASX: WC8), another WA lithium junior miner. Not to be outdone, Australian billionaire Gina Reinhart has recently bought a 19% interest in Azure Minerals. Reinhart was active in buying Liontown Resources Limited (ASX: LTR), ultimately leading Albemarle to withdraw their takeover offer.

At least it looks like the Allkem-Livent merger is still going ahead. Allkem Limited (ASX: AKE) and Livent Corporation (NYSE: LTHM) have received all required regulatory approvals globally for their ‘merger of equals’, expected to close by January 4, 2024.

All of this takeover activity from the major lithium companies suggests that we are near a bottom in the lithium price cycle and that the mid to long-term outlook for lithium remains very strong.

Rare Earths

Neodymium (“Nd”) prices fell in November and are currently sitting at CNY 610,000/t. The neodymium price is down 33% over the past year, but still well above the 2019 price.

On November 16 Rare Element Resources Ltd. (OTCQB: REEMF) announced receipt of the final NEPA approval for their rare earth processing and separation demonstration plant to be built in Upton, Wyoming, USA. The news stated: “The Company is awaiting next stage budget approval from the DOE, which is providing approximately 50% of the project costs, to commence construction.”

Cobalt, Graphite, Nickel, Manganese and other critical minerals

Cobalt prices (currently at US$14.85/lb) remained flat the past month and continue to be very depressed. China’s demand for NMC cathode material for EVs has been weak as LFP cathodes (no nickel or cobalt) have gained in popularity.

Flake graphiteprices also remain very weak with prices near the marginal cost of production. The big news in the graphite world is China’s intention to temporarily enforce export license permits on three synthetic graphite-related items and six natural graphite-related items, starting from December 1, 2023. As a result, we have seen some buying activity and flake graphite prices rising in Europe.

Nickel prices fell further to US$16,593/t in November due to oversupply concerns from Indonesia and the depressed Chinese property sector.

Can the Western graphite and anode industry rise to meet China’s challenge?

written by Matt Bohlsen | February 5, 2024

China to impose some graphite and processed graphite materials ‘export permits’ from December 1, 2023

Last week it was reported that China, the world’s top graphite producer plans to curb exports of key battery material by implementing export permits for some graphite products from December 1 to protect national security. Another report stated: “China graphite export restrictions could hinder ex-China anode development….if it lasts into the longer term, it is likely to accelerate the build-out of a localized graphite and battery anode supply chain outside China.”

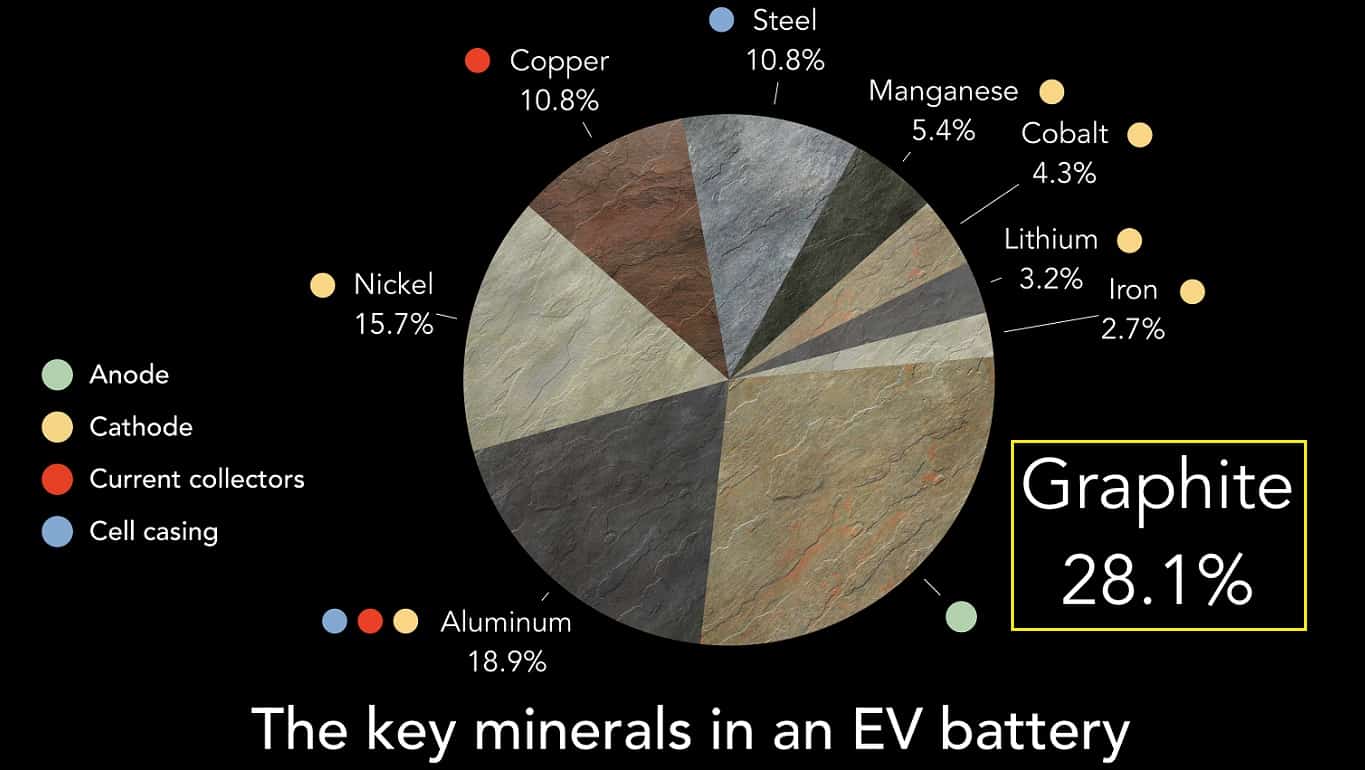

Graphite is the number one metal required for lithium-ion batteries making up about a 28% share. It is used in the anode.

