Technology Metals Report (04.12.2024): Gina Rinehart Steps into the Critical Minerals Ring, while Copper Prepares for a Bull Ride

Welcome to the latest issue of the Technology Metals Report (TMR), brought to you by the Critical Minerals Institute (CMI). In this edition, we compile the most impactful stories shared by our CMI Directors over the past week, reflecting the dynamic and evolving nature of the critical minerals and technology metals industry. Among the key stories featured in this report are the surging success of Vulcan Energy Resources Ltd. (ASX: VUL), backed by Gina Rinehart, in lithium production, signaling a significant advancement in battery technology. Additionally, we explore the implications of copper’s climb to a 2024 high, heralded by Citi analysts as the start of the metal’s second bull market this century, amidst concerns about sustainability and market dynamics. We also delve into the ramifications of Chinese car manufacturing in Italy on Stellantis and the challenges faced by Volkswagen amidst a resurgence in petrol car demand in Europe, among other crucial developments shaping the industry landscape.

This week’s TMR Report also highlights the strategic moves of influential figures like Gina Rinehart, whose investments in the U.S. rare earths sector and Brazil hint at potential industry mergers and reshaping of the global rare earths supply chain. Furthermore, we discuss the imperative for the United States to strengthen its commercial ties with African nations to secure key minerals, aiming to reduce dependency on China. Amidst fluctuating rare earths prices in China and U.S. efforts to bolster domestic mining projects, we explore the intersection of environmental concerns with mining practices, exemplified by Australian billionaire Andrew Forrest’s call for greener nickel production. Lastly, we examine Canada’s risk of losing its position as a major mining capital due to government opacity surrounding Chinese investments in the critical minerals sector, highlighting the broader implications of uncertain investment policies on the industry’s strategic positioning.

To become a CMI member and stay informed on these and other topics, click here

Gina Rinehart-Backed Lithium Hopeful Surges After Demo Batch: (April 11, 2024, Source) — Vulcan Energy Resources Ltd. (ASX: VUL), an Australia-listed lithium developer, experienced a surge of nearly 40% in its stock value after announcing the successful production of a demo batch of lithium chloride using direct-extraction technology (DLE) at its demonstration plant in Landau, Germany. This marks a significant advancement in lithium production for batteries, showcasing the potential of DLE to streamline the production process. Vulcan, backed by Australia’s wealthiest individual Gina Rinehart, has established supply agreements with major European car manufacturers like Stellantis, Renault SA, and Volkswagen AG. The company’s achievement was hailed as a validation of Vulcan’s efforts and the viability of DLE in the lithium supply chain. Vulcan aims to commence commercial production in 2026, targeting an annual output sufficient to support half a million electric vehicles, while still seeking necessary funding. The project promises reduced carbon emissions by utilizing geothermal energy.

Copper prices climb to 2024 high as Citi calls the start of the metal’s second bull market this century: (April 10, 2024, Source) — Copper prices have surged to their highest levels since June 2022, with May delivery trading at $4.323 per pound in New York and three-month prices on the London Metal Exchange rising to $9,477 per metric ton. This increase reflects growing demand for copper, seen as an indicator of economic health and a vital component of the energy transition, including electric vehicles, power grids, and wind turbines. Citi analysts herald the start of copper’s second secular bull market of the century, predicting prices could average $10,000 per metric ton by year’s end and potentially rise to $15,000 in a bullish scenario. However, concerns exist about the sustainability of these price levels, with some analysts warning that high prices could dampen demand through substitution or demand destruction, emphasizing the self-regulating nature of commodity markets.

Chinese car manufacturing in Italy could force tough decisions, says Stellantis CEO: (April 10, 2024, Source) — Stellantis N.V. (NYSE: STLA) CEO Carlos Tavares warned of tough decisions, including potential plant closures, as Chinese car manufacturing in Italy could introduce new competition, notably from automakers like Chery Auto. The Italian government’s negotiations with Tesla Inc. (NASDAQ: TSLA) and Chinese companies aim to boost Italy’s automotive production. Tavares emphasized the pressure on Stellantis, Italy’s only major automaker, could lead to efforts to increase productivity to stay competitive, potentially affecting market share and necessitating a reduction in the number of plants. Despite rumors, Tavares confirmed Stellantis’s commitment to Italy, highlighting investments such as the extension of Fiat Panda’s production until 2030 and the inauguration of a facility for electrified transmissions at Mirafiori. He dismissed speculation about divesting from Italy as “fake news.”

Volkswagen electric car sales plunge as Europe returns to petrol: (April 10, 2024, Source) — Volkswagen’s electric vehicle (EV) sales in Europe plummeted by nearly a quarter in the first quarter of the year, amid a resurgence in petrol car demand, driven by high inflation and rising energy costs. This decline contrasts with a modest 3% global dip in all-electric sales and a 4% rise in combustion engine vehicle sales. The shift comes as governments reevaluate EV subsidies and emissions targets, with the UK delaying its ban on new petrol and diesel sales from 2030 to 2035, and the EU considering allowances for synthetic fuels. This backdrop of diminishing government support and increased competition from more affordably priced Chinese EVs, such as those from BYD, has pressured Volkswagen’s sales. Despite these challenges, Volkswagen experienced a significant 91% surge in EV sales in China, underscoring the regional disparities in EV adoption trends. Other manufacturers like BMW and Tesla also report varying EV sales performance, highlighting the evolving and competitive landscape of the global electric vehicle market.

China’s Tianqi Lithium’s $4bn bet on Chile at risk of backfiring: (April 9, 2024, Source) — In 2018, Tianqi Lithium, a major Chinese lithium producer, invested $4 billion to acquire a significant stake in Chile’s SQM, a move aimed at securing a strong position in the global lithium market, essential for electric vehicles. This investment in the heart of the “lithium triangle” (Argentina, Bolivia, and Chile) now faces challenges due to Chile’s government seeking greater control over lithium resources, particularly in the Atacama Desert where SQM operates. SQM’s agreement with Codelco, a state-owned enterprise, to form a joint venture aligns with Chilean policies for public-private partnerships in strategic sectors, potentially diminishing Tianqi’s influence and future prospects in SQM’s lithium venture. This development is part of a broader trend where countries are reclaiming control over critical minerals for the green transition, affecting companies like Tianqi, whose profitability and market position are under pressure from changing regulations, market dynamics, and operational challenges, both in Chile and globally.

Rinehart’s MP Buy Could Trigger Rare Earths Mining Mega Merger: (April 9, 2024, Source) — Gina Rinehart, Australia’s wealthiest person and iron ore magnate, has made a significant move into the U.S. rare earths sector by acquiring a 5.3% stake in MP Materials Corp. (NYSE: MP), which owns the Mountain Pass mine in California. This purchase has led to a 20% increase in MP’s share price within five days. Rinehart’s investment extends beyond MP to a 10% stake in Arafura Rare Earths Limited (ASX: ARU), an Australian rare earth producer, and 5.8% in a Brazilian company. Amidst growing competition with China and threats to “weaponize” its dominance in rare earths essential for modern technologies, Rinehart’s actions hint at potential for a major merger, particularly between MP and Australia’s Lynas Rare Earths Ltd. (ASX: LYC), aiming to create a significant non-Chinese rare earth supply. This development could signal strategic shifts in global rare earths production, with potential large-scale industry consolidation on the horizon.

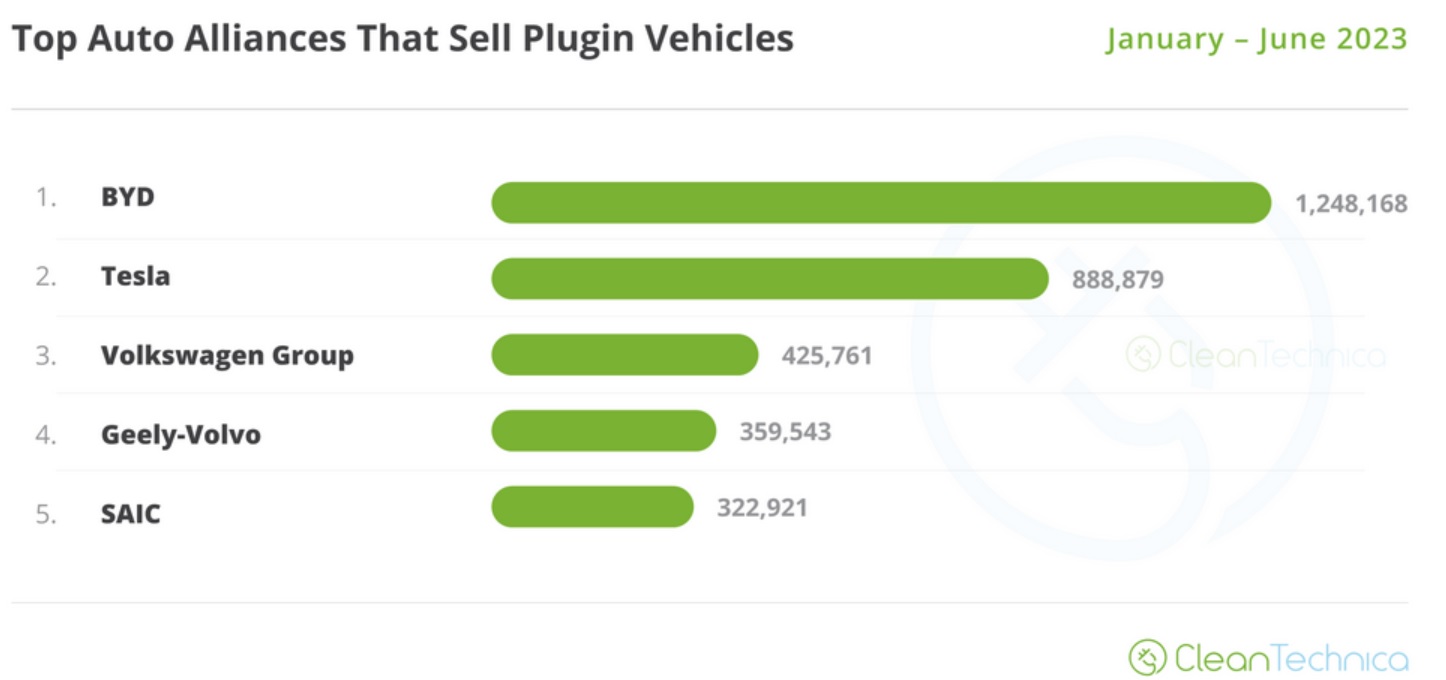

China’s EV export boom fuels surge in demand for new car-carrying ships: (April 9, 2024, Source) — Amidst a burgeoning demand for electric vehicles (EVs), Chinese automakers and shippers are investing heavily in a fleet expansion, ordering a record number of car-carrying ships. This surge places China on a trajectory to possess the world’s fourth-largest car-carrying fleet by 2028, ascending from its current eighth position. Major corporations like SAIC Motor, Chery Automobile, and EV titan BYD, along with shippers such as COSCO and China Merchants, are spearheading this initiative, accounting for a quarter of global orders. This influx primarily benefits Chinese shipyards, capturing 82% of the global orders. The expansion into foreign markets, buoyed by a cost-efficient supply chain, has been crucial for Chinese automakers facing domestic challenges like price competition and a slow economy. Notably, China has surpassed Japan as the premier auto exporter, with significant contributions from companies like BYD. However, this export growth has raised concerns in the U.S. and EU about market oversaturation with low-priced goods, though China rebuts, highlighting innovation and downplaying state support’s role.

US must boost Africa ties to secure key minerals, report says: (April 9, 2024, Source) — To secure vital minerals critical for sectors ranging from electric vehicle production to defense, the United States must strengthen its commercial relationships with African nations, a report from the United States Institute of Peace emphasizes. This is to reduce dependency on China, which currently dominates the supply of these critical minerals. The U.S.’s near-total reliance on foreign sources, especially China, for these materials poses significant economic and national security risks. The report highlights the lag of Western mining companies behind Chinese counterparts in tapping into Africa’s rich mineral resources. It suggests enhanced U.S. commercial diplomacy, particularly with leading mineral suppliers like the Democratic Republic of Congo and Zambia. Additionally, it points out the competition from Middle East firms and proposes measures like increasing project financing and reopening the U.S. consulate in Lubumbashi to facilitate U.S. investment. Despite challenges, the report argues for a more vigorous approach to match China’s influence in Africa’s mining sector.

Rare earths prices in China hit 7-week high on post-holiday restocking: (April 9, 2024, Source) — Rare earths prices in China, the world’s leading producer, reached a seven-week peak on April 8 due to increased post-holiday restocking, before slightly declining the following day. With China dominating 70% of mining and 90% of the refined rare earths market, notable increases were observed in praseodymium oxide and terbium oxide prices, highlighting the country’s significant influence on the market. The demand surge, particularly after the QingMing Festival, led to a depletion of in-plant stocks among magnetic materials producers, who then turned to the spot market for replenishment. Additionally, the use of ore cargoes as collateral by some to alleviate financial pressures contributed to the price hike. The start of the rainy season in Myanmar, a major supplier, is expected to reduce ore availability, potentially increasing market volatility as companies rely more on spot market purchases, impacting long-term contract stability. Consequently, shares in China Northern Rare Earth (Group) High-Tech saw a 4.3% increase.

Perpetua Resources gets nod to seek $1.8 bln US loan for antimony mine: (April 8, 2024, Source) — Perpetua Resources Corp. (NASDAQ: PPTA | TSX: PPTA) has received preliminary approval from the U.S. Export-Import Bank (EXIM) for a $1.8 billion loan to develop an antimony and gold mine in northern Idaho, aligning with efforts to reduce China’s dominance in critical minerals. This potential loan marks one of the largest U.S. investments in the mining sector, reflecting the Biden administration’s strategy of using federal funds to support projects that compete with Chinese firms. In addition to this loan, Perpetua will seek extra equity funding. The Stibnite mine aims to become the only U.S. source of antimony, vital for military hardware and electric vehicle batteries, while also harboring substantial gold reserves. This venture is part of a broader U.S. initiative to secure domestic supplies of essential minerals and counter China’s market influence.

Mining billionaire Forrest urges China to demand greener nickel: (April 7, 2024, Source) — Australian mining billionaire Andrew Forrest has publicly called for China to implement and enforce higher environmental standards within its global supply chains, especially focusing on nickel processing in Indonesia, citing severe environmental damage. In a Financial Times interview, Forrest, who is the chair and largest shareholder of Fortescue Ltd. (ASX: FMG), criticized the extraction of Indonesian nickel for its extensive environmental degradation and urged electric vehicle manufacturers to be cautious when sourcing nickel from Indonesia. Forrest highlighted that China’s increasing control over Indonesia’s nickel production, vital for electric car batteries and steelmaking, comes with significant environmental concerns, including deforestation, mining waste pollution, and high carbon emissions from coal power. Despite shutting down his nickel mines in Western Australia due to price drops influenced by Indonesian nickel, Forrest remains vocal about the need for a “green premium” for sustainably produced nickel and criticizes the lack of differentiation in the market. The call comes amid rising environmental scrutiny and the potential for market-driven adjustments to reflect the environmental cost of production.

Canada risks losing mining capital because of government opacity around Chinese investment in critical minerals sector: (April 5, 2024, Source) — The opacity of the Canadian government regarding Chinese investment in the critical minerals sector is leading to investor uncertainty and risking Canada’s position as a major capital source for mining. Despite Ottawa’s late 2022 announcement allowing Chinese investments only under “exceptional circumstances” without defining them, transactions continue, confusing the market. For instance, Shenghe Resources acquired a 10% stake in Vital Metals Ltd. (ASX: VML), owner of Canada’s only operating rare earths mine, even purchasing a significant stockpile of rare earths mined in Canada. Critics, including those from the Macdonald-Laurier Institute, find it problematic, especially given China’s dominance in the rare earths market. The unclear stance and handling of investments, such as the blocked financing deal for SRG Mining Inc. (TSXV: SRG)., reflect a broader uncertainty and potential discouragement of future critical minerals companies from basing in Canada, fearing the government’s unpredictable investment policies. This situation may drive new companies to other countries, impacting Canada’s mining capital and strategic positioning in critical minerals.

Investor.News Critical Minerals Videos:

- April 12, 2024 – Defense Metals Dr. Moreno on the Wicheeda Project Poised to Become North America’s Next Rare Earth Mine https://bit.ly/3TXs7kh

Critical Minerals IN8.Pro Member News Releases:

- April 10, 2024 – American Rare Earths’ Assay Results Expand Rare Earth Enrichment Within the Cowboy State Mine Area at Halleck Creek, Wyoming https://bit.ly/3JecWOT

- April 10, 2024 – Critical Metals PLC: Issue of Convertible Loan Notes and Corporate Update https://bit.ly/4aLZ75P

- April 10, 2024 – Mount Squires Project Option Agreement to unlock potential further rare earth supply https://bit.ly/440rco4

- April 09, 2024 – Pekuakamiulnuatsh First Nation and First Phosphate Announce Collaboration Agreement https://bit.ly/4d2nH4C