Technology Metals Report (03.08.2024): Chinese Investment in Asia rose 37% in 2023, and the BYD Push in Australia is Underway

Welcome to the latest Technology Metals Report (TMR) where we highlight the top news stories that members of the Critical Minerals Institute (CMI) have forwarded to us in the last week. Key highlights in this Technology Metals Report include the announcement of Australia and Vietnam upgrading their relations to begin talks on critical minerals, focusing on diversifying supply chains away from China. This significant move aims to enhance cooperation in several sectors, particularly in the energy and resources sector, emphasizing the critical minerals supply chain. Both countries, known for their substantial roles in the production and reserves of critical minerals, are looking to strengthen their global supply chain positions amid rising geopolitical tensions and efforts to reduce dependency on China. Additionally, this edition features updates on Chinese investments in Asia, notably in Indonesia, which have surged by 37% in 2023 despite global economic challenges. This growth, largely concentrated in Belt and Road Initiative (BRI) countries, underscores China’s strategic shift towards green energy and mining investments, especially in Southeast Asia.

Moreover, this edition of the TMR delves into several crucial developments in the critical minerals and technology metals landscape. The United States outlined its critical minerals strategy for the clean energy transition, emphasizing the need to secure and diversify supply chains for essential minerals such as nickel, manganese, cobalt, and lithium. The EU’s move to register Chinese electric vehicle (EV) imports for potential retroactive tariffs reflects growing concerns over fair trade practices. Kazakhstan’s emergence as a potential major supplier of lithium, along with investments aimed at expanding lithium operations by companies like Albemarle, highlights the global race to secure essential components for green and digital technologies. Furthermore, the report covers strategic shifts in the supply chain, such as Posco’s agreement with Syrah Resources for graphite supply from Mozambique and Toyota’s multi-pathway approach to CO2 emissions reduction. These stories collectively point to a dynamic and rapidly evolving global landscape for critical minerals and technology metals, underlining the strategic importance of diversification, cooperation, and sustainable development in securing the materials essential for the future of technology and clean energy.

Australia and Vietnam upgrade relations, to begin talks on critical minerals (March 7, 2024, Source) — Australia and Vietnam have elevated their relations to a comprehensive strategic partnership, announced by Australian Prime Minister Anthony Albanese. This upgrade includes an annual dialogue on minerals, focusing on diversifying supply chains away from China. The partnership aims to enhance cooperation on climate, environment and energy, defense and security, and economic engagement and education. Additionally, it will foster collaboration in the energy and resources sectors, especially in critical minerals supply chains. Both countries, significant in the production and reserves of critical minerals, seek to strengthen their positions in global supply chains amid rising tensions and efforts to reduce dependency on China. This move also signifies Vietnam’s success in “bamboo diplomacy,” enhancing its relations with major global powers. The partnership reflects a deep mutual political trust and commits to expanded cooperation across various sectors, marking a milestone in the bilateral relationship between Australia and Vietnam.

Chinese investment in Asia rose 37% in 2023, led by Indonesia (March 7, 2024, Source) — In 2023, Chinese investment in the Asia-Pacific region surged by 37% to nearly $20 billion, outperforming global trends amid economic challenges. Construction contracts also grew by 14% to about $17 billion, supported by Chinese loans. This contrasts with a 12% decrease in foreign direct investment into Asia’s emerging economies. The investment was predominantly in Belt and Road Initiative (BRI) countries, focusing on infrastructure that connects Asia to Europe. Non-BRI country investment plummeted by 90% to a mere $120 million. Notably, investment strategies shifted towards green energy and mining, with 50% of China’s regional investment directed towards Southeast Asia, and Indonesia receiving the largest share at $7.3 billion. However, certain countries like the Philippines and Pakistan saw significant drops in Chinese engagement due to political and economic risks. The report anticipates a further increase in Chinese investment and construction, especially in green transition initiatives and strategic infrastructure projects, despite China’s own economic challenges.

