BYD and Tesla are totally dominating global electric car sales in 2023

Many people would probably be surprised to hear how poorly legacy car manufacturers are doing in terms of electric car sales. They would also be shocked how just two companies are totally dominating global plugin electric car sales. Those two companies are BYD Co. Ltd. (OTC: BYDDF) and Tesla Inc. (NASDAQ: TSLA).

BYD dominates total sales with about half coming from pure electric cars and about half from plugin hybrids. Tesla dominates in terms of total revenues as well as profit per vehicle.

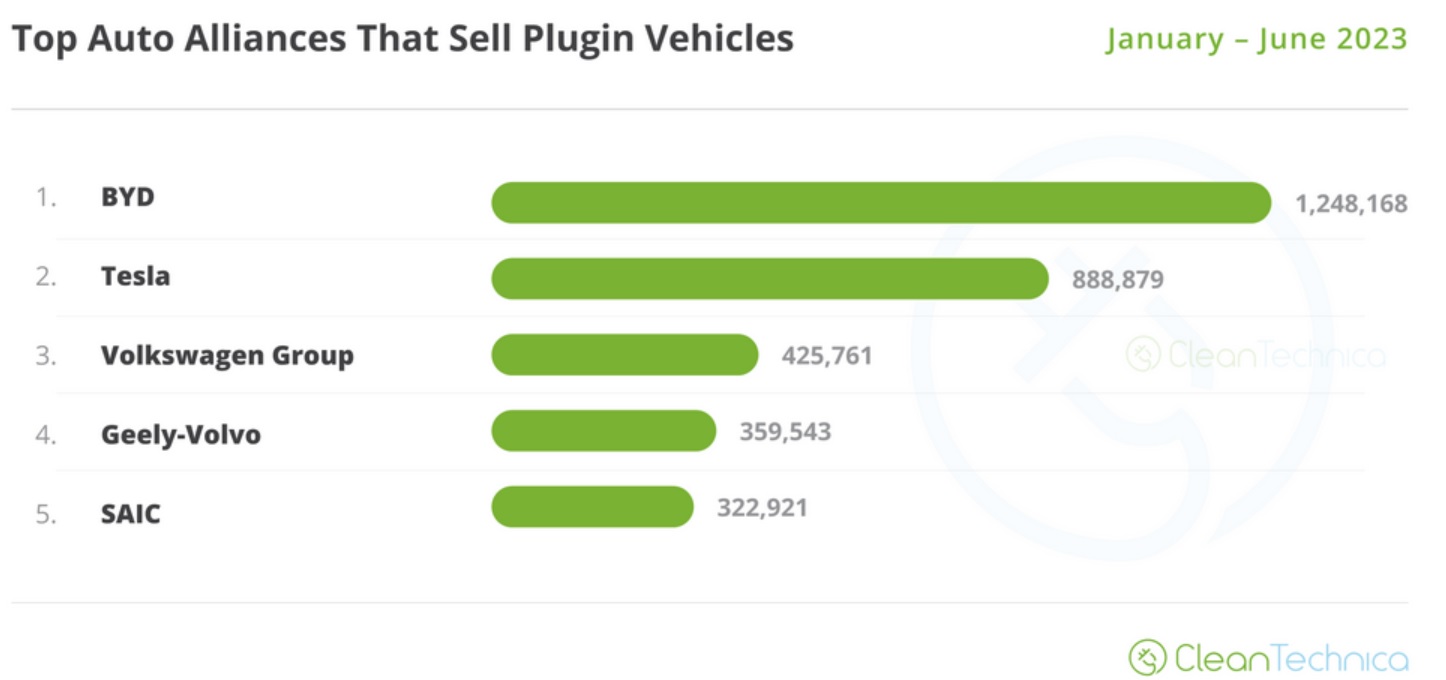

The chart below shows H1, 2023 global plugin electric car sales with BYD leading on 1,248,168 sales and Tesla on 888,879 sales.

The next closest is the Volkswagen Group with 425,761 sales, roughly a third of BYD and half of Tesla.

Top selling global plugin electric car auto groups Jan-June, 2023

Tesla and BYD’s lead looks set to continue in 2023, currently with a combined 36.6% of the market

Tesla and BYD have been expanding their manufacturing facilities at a feverish pace for the past several years and the results are now showing. Furthermore, by the end of 2023, their lead will be even bigger, in raw number terms. Tesla targets 1.8 million sales and BYD a massive 3 million sales in 2023.

Results like this are leaving internal combustion energy (“ICE”) legacy auto companies at risk of becoming extinct this decade as the world transitions rapidly towards EVs. For example, Toyota only sold 46,171 pure battery electric vehicles globally in H1, 2023.

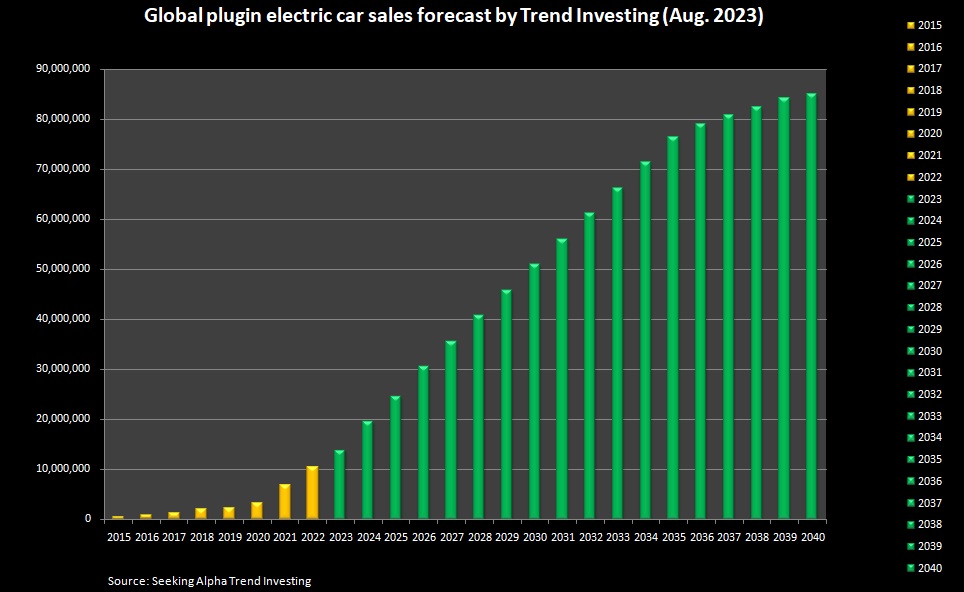

As shown on the chart below we are still in the early stages of the EV boom with sales forecast to increase exponentially over the next 10-15 years. Given the current dominance of BYD and Tesla, it is looking like they will get a major part of these future sales.

BYD is currently ranked number 1 globally with 21.4% market share YTD (Jan-June 2023).

Tesla is currently ranked number 2 globally with 15.2% global market YTD (Jan-June 2023).

Combined BYD and Tesla currently have 36.6% of the global plugin electric car market.

Global plugin electric car sales forecast to 2040 (green bars)

BYD sales continue to boom with 261,105 sold in July and 274,086 electric cars sold in August 2023. Tesla’s sales will be released at the end of Q3.

Takeaway for investors

BYD and Tesla are dominating global sales. They are really the only two companies selling electric cars at a profit and it shows with their tremendous growth in profits in recent years.

As reported on August 29, 2023, BYD posted a >200% surge in first half profit, with net profit in the first six months rising 204.68% to 10.95 billion yuan (US$1.50 billion), as compared to 3.6 billion yuan a year earlier.

Tesla’s Q2, 2023 net profit rose 20% YoY, despite massive price cuts for their vehicles. Tesla made ~$25 billion in revenue in Q2 (up 47% YoY), which puts them on a run rate of US$100 billion per annum in revenue. Q2 GAAP net income was a very nice US$2.7 billion. Looking ahead Tesla has multiple catalysts that can potentially surge revenue including – Cybertruck and Semi sales, Megapack sales, a Compact Tesla (Model 2) coming soon, and their AI potential via Full Self Driving (“FSD”) (robotaxis, Dojo, and Optimus robot).

Tesla recently revealed their updated Model 3 with sleeker styling, longer range, new interior features and much more

Closing remarks

For the skeptics out there who think the EV boom will not happen please read the next two sentences. Tesla Model Y became ‘the best-selling vehicle globally‘ (of all types) in Q1, 2023. BYD is now ‘the 5th largest carmaker globally‘ with 4.7% market share, based on July 2023 sales.

The EV boom is not only happening, it is happening faster than what most people thought.

BYD and Tesla now sell 36.6% of all global plugin electric car sales and are totally dominating the market. Little wonder both companies have enjoyed spectacular investment returns for shareholders over the past 5 years and look set to continue this decade.

Investor.News will continue to update investors on the progress of Tesla and BYD in 2023, as well as give some updates on their new products and other business divisions such as energy storage which is growing even faster than EVs.