World Renowned Critical Minerals Expert Constantine Karayannopoulos is Bullish on Lithium

written by InvestorNews | March 19, 2024

In an insightful interview with Tracy Weslosky of InvestorNews, Constantine Karayannopoulos, a renowned expert in the field of critical minerals, shared his perspectives on the current state and future prospects of the critical minerals market. Karayannopoulos highlighted the pivotal role of critical minerals such as rare earths, lithium, and nickel in the burgeoning sectors of battery technology and electric vehicles (EVs), underscoring the global buzz around these resources. He noted the current challenges faced by small companies in raising funds and the general market sentiment. Despite these hurdles, he expressed optimism, suggesting that the downturn in valuations and financing is temporary. “We’re at close to or at the bottom of the cycle with a lot of these commodities,” he stated, advising resilience for these firms in anticipation of a market rebound fueled by sustained demand for technologies reliant on critical minerals.

Karayannopoulos offered insightful commentary on the critical minerals market, particularly focusing on lithium and rare earths. With a bullish stance on lithium, he reminisced about the industry’s past pricing projections and observed the current market’s resilience despite recent price drops. “Lithium still is the workhorse in the battery space… for the next decade, lithium will be the workhorse of the EV battery,” he affirmed, advocating for strategic investments in this area during market lows. His observations extended to the rare earths market, noting its sensitivity to Chinese economic dynamics and the potential for price stabilization in the near term. Highlighting Brazil’s emerging role in diversifying the global supply of heavy rare earths, he emphasized the importance of exploring favorable mineralogy and environmental practices in new geographies. This strategic diversification, he argued, is crucial for addressing the geopolitical and social concerns associated with current heavy rare earths sourcing, primarily from Myanmar.

Don’t miss other InvestorNews interviews. Subscribe to the InvestorNews YouTube channel by clicking here

The Critical Minerals Institute Report (12.27.2023): Politics Driving Marketable Commodities into 2024

written by Matt Bohlsen | March 19, 2024

Welcome to the December 2023 Critical Minerals Institute (“CMI”) report, designed to keep you up to date on all the latest major news across the critical minerals markets. Here is the CMI List of Critical Minerals or click here to visit the CMI Library.

Global macro view

December 2023 saw a further fall in U.S. inflation from 3.2%pa in October to 3.1%pa in November. As expected the U.S. Fed left interest rates unchanged at their December meeting. Even more significant was the Fed indicated that there are potentially ‘3 interest rate cuts coming’ in 2024. This was an early Christmas present for U.S. equity markets which continued their recent rally. Year to date, as of December 26, 2023, the S&P 500 is up 25.75% and the NASDAQ is up an amazing 43.25%. Of course, this follows heavy falls in 2022.

In late December China signaled a possible early 2024 interest rate cut when they reduced bank deposit rates. As a result China 30 year government bond yields hit their lowest level since 2005. All of this recent support for China’s economy and property market looks likely to set up a potential China recovery story in 2024. If China starts to recover in 2024 it would be a positive for commodity markets including the critical minerals.

The Russia-Ukraine war drags on through the European winter. There are some very early signs that both sides may be willing to end the war in 2024. We will see. Meanwhile, the Hamas-Israel war has been contained for now. We can only hope for peace in 2024.