Under Secretary Jose Fernandez Discusses U.S. Critical Minerals Strategy for Clean Energy Transition (March 6, 2024, Source) — Under Secretary Jose W. Fernandez discussed the U.S.’s strategy for securing and diversifying the supply chain of critical minerals crucial for the clean energy transition in a conversation with InvestorNews’ Tracy Weslosky. Highlighting minerals like nickel, manganese, cobalt, and lithium, Fernandez underscored efforts to expand their supply and engage with countries possessing these resources through concrete projects, investment, and financing. He emphasized the challenge of reducing dependency on China, which currently controls a significant share of these minerals, pointing out the strategic vulnerability this poses. Fernandez stressed the importance of adhering to values such as environmental respect, community collaboration, and transparency in these endeavors. Despite slow progress, the U.S. aims to not only secure but also ethically source these minerals to support the global shift towards clean energy.

EU set to allow possible retroactive tariffs for Chinese EVs (March 6, 2024, Source) — The European Commission will start registering Chinese electric vehicle (EV) imports for potential retroactive tariffs, in response to an anti-subsidy investigation. This investigation aims to determine if Chinese EVs benefit from unfair subsidies, potentially harming EU producers. If found guilty, tariffs could be imposed, with provisional duties possible by July and a final decision expected by November. The Commission has found preliminary evidence of subsidy and a significant 14% year-on-year increase in imports since the investigation began in October, suggesting potential harm to EU producers. The China Chamber of Commerce expressed disappointment, attributing the import surge to growing European demand for EVs.

Kazakhstan positions itself for lithium windfall (March 6, 2024, Source) — Kazakhstan is emerging as a significant potential supplier of lithium, crucial for power-storage technology, with reserves estimated at around 75,600 tons. Research by the Korea Institute of Geoscience and Mineral Resources highlighted substantial reserves in eastern Kazakhstan, potentially worth up to $15.7 billion. This discovery, along with European interest in Kazakhstan’s critical raw materials, underscores the country’s growing importance in the global lithium market. The European Commission and European Bank for Reconstruction and Development have allocated funds for lithium exploration, highlighting the strategic value of Kazakhstan’s resources amidst increasing global demand. With investments from various countries, including China and potentially European entities, Kazakhstan is set to play a crucial role in the lithium supply chain, essential for green and digital technologies.

BYD spearheads Chinese electric car push in Australia, a friendlier market (March 5, 2024, Source) — BYD and other Chinese automakers are making significant inroads into the Australian electric vehicle (EV) market, leveraging the friendly trade environment and benefiting from the government’s aggressive EV adoption policies under Prime Minister Anthony Albanese since 2022. With no trade barriers, EV subsidies, and tax benefits, EV sales in Australia have soared, with EVs making up 7.2% of new car sales in 2023. BYD, supported by Warren Buffett, has quickly captured 14% of Australia’s EV market since its entry in 2022, trailing only behind Tesla. The company plans to expand its product lineup and dealership network in Australia, aiming for mainstream market penetration. Similarly, SAIC Motor under its MG brand is set to launch new models. Incumbent automakers like Ford and Toyota are also adapting, introducing electrified vehicles to compete. Despite being a relatively small market, Australia’s lack of local car manufacturing and openness to international trade make it an attractive destination for Chinese EV manufacturers, especially given the geopolitical tensions in other key markets.

Canada and Australia boost collaboration on critical minerals (March 4, 2024, Source) — Canada and Australia have committed to enhancing their cooperation on critical minerals, vital for battery production and clean energy transition, according to a joint statement released on the margins of the PDAC conference in Toronto. Both countries, rich in these essential minerals, aim to bolster their partnership through R&D collaboration, trade, and investment in the mining sector based on a non-legally binding agreement. This collaboration seeks to ensure supply chain transparency and promote high Environmental, Social, and Governance (ESG) standards globally. The initiative will be spearheaded by Canada’s Natural Resources Ministry and Australia’s Critical Minerals Office, focusing on policy and investment coordination to support the burgeoning demand for these minerals in the upcoming decades.

Albemarle (ALB) Accelerates Lithium Growth With $1.75B Offering (March 4, 2024, Source) — Albemarle Corporation (NYSE: ALB) announced a $1.75 billion offering in depositary shares, each representing a 1/20th interest in Series A Mandatory Convertible Preferred Stock, with a potential additional offering of $262.5 million under certain conditions. The proceeds are intended for general corporate uses, notably to fund growth capital expenditures for expanding lithium operations in Australia and China, as well as repaying outstanding commercial paper. The depositary shares will carry rights and preferences similar to the Preferred Stock, including conversion into common stock on or around March 1, 2027. Despite a 52.1% decrease in Albemarle’s share price over the past year, the company forecasts a 10-20% increase in Energy Storage volumes for 2024, with expected net sales in its Specialties and Ketjen segments ranging from $1.3 to $1.5 billion and $1 to $1.2 billion, respectively.

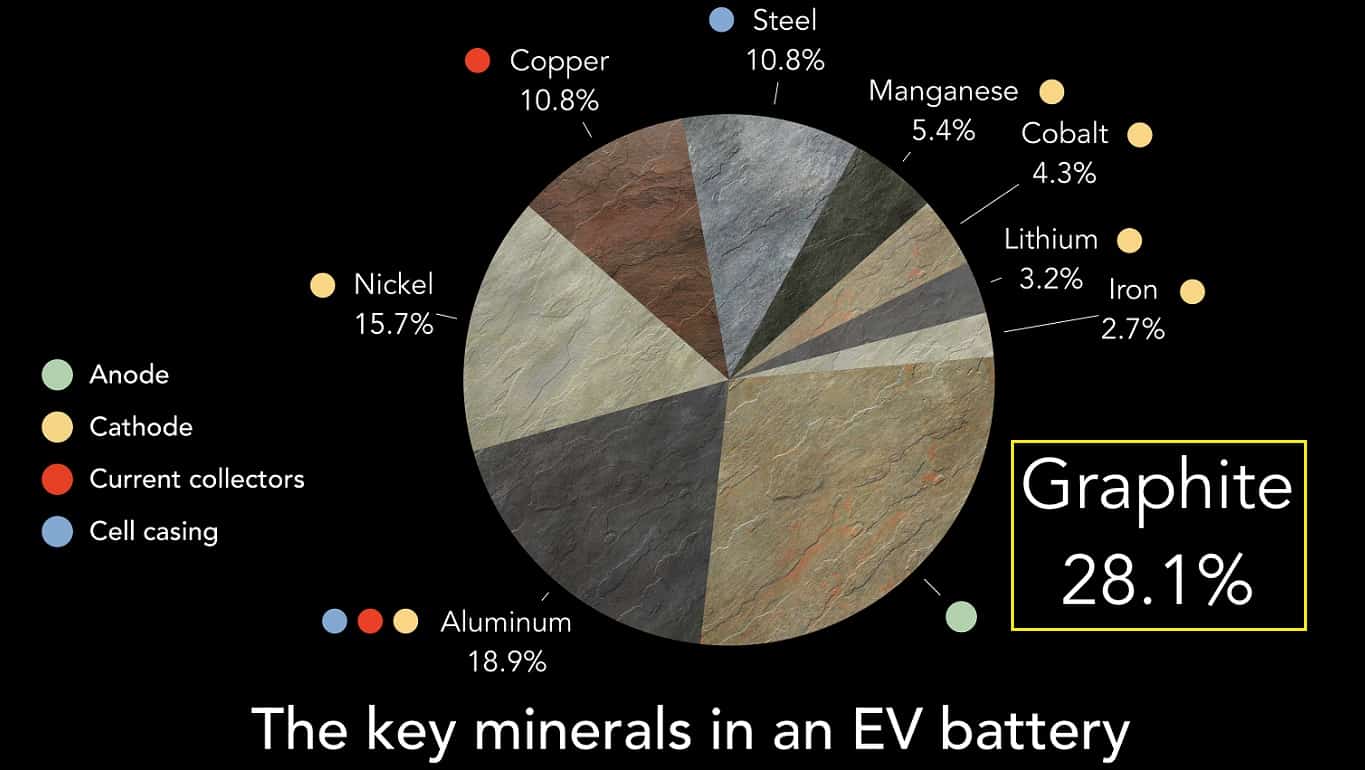

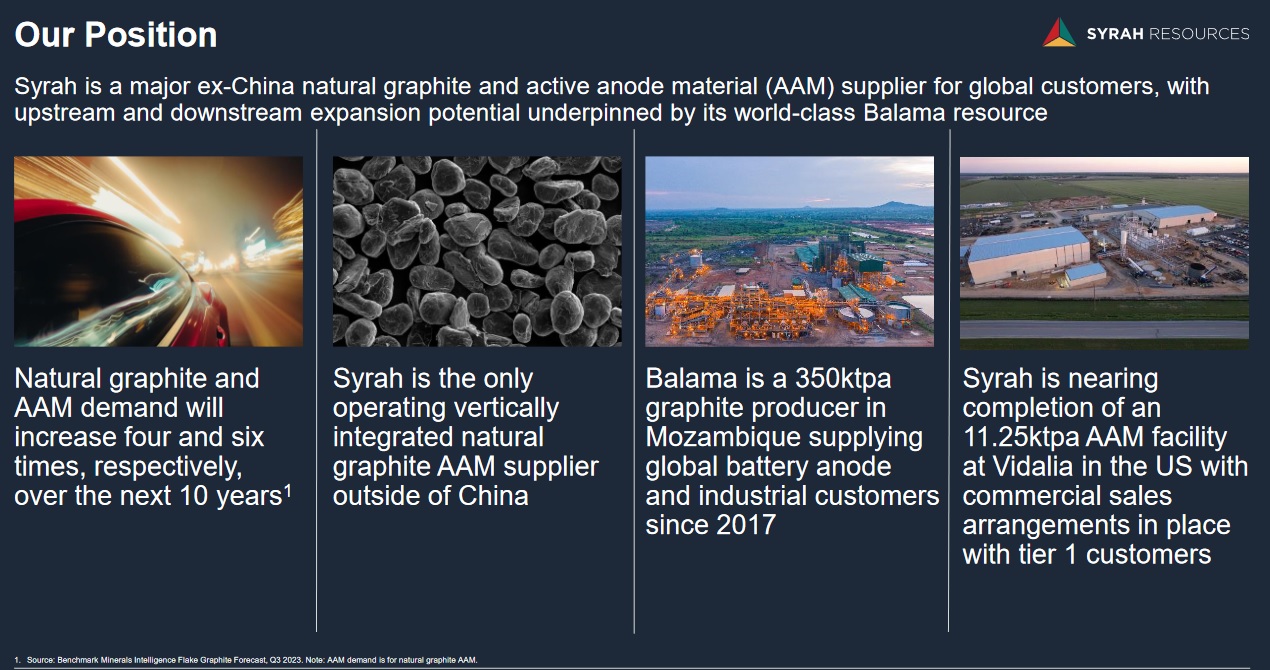

Posco to source 60,000 tons of graphite from Africa in pull away from China (March 3, 2024, Source) — Posco Future M, a subsidiary of Posco Group, is shifting its supply chain for natural graphite, a crucial battery material, away from China towards Africa. This move is highlighted by a new deal with Australian mining firm Syrah Resources Limited (ASX: SYR), which will provide Posco Future M with up to 60,000 tons of natural graphite annually for six years from its Mozambique Balama operation, starting no later than 2025. This supply is expected to cover 40% of Posco Future M’s anode production, translating to about 30,000 tons of anodes. The agreement comes amid concerns over China’s control over graphite exports, potentially as leverage against international policies such as the U.S.’s Inflation Reduction Act. Posco’s decision reflects a broader strategy to diversify supply sources and reduce dependency on China, amid rising geopolitical tensions and supply chain vulnerabilities.

Total EV Adoption Is Not The Way Forward, Says Toyota Chairman (March 3, 2024, Source) — Akio Toyoda, Toyota’s Chairman, expresses skepticism towards full adoption of battery electric vehicles (BEVs), arguing they will not dominate the market beyond a 30% share despite other markets already exceeding this percentage. In a presentation in Tokyo, he emphasized a multi-pathway approach to combating CO2 emissions, suggesting that consumer choice should drive the future of automotive powertrains rather than regulations. Toyota plans to focus on a diverse range of technologies including internal combustion engines, hybrids, and hydrogen vehicles, alongside BEVs. Despite the global push towards electric vehicles, with countries like Norway showing an 80% market share for EVs, Toyoda’s stance reflects a broader strategy to embrace multiple solutions for emission reduction. This perspective aligns with Toyota’s goal to comply with future regulations and its commitment to sell 1.5 million EVs by 2026, while also investing in alternative technologies like e-fuels.

Kazakhstan plans to export aluminum, gallium and scandium to the US (March 1, 2024, Source) — Kazakhstan is aiming to strengthen its trade ties with the United States by proposing to export aluminum, gallium, and scandium. This initiative was unveiled during Minister of Industry and Construction Kanat Sharlapayev’s official visit to the U.S., focusing on promoting Kazakhstani interests globally and expanding cooperation in critical materials. In addition to these exports, Kazakhstan is offering tolling services and exploring the production of other precious minerals like wolfram, cobalt, lithium, and titan, aiming to discuss long-term contracts and investment support. The country, which processes 17 of the 50 minerals critical to the U.S. economy, already exports several strategic minerals to American companies. Sharlapayev’s visit also involved meetings with leading American companies to discuss opportunities in industrial production and geological exploration. The talks highlighted the potential for joint projects in various sectors, including infrastructure development and technology, with the U.S. International Development Finance Corporation expressing interest in deepening cooperation with Kazakhstan.

Chinese money still chasing Canadian critical mining deals despite Ottawa’s scrutiny (February 27, 2024, Source) — A year after Canada tightened its foreign investment rules for the critical minerals sector to enhance national security, Chinese investments continue to flow into Toronto-listed mining companies, as per research by the University of Alberta. Despite Canada forcing three Chinese investors to divest their stakes in 2022 and increasing scrutiny on foreign deals, especially in critical minerals, investments from China and Hong Kong surged to C$2.2 billion in 2023, a significant leap from C$62 million in 2022. This influx is buoyed by the perception that Canada remains open to Chinese investments, with junior miners finding it easier to secure funding. The critical minerals sector, vital for Canada’s national security, has seen Chinese entities actively investing, notably in copper assets. For instance, MMG Africa Ventures acquired a copper mine for C$1.7 billion, and Jiangxi Copper Co increased its stake in First Quantum Minerals Ltd. (TSX: FM). Some Canadian miners are lobbying for more Chinese investments due to difficulties in raising capital elsewhere, despite the government’s stringent stance on safeguarding critical resources.

Investor.News Critical Minerals Videos:

- March 08, 2024 – Mark Chalmers on Energy Fuels as a Profitable Uranium Producer in the U.S. https://bit.ly/3P9nl1J

- March 07, 2024 – Critical Metals Russell Fryer on Copper and Cobalt Plans for Production in 2024 https://bit.ly/43bGYvJ

- March 06, 2024 – Under Secretary Jose Fernandez Discusses U.S. Critical Minerals Strategy for Clean Energy Transition https://bit.ly/433yBSZ

Critical Minerals IN8.Pro Member News Releases:

- March 8, 2024 – F3 and Traction Begin Drilling to Locate Source of Radioactive Boulders https://bit.ly/436k09t

- March 7, 2024 – American Clean Resources Group Commits to Transfer Federal Tax Credits to Investors to Accelerate the Development of Its Renewable Energy Assets https://bit.ly/3wCIjzu

- March 6, 2024 – Halleck Creek Project Update https://bit.ly/3InYYJV

- March 6, 2024 – Karbon-X Announces Appointment of Brett Hull and Justin Bourque to its Board of Directors https://bit.ly/3TpdYxt

- March 5, 2024 – Panther Metals PLC – Australia: Coglia Nickel-Cobalt Mineral Resource Exceeds 100Mt https://bit.ly/3IptcMI

- March 5, 2024 – Panther Metals PLC – Obonga: Extension of Purchase Agreement https://bit.ly/3TmYLge

- March 4, 2024 – Ucore Progresses Through Heavy Rare Earth Processing as It Completes Second Milestone of Strategic US DoD Contract https://bit.ly/3uSunkx

- March 4, 2024 – First Phosphate Corp. Receives Mining Research and Innovation Grant from Quebec Ministry of Natural Resources https://bit.ly/3Iny84z

- March 4, 2024 – Voyageur Pharmaceuticals and API Forge Alliance for Carbon-Based Imaging Drug Advancement https://bit.ly/3wBuem6

- March 4, 2024 – Defense Metals Ships Mixed Rare Earth Carbonate Samples to two major REE companies https://bit.ly/43iwmLT

- March 4, 2024 – Power Nickel Defines Initial Volume on its High-Grade Cu-Pt-Pd-Au-Ag Zone 5km Northeast of its Main Nisk Deposit https://bit.ly/3TiZNde

{kind=link}

{kind=link}