The key metals and minerals in a battery of an electric vehicle

The world is very dependent upon China to supply processed graphite material and anodes for Li-ion batteries

The reason why this is huge news in the graphite world is that China produces 67% of global natural flake graphite supply and refines more than 90% of the world’s graphite into active anode material (typically spherical graphite). If China were to deny or delay permits for spherical graphite it will cause major problems for anode manufacturers outside China, such as those in South Korea, Japan, or North America.

China currently produces ~77% of global lithium-ion batteries and 75-80% of global electric cars, thereby completely dominating the industry. If the West is shut out from sourcing processed EV battery materials from China then they will have a major problem producing their own EVs. China plans to prioritize EV battery materials for their own needs. This is why President Biden introduced the Inflation Reduction Act (IRA) and the EU introduced the EU Critical Raw Materials Act. Both are designed to address the shortages in the EV supply chain and the forecast shortages of future supply of critical raw materials. The problem is the IRA has done little to address the supply of raw materials and the EU Critical Raw Materials Act is woefully inadequate and targets fall way short of what will be needed.

Which western graphite companies can rise to meet the challenge to establish an ex-China graphite supply chain

The leading western graphite companies that are working to establish an ex-China supply chain for flake graphite, synthetic graphite, and spherical graphite include:

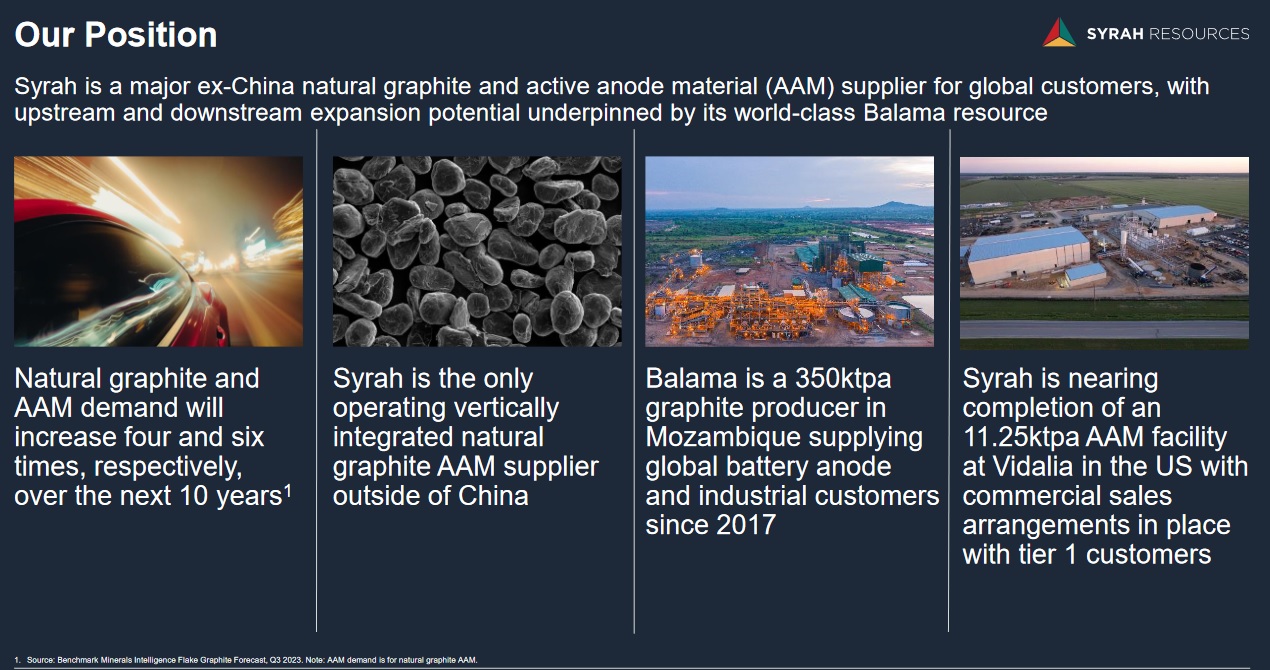

Syrah Resources Limited (ASX: SYR) – Largest western flake graphite producer with their 350,000tpa flake graphite capacity Balama Mine in Mozambique. Currently constructing the Vidalia spherical graphite facility in Louisiana, USA with Stage 1 production plans to produce 11,250tpa of spherical graphite. Longer term they plan to expand to 45,000tpa in 2026 and then to >100,000tpa by 2030 with an Europe/Middle East facility. Syrah already has an off-take agreement with Tesla (NASDAQ: TSLA). Syrah’s stock price has surged ~80% higher the past week following the release of the China export permits news.

Nouveau Monde Graphite Inc. (NYSE: NMG | TSXV: NOU) – Is rapidly progressing their plans for their Matawinie Graphite Mine and Bécancour Battery Anode Material Plant in Quebec, Canada. The company is working with Panasonic to qualify their graphite anode material. Panasonic supplies Tesla with batteries.

Northern Graphite Corporation (TSXV: NGC | OTCQB: NGPHF) – Owns graphite producing and past producing mines in Quebec, Canada and Namibia. They also own the Bissett Creek graphite Project in Ontario, Canada. The Company state that they are “North America’s Only Significant Natural Graphite Producer”. The Company plans to develop one of the world’s largest battery anode materials facilities in Baie-Comeau Québec with 200,000tpa of capacity.

NextSource Materials Inc. (TSX: NEXT | OTCQB: NSRCF) – A new graphite producer from their Molo Graphite Mine in Madagascar with Phase 1 capacity of 17,000tpa of flake graphite production and plans to expand to 150,000tpa. The Company’s short term plan is for a Battery Anode Facility in Mauritius and longer term for similar facilities in USA/Canada, UK, EU.

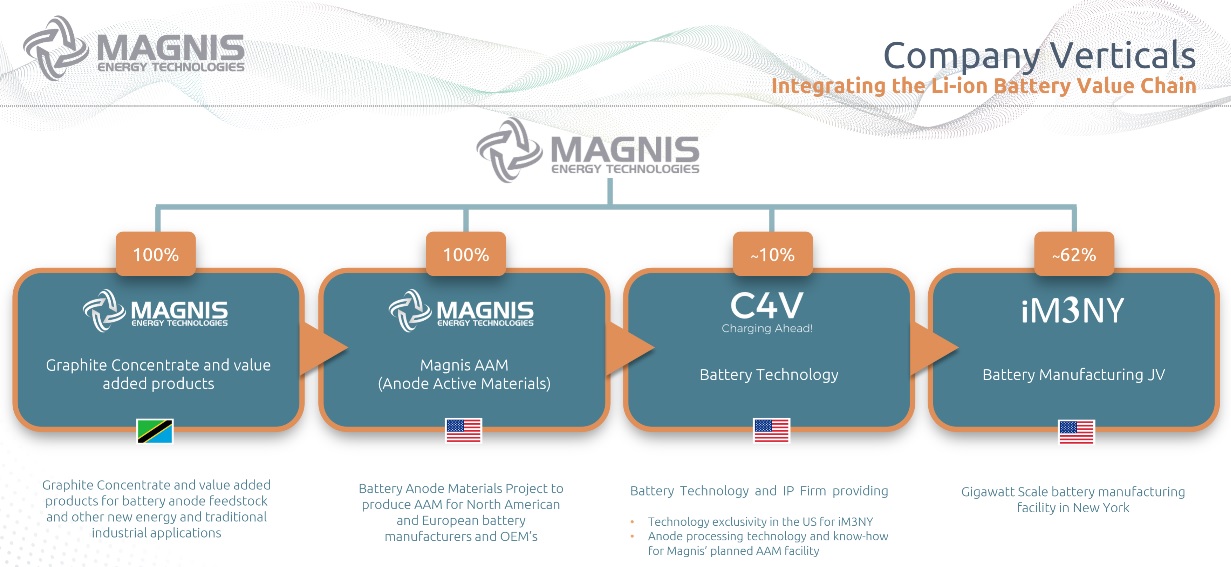

Magnis Energy Technologies Ltd. (ASX: MNS | OTCQX: MNSEF) – Magnis aims to produce high performance anode materials utilising ultra-high purity natural flake graphite from their Nachu Graphite Project in Tanzania. Magnis’ partially owned U.S.-based subsidiary Imperium3 New York, Inc (“iM3NY”) operates a gigawatt scale lithium-ion battery manufacturing project in Endicott, New York.

Talga Group Ltd. (ASX: TLG) – Own the integrated mine to anode Vittangi Graphite Project in Sweden. In September 2023 Talga broke ground on their 19,500tpa anode facility, stating “the refinery is projected to be the first commercial anode production in Europe for electric vehicle Li-ion batteries”.

Novonix Limited (NASDAQ: NVX | ASX: NVX) – Has a production capacity target of up to 20,000 tpa of synthetic graphite anode material from their Tennessee facility in the USA.

Magnis Energy Technologies is working towards becoming a graphite producer, anode materials producer and is already a small scale JV battery producer in the USA

The Western world received a loud wake-up call the past week. The China graphite products ‘export permits’ may only serve to restrict or slow down some anode material supply from China, but it puts the West on notice of how dependent they are upon China.

Given the world is rapidly moving to electric vehicles, the West must urgently build up its EV materials supply chains or risk being left behind in the global EV race.

The USA is making some bold moves and the companies discussed in this article are moving in the right direction. Let’s just hope that the western EV supply chain build out accelerates rather than stalls like GM’s latest electric pickup truck plans. I think Americans will want U.S.-branded electric cars and I know Europeans will want European branded electric cars. If we are not careful our only choice one day might be Tesla and Chinese electric cars. Stay tuned.

China’s Tightening Control over the Global Graphite Market

written by Tracy Weslosky | February 5, 2024

China’s Ministry of Commerce has announced that, effective December 1, export permits will be mandated for specific graphite products, citing national security reasons. Graphite, a pivotal component for electric vehicle (EV) batteries, finds China at its epicenter, producing 67% of the global supply of natural graphite. Additionally, China refines over 90% of the world’s graphite, which is integral to almost all EV battery anodes.

This decision unfolds in a backdrop of escalating tensions and increasing scrutiny from foreign nations. The European Union is considering tariffs on EVs originating from China, attributing unfair advantages due to state-backed subsidies. Concurrently, the U.S. has broadened its restrictions on Chinese firms accessing semiconductors and has prohibited the sale of advanced AI chips by Nvidia to Chinese companies.

The new regulatory framework targets two primary graphite types for export permits: high-purity synthetic graphite and natural flake graphite. This is reminiscent of earlier controls over “highly sensitive” graphite products, which are now integrated into the updated regulations. Analogous constraints were previously placed on semiconductor metals, gallium and germanium, which witnessed a marked reduction in exports from China.

Even though the U.S. and Europe are venturing into the graphite domain to counteract China’s monopoly, experts forecast a formidable path ahead. The central graphite importers from China currently include Japan, India, and South Korea.

These developments occur as the EV market is on an upward trajectory, with sales surging past 10 million units the previous year and predictions hovering around 14 million for the current year. This booming sector has amplified the demand for graphite, with the global market for battery use expanding by 250% since 2018. China’s contribution was a colossal 65% of the total production in the past year.

The growing EV market accentuates the criticality of raw materials like graphite. As China further consolidates its hold on the graphite industry, potential ramifications for the global EV landscape are imminent.

Right after writing this summary, I was able to reach Jack Lifton, Co-Chairman of the Critical Minerals Institute, to delve deeper into the repercussions and intricacies of these developments.

Lifton’s perspective on China’s recent announcements was direct: “This isn’t fundamentally about national security. It’s a manifestation of China’s discontent with the West’s ongoing rhetoric of reducing dependence and risks associated with their supply chain.” Lifton highlighted China’s pivotal role in graphite anode processing, suggesting that the dream of a rapid shift to EVs in the West could remain elusive without China’s involvement.

Addressing the challenges to China’s manufacturing supremacy, Lifton commented, “For years, the West prioritized cost-cutting, and China emerged as the answer. Today, the tables have turned, and the West is waking up to the consequences of its over-reliance on Chinese supply chains.”

On the topic of recent restrictions, Lifton opined, “China is fortifying its position in the critical minerals sector. The reality is that with China’s stronghold, the anticipated rapid transition of the West to EVs is looking increasingly optimistic.”

When quizzed about what minerals might be next in line, Lifton’s prediction was clear: “Post rare earths and graphite, my money would be on lithium or cobalt. The West’s ambitions for the EV transition are simply too vast for its current resources without China’s involvement.”

Lithium Ionic’s Bandeira Project: A Game Changer in the World of Critical Minerals

written by Tracy Weslosky | February 5, 2024

In a significant news this morning, Lithium Ionic Corp. (TSXV: LTH | OTCQX: LTHCF) has announced the results of its Preliminary Economic Assessment (PEA) and an updated Mineral Resource Estimate (MRE) for its Bandeira project. Located in the mineral-rich state of Minas Gerais, Brazil, this wholly-owned project stands poised to make a seismic impact in the world of critical minerals and rare earths.

The PEA Findings

The PEA, independently completed by GE21 Consultoria Mineral Ltda with support from SNC Lavalin, unveils Bandeira’s promising potential. The project could be a massive producer of low-cost spodumene concentrate, ensuring its economic viability. Some key highlights include:

A post-tax NPV8% of $1.6 billion

An internal rate of return (IRR) of 121%

A rapid payback period of just 14 months

A 20-year mine life, with an average LOM annual production of 217,700t of spodumene concentrate at 5.5% Li2O equivalent

Expanded Mineral Resources

The updated MRE is no less significant. Bandeira’s M&I resources now stand at 13.72Mt grading 1.40% Li2O, and the Inferred resources amount to 15.79Mt at 1.34% Li2O. This growth was the result of extensive drilling, marking a 196% increase in the Indicated category from the last estimate.

Company Insights

Blake Hylands, the CEO of Lithium Ionic, commented on the PEA, stating, “We congratulate our team on advancing the Project to this stage in a short time span. Our aim remains clear: becoming the next major Brazilian lithium producer.” He believes that the PEA marks a significant step toward supplying top-quality spodumene concentrate to the global lithium and electric vehicle supply chains.

Hylands also highlighted the project’s environmental conscientiousness, adding, “Commencing with a highly attractive underground project will result in significantly less surface disturbance.”

On the other hand, Helio Diniz, the President of Lithium Ionic, emphasized the company’s drive, saying, “We believe that the best approach for all of our stakeholders is to develop a significant producing operation in the shortest possible time frame.”

Bandeira Project: An Overview

The Bandeira Project encompasses 175 hectares of Lithium Ionic’s vast 14,182 hectares land package. It’s situated between Araçuaí and Itinga in Brazil’s emerging “Lithium Valley”, hinting at its strategic importance.

The engineering design for the Bandeira project envisages dual underground mining operations. The primary orebodies, which make up about 90% of the deposit, will be extracted using the “sublevel stoping” method. In contrast, the secondary southeast orebody will be mined using the “room-and-pillar” technique.

Next Steps

With the PEA out, Lithium Ionic is gearing up for the next phases of the Bandeira project. A Definitive Feasibility and Environmental Impact Assessment is anticipated by the end of 2023. The company remains optimistic about the future, hoping that the Bandeira project will set the gold standard for further expansions and serve as a catalyst for more discoveries.

Russell Fryer on Critical Metals PLC’s Strategic Moves in the DRC and Global Expansion Plans

written by InvestorNews | February 5, 2024

In a recent InvestorNews interview, host Brandon Colwell spoke with Russell Fryer, the Executive Director of Critical Metals PLC (LSE: CRTM), about the recent ‘transformational’ developments in their critical mineral operations in the Democratic Republic of the Congo (“DRC”). In addition to signing an offtake agreement for a minimum of 20,000 tons of copper oxide ore, Russell said that Critical Minerals has also secured a hydrometallurgical plant for producing a finished product.

Located less than 100 kilometers from the Molulu project, Russell said that the hydrometallurgical plant has the capacity to produce substantial amounts of copper cathode and cobalt hydroxide. With plans to grow production at the plant, Russell discusses how they are positioned to be a mid-tier player in the metals and mining industry.

Fryer emphasized that controlling downstream production and finished goods is key to competing in the global market. With the new processing capabilities, the company is well-positioned to serve the growing demand for copper cathode and cobalt hydroxide, particularly in the electric vehicle market.

Looking ahead, Critical Metals aims to expand its presence in the copper, cobalt, tantalum, tungsten, and niobium sectors. The company has been actively conducting due diligence on several mines in various countries, with the goal of operating five mines in five different jurisdictions.

Don’t miss other InvestorNews interviews. Subscribe to the InvestorNews YouTube channel by clicking here

About Critical Metals PLC

Critical Metals PLC has acquired a controlling 100% stake in Madini Occidental Limited, which holds an indirect 70% interest in the Molulu copper/cobalt project, a producing asset in the Katangan Copperbelt in the Democratic Republic of Congo.

The Company will continue to identify future assets that are in line with its stated acquisition objective of low CAPEX and OPEX brown-field projects with near-term production and cash-flow, whilst concentrating on minerals that have strategic importance to future economic growth thereby generating significant value for shareholders.

To know more about Critical Metals Plc, click here

Disclaimer:Critical Metals Plc is an advertorial member of InvestorNews Inc.

This interview, which was produced by InvestorNews Inc. (“InvestorNews”), does not contain, nor does it purport to contain, a summary of all material information concerning the Company, including important disclosure and risk factors associated with the Company, its business and an investment in its securities. InvestorNews offers no representations or warranties that any of the information contained in this interview is accurate or complete.

This interview and any transcriptions or reproductions thereof (collectively, this “presentation”) does not constitute, or form part of, any offer or invitation to sell or issue, or any solicitation of any offer to subscribe for or purchase any securities in the Company. The information in this presentation is provided for informational purposes only and may be subject to updating, completion or revision, and except as may be required by applicable securities laws, the Company disclaims any intent or obligation to update any information herein. This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein.

Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. This presentation should not be considered as the giving of investment advice by the Company or any of its directors, officers, agents, employees or advisors. Each person to whom this presentation is made available must make its own independent assessment of the Company after making such investigations and taking such advice as may be deemed necessary. Prospective investors are urged to review the Company’s profile on SedarPlus.ca and to carry out independent investigations in order to determine their interest in investing in the Company.

Defense Metals’ Wicheeda Project: A Future Powerhouse in Rare Earth Production

written by InvestorNews | February 5, 2024

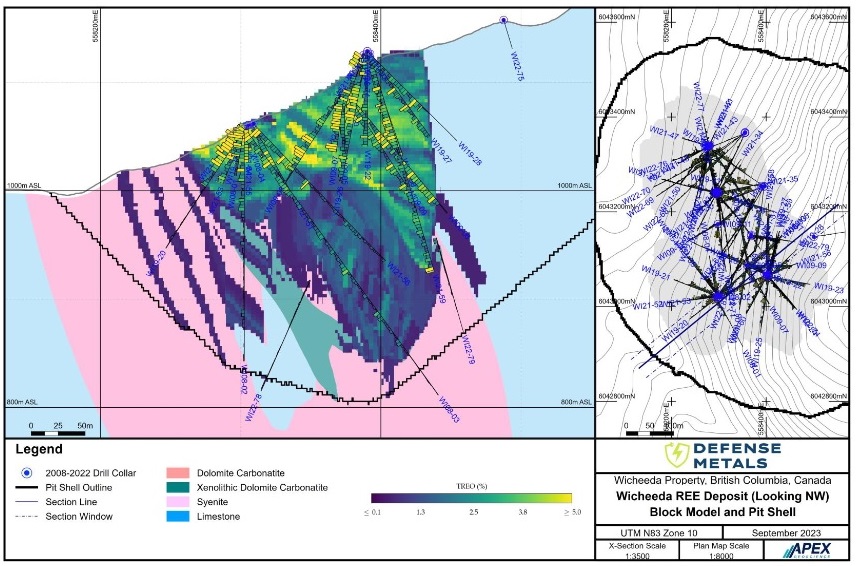

Defense Metals Corp. (TSXV: DEFN | OTCQB: DFMTF), known as ‘Defense Metals’, fully owns the Wicheeda Rare Earth Element Project, situated 80 km northeast of Prince George in British Columbia, Canada. This project is not only strategic but could emerge as a globally recognized hub for the production of critical magnet rare earths, specifically neodymium (Nd), praseodymium (Pd), cerium (Ce), and lanthanum (La). To put this into perspective, Defense Metals envisions that the Wicheeda Project might churn out 25,000tpa of REO, potentially accounting for roughly 10% of the world’s current output.

Recent Enhancements in the Wicheeda Resource Estimate

Come September 12, 2023, Defense Metals announced a significant expansion of the Wicheeda resource: a growth of 31% in tonnage and 17% in contained metal since the 2021 estimate. Moreover, the Total Measured and Indicated (M+I) Mineral Resources now touch a whopping 34.2 million tonnes with an average of 2.02% TREO.

Thanks to its geological structure, the Wicheeda Project is primed for a straightforward open-pit operation, accompanied by parasite/bastnaesite/monazite metallurgy, simplifying the processing phase.

Schematic showing the Wicheeda deposit and open pit block model(noting higher grades near surface)

Just a week earlier, on September 5, Defense Metals unveiled new exploration targets within the Wicheeda REE Deposit. They identified two previously undetected linear radiometric anomalies, each approximately 40 meters wide and extending around 250 meters northwest from the core Wicheeda REE deposit. Defense Metals’ Director, Kristopher Raffle, P.Geo., remarked, “After a thorough review of the geophysical data juxtaposed with our revamped Wicheeda 3D geological model, the potential for undiscovered carbonatite bodies came to light. We’re keen on drill testing these anomalies.”

Further enhancing its value proposition, the Wicheeda Project boasts easy road accessibility and is close to a major deep-sea port, power transmission lines, a gas conduit, and a critical rail line.

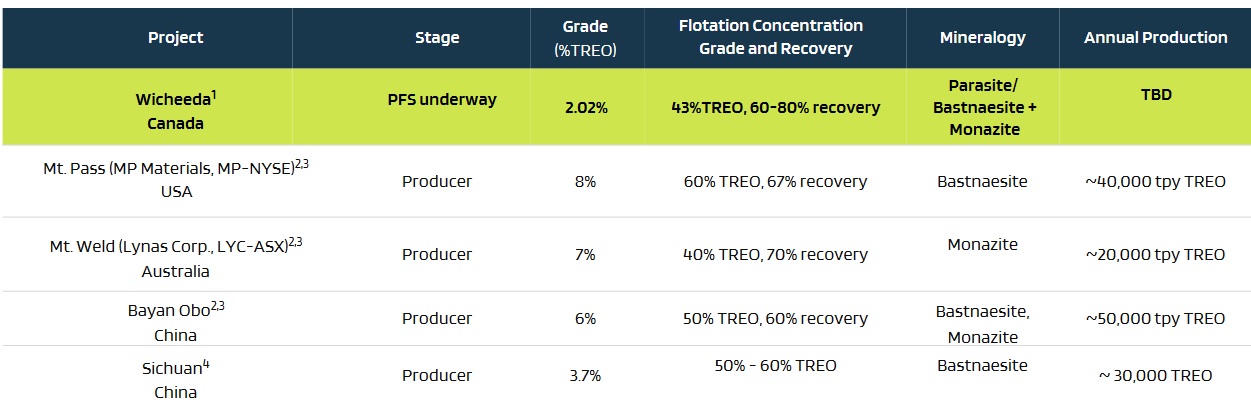

When stacked against leading rare earth producers, while the Wicheeda Project may have a lower grade, it’s planning to roll out large-scale production – all in the secure environment of Canada.

Wicheeda Project in comparison to leading rare earths producers

Upcoming on Defense Metals’ agenda is the Preliminary Feasibility Study (PFS) set for H1 2024, followed by a comprehensive Feasibility Study (FS) in the latter half of the year. By 2025, their focus will shift towards optimizing and ramping up flotation and hydromet pilot plants.

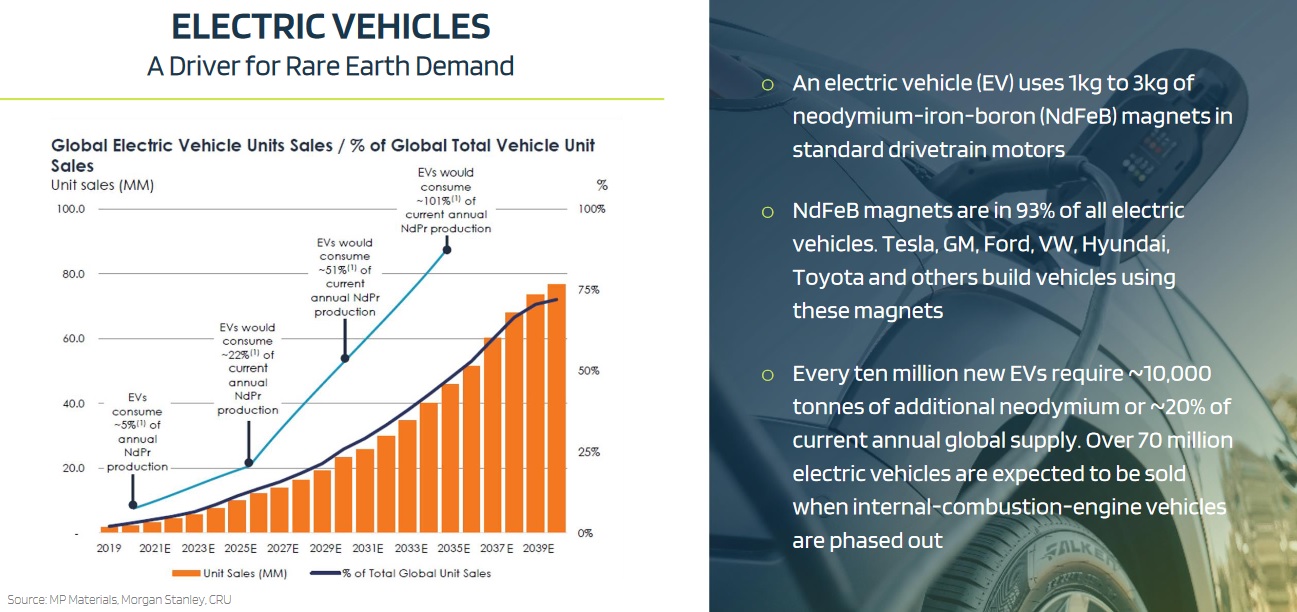

Electric car sales are forecast to surge in the years ahead requiring ever increasing amounts of magnet rare earths

The appetite for NdPr, key magnet metals, has been on a steady incline, further fueled by the escalating demand for top-tier permanent magnet motors employed in electric vehicles and wind turbines.

Transitioning smoothly from exploration to development, Defense Metals’ Wicheeda Project stands out with its rich NdPr resource. Stakeholders and potential investors are keenly looking forward to the H1 2024 PFS for an in-depth look at the project’s financial prospects.

Currently, Defense Metals Corp. has a market capitalization of C$50 million. This is definitely a venture to closely monitor in 2024.

Lithium Ionic Charges Forward with a Growing Portfolio of Lithium Deposits in Brazil

written by InvestorNews | February 5, 2024

InvestorNews discussed Lithium Ionic Corp. (TSXV: LTH | OTCQB: LTHCF) in June 2023 in an article here, where we looked at who might potentially be the next successful lithium company in Brazil. Since then the stock has moved sideways, in part due to falling lithium prices and sentiment, yet the good news keeps coming from Lithium Ionic. The Company continues to advance at ‘warp speed’ with a Maiden Resource totaling ~19.43 MT at ~1.40% Li2O already declared in June 2023, a PEA due out in Q3, 2023, and a DFS by the end of 2023. Added to this will be more drill results and Environmental Impact Assessment (“EIA”) studies expected to be completed within H2 2023. Wow!

Lithium Ionic owns two exciting lithium projects – The Itinga and Salinas lithium projects, spread over 14,182 hectares in the northeastern part of Minas Gerais, Brazil.

Lithium Ionic Corp. company highlights includes their Itinga and Salinas lithium projects in Brazil

The good news keeps coming as Lithium Ionic hits the accelerator at their Itinga Lithium Project in Brazil

On June 27, 2023, Lithium Ionic announced their Maiden 43-101 compliant mineral resource estimate at their Itinga Lithium Project (Bandeira and Outro Lado (Galvani) deposits). The Measured and Indicated (“M&I”) Resource was 7.57 million tonnes (“Mt”) grading 1.40%Li2O and the Inferred Resource was 11.86 Mt grading 1.44% Li2O. If adding the two together we get to a total resource of ~19.43 MT, a very impressive start for the Company.

Following the Maiden Resource Lithium Ionic immediately expanded their drill campaign to 13 drill rigs (50,000 metres in total planned). Work is underway on their PEA which is due for release in Q3, 2023 and a DFS targeted for completion by the end of 2023. That is lightning speed and really only possible in places such as Brazil where new projects are being accelerated.

Lithium Ionic CEO Blake Hylands commented at the time:

“I commend our excellent team in Brazil for the speed at which these pegmatites have been delineated; the past year has been an impressive demonstration of how quickly these deposits can be defined and expanded.……Our execution strategy is to advance Bandeira and Outro Lado through engineering and permitting as quickly as possible, while expanding and upgrading resources at these, and our various other prospective targets in this belt. We look forward to delivering resource updates later this year in parallel with the planned PEA in Q3 and Feasibility Study by year-end.”

On July 19, 2023, Lithium Ionic announced: “Lithium Ionic signs MOU with local government authority Invest Minas; obtains priority statusto facilitate acceleration of licensing and development for its Itinga and Salinas lithium projects, Brazil.”

Note: Bold emphasis by the author.

Again we see the word ‘accelerate’. Lithium Ionic is in a hurry, which is usually great news for investors if good results continue.

Highlights of Lithium Ionic’s MOU with the local government authority Invest Minas

On July 20 Lithium Ionic announced further strong drill results including 1.89% Li2O over 10.2m and 1.92% Li2O over 6.4m at the Bandeira deposit within the Itinga Lithium Project. The chart below gives a nice summary of recent drill results.

Best recent drill results at the Bandeira and Outro Lado deposits within the Itinga Lithium Projects

Solid early stage drill results from Salinas Project

As announced on July 25 Lithium Ionic drill results at their Salinas Project included 1.38% Li2O over 16m from 40.4mdepth, 1.60% Li2O over 12mfrom 68.2m, 1.55% Li2O over 9m from 129m, 1.26% Li2O over 11m from 63m, and 1.34% Li2O over 10m from 94m. These are solid results with very good grades, albeit shorter lengths. CEO Blake Hylands stated:

“The initial results from Salinas confirm continuity of lithium mineralization with good grades and widths between the wide spaced drill holes completed in 2022 by the previous owner. These results, along with the significant growth seen at the Colina deposit only 500 metres west of our drilling site, as well as numerous historical artisanal workings that span decades of activity to the east, provide a strong indication of the potential for Salinas to quickly develop into an important part of our growing portfolio of lithium deposits.”

Closing remarks

Lithium Ionic continues to move at warp speed and deliver excellent results, especially at their Itinga Project located very close (<4kms) to Sigma Lithium’s huge Grota do Cirilo Mine and Resource (85.6Mt @ 1.44% Li2O). Lithium Ionic’s Salinas Project is also showing some positive early signs. It sits adjacent to Latin Resources’ Colina Project (45.2Mt @1.34% Li2O). These two other projects (Grota do Cirilo & Colina) very near Lithium Ionic’s projects are the two largest lithium projects in Brazil.

Lithium Ionic’s recent sideways stock price movement is more a reflection of the current market dynamics than the Company’s recent results. Best not to wait too long to discover Lithium Ionic as we saw with past Brazil stars Sigma Lithium Corporation (NASDAQ: SGML | TSXV: SGML) and Latin Resources Limited (ASX: LRS).

H2, 2023 is stacked full of catalysts for this very exciting company which is well funded after a recent raise of ~C$28 million in July 2023.

Lithium Ionic Corp. trades on a market cap of C$331 million.

Automotive’s Existential Challenge – Supply Chain Awareness for EV Production

written by Jack Lifton | February 5, 2024

It has become necessary today for the OEM automotive assemblers to assert varying degrees of control over the component companies in the total supply chain for electric vehicle (“EV”) storage batteries and, also, for rare earth permanent magnet motors, not only for those used in powering onboard accessories but also for the vehicle drive trains.

The automotive industry faces a new supply chain issue

Up until now OEM automotive relied on a tiered supplier system. For the supply of outsourced production parts (those that are actually on the finished car as delivered to the customer) the OEMs bought from prior approved, by them individually, Tier One vendors of the part. In turn, these Tier Ones were responsible for the selection of qualifiable (to the OEM) vendors to themselves, these would be the Tier Twos. The daisy chain continued until the anchor of the supply chain, the mine and/or the mineral processor was reached far, far away from the concern, or understanding, of the OEM automotive assembler’s procurement operations.

The reliance on the daisy chain of tiered responsibility has been upended by the need for the fine chemicals required to manufacture lithium-ion storage batteries and rare earth permanent magnet motors.

Those total supply chains with enough capacity to supply an OEM automotive assembler exist today only in China, which has been constructing those supply chains for at least 15 years.

Lack of understanding of key players in the supply chain

American (and European and non-Chinese Asian with the possible exception only of Japan) do not understand these supply chains well enough, much less the detail of their individual component companies, to identify the key players, much less to manage them from the standpoint of strict adherence to specifications, quality control, on-time delivery, and guaranteed pricing, the main pillars of OEM automotive procurement.

OEM automotive has thus embarked on what I like to call, The-Streetcar-named-Desire system of procurement selection, the industry depends on the kindness of strangers. The main barrier to success in such a system is the absence of experience among the procurement groups of almost any knowledge of the principal industries, mining, chemical engineering, and technology metal-enabled component manufacturing that need to be reconfigured to meet the rigid standards for qualification among the OEM automotive assemble industry.

Experience currently not driving government and business decisions

Just as an example of the pervasiveness in America of this dilemma, I asked the U.S. Dept of Defense why they chose the American rare earth mining company, MP Materials Corp. (NYSE: MP), and the Australian rare earth miner, initial processor, Lynas Rare Earths Ltd. (ASX: LYC) to develop separation systems for “heavy” rare earths, when neither company had ever done such development work. The answer was “Both had large market capitalization, revenues, and significant retained earnings.” So, I guess, it will have been the “bean counters” who killed the program, not those who sought prior experience and proven capability among vendors.

The OEM automotive industry has embarked on an existential challenge, the total replacement of a well-understood technology, ICE drive trains, with a long-established and proven total supply chain, with a supply chain, that for storage batteries and rare earth permanent magnet drive motors with which they have no experience at all.

What is needed

The mining, refining, and fabrication of industrial precursor forms of the technology metals for the OEM automotive industry are not well developed outside of China.

The survival of the non-Chinese OEM EV automotive industry will depend on selecting the component vendors in the distinctly different total supply chains for lithium and rare earths. Sadly, this cannot be left to the battery and motor vendors, who mostly do not have the political and financial resources to address the problems involved.

Final thoughts

The key problem to be faced is finding the necessary experienced expert total supply chain advisors.