Global plugin electric vehicle (“EV”) update

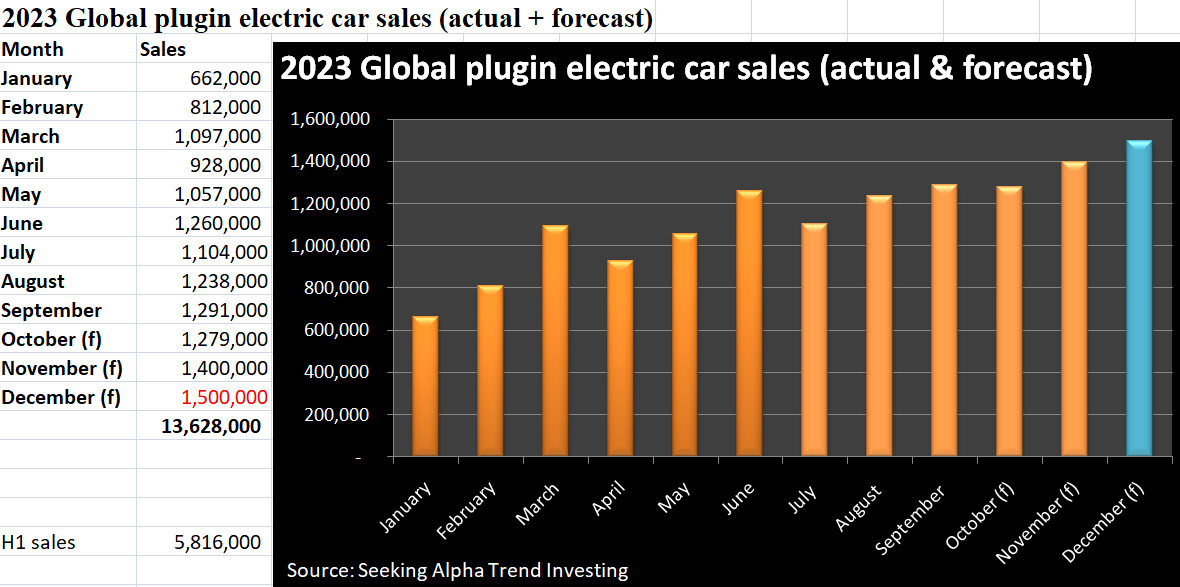

Global plugin electric car sales were 1,279,000 in October 2023 (the second-best month ever), up 37% YoY. November global sales reached 1.4 million. December should be even better. CPCA expects China’s NEV (New Energy Vehicle) retail sales in December 2023 to reach a record 940,000 units (41.4% market share), up 46.6% YoY. That should mean December global EV sales will be around 1.5 million.

This means that 2023 global plugin electric car sales should end up close to 13.6 million (~17% market share), for a growth rate of ~29% YoY (a significant slowdown from the 56% growth rate in 2022).

In other EV related news, in December Germany announced an abrupt ending to their EV subsidy. The subsidy was originally intended to apply until the end of 2024.

We also heard news that the U.S. is considering raising tariffs on Chinese EVs and Chinese solar products. The White House plans to complete a tariff review in early 2024. Chinese EVs entering the USA already have a 25% tariff. This follows the EU’s probe into China subsidies for EVs. All of this has come about due to the fact that about 60% of all global plugin EV sales are in China and the fact that China completely dominates the EV market and EV supply chain. This is now leading to a flood of compelling Chinese electric cars being exported to global markets where Western manufacturers (excluding Tesla Inc. (NASDAQ: TSLA)) are struggling to compete with China.

Finally, in December it was announced that Canada will require all new cars and trucks to be zero-emissions vehicles by 2035. The Canadian government stated: “The Standard will ensure that Canada can achieve a national target of 100 percent zero-emission vehicle sales by 2035. Interim targets of at least 20 percent of all sales by 2026, and at least 60 percent by 2030.”

Global critical minerals update

In December we got a key U.S. political announcement that will impact EV sales and critical minerals demand in 2024 and beyond.

U.S. Foreign Entity of Concern (“FEOC”) proposal

The U.S. DoE releases proposed interpretive guidance on Foreign Entity of Concern (“FEOC”) rules. FEOC’s include China, Russia, North Korea, and Iran. Key proposals include:

Beginning 2024, companies that have >25% ownership or control by a FEOC will not be eligible for tax credits available under the Inflation Reduction Act (IRA).

Beginning in 2024, an eligible clean vehicle (for IRA credits) may not contain any battery components that are manufactured or assembled by a FEOC.

Beginning in 2025, an eligible clean vehicle may not contain any critical minerals that were extracted, processed, or recycled by a FEOC.

These rules are quite strict and it is looking like the majority of EVs sold in the USA will not qualify in 2024 and hence not receive the subsidy of up to US$7,000 per vehicle. For example, the Tesla Model 3 and Model Y base range EVs use Chinese made LFP batteries, making them both ineligible to meet the FEOC rules. Things will only get harder in 2025. Of course, this is designed to motivate auto and battery OEMs to hurry up and build a new western battery supply chain, independent of FEOC.

The FEOC proposal follows last month’s news of new guidelines for the EU Critical Raw Materials Act (“CRMA”) as discussed here. A key ruling was that “not more than 65% of the Union’s consumption of each strategic raw material comes from a single third county.”

U.S. proposal to create a ‘Resilient Resource Reserve’ for key critical minerals

As reported in December, the U.S. select committee has recommended the creation of a critical mineral reserve to protect domestic industry. The Fastmarkets report stated:

“The adoption of such a reserve is intended to “insulate American producers from price volatility and (the People’s Republic of China’s) weaponization of its dominance in critical mineral supply chain. Such a reserve would be used to sustain the price of a critical mineral when prices fall below a certain threshold and would be replenished through contribution from companies when prices are “significantly” higher”…The fund would target critical metals where there is high price volatility, low US domestic production and import dependence on China. Cobalt, manganese, light and heavy rare earths, vanadium, gallium, graphite, germanium and boron are critical minerals that fall under that category, according to the report…”

Note: Bold emphasis by the author.

Lithium

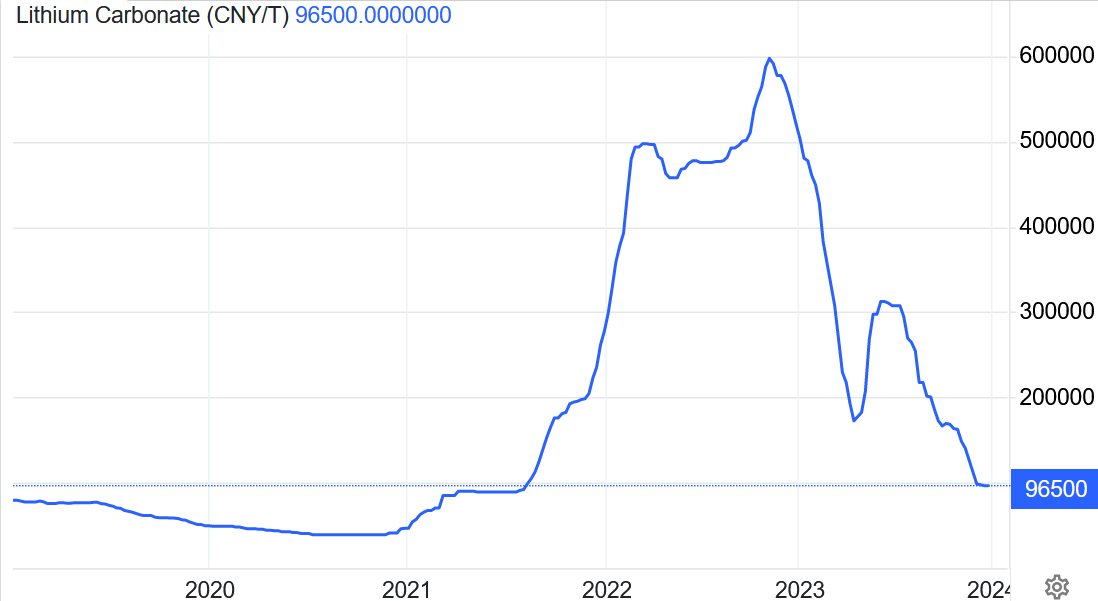

China lithium carbonate spot prices fell again in December 2023, with the price now at CNY 96,500/t (USD 13,505/t) and down 82% over the past year. Prices are now below the marginal cost of production, meaning a bottom should be found very soon (assuming EV sales hold up in 2024).

Industry participants are increasingly calling a likely bottom. For example, China Futures Co. analyst, Zhang Weixin, forecasts China’s lithium carbonate spot to bottom out between CNY 80- 90,000/t (US$11,200-US$12,600/t). Goldman Sachs is a little more bearish with a 1 year price target for China’s spot lithium carbonate of US$11,000/t.

The negative price action has not deterred SQM and Gina Reinhart’s Hancock Prospecting (private) who recently increased their bid to A$3.70 per share to takeover Australia’s Azure Minerals Limited (ASX: AZS).

In December we saw shareholders approve the Allkem Limited (ASX: AKE | TSX: AKE) – Livent Corporation (NYSE: LTHM) ‘merger of equals’ which is now expected to close by January 4, 2024. The new company is to be known as Arcadian Lithium PLC (NYSE: ALTM | ASX: LTM).

Finally, in December we got news that free markets supporter Javei Milei was elected as the new Argentina President. This is good news for those companies with mining projects in Argentina, of which there are many lithium projects under development.

The lithium carbonate spot price collapsed in 2023 and is now below the marginal cost of production and expected to form a bottom very soon

Neodymium prices fell in December to CNY 560,000/t almost 1/3 the price of the February 2022 peak. The one year outlook remains quite weak; however, this will largely depend on how China’s economy performs in 2024. A strong pickup in EV sales in 2024 could quickly change the market dynamics.

The big news in December in the rare earths market this month was China’s announcement to ban the export of rare earth processing technology. As discussed in an InvestorNews article, Western companies have been efficiently separating rare earths for some time, so this ban has minimal implications. CMI Co-Chair and rare earths expert, Jack Lifton, states: “Solvent extraction separation is a long-established practice everywhere. The issue is the production of rare earth metals and alloys and from them of rare earth permanent magnets. This is where China’s massive lead in manufacturing technology may be insurmountable. Time will tell.”

Of course, the trend for Western auto OEMs is concerning, especially following China’s recent introduction of export license permits on graphite products (including synthetic graphite, flake graphite, and spherical graphite).

Cobalt, Graphite, Nickel, Manganese, and other critical minerals

Cobalt prices (currently at US$12.91/lb) were lower the past month and continue to be very depressed. China’s slowdown and the slowdown in global electronics sales have suppressed cobalt demand at the same time as new supply from the DRC and Indonesia has risen.

One glimmer of hope for the Western cobalt producers is that the U.S. government announced in December the creation of a critical mineral ‘Resilient Resource Reserve’ (as discussed above).

Flake graphiteprices also remain very weak with prices near the marginal cost of production. Following the introduction of Chinese export license permits in December 2023 there has been some increased signs of buying activity and a slight graphite price improvement. However, the main concern for flake and spherical graphite is that lower energy input costs in China have lowered the cost of producing synthetic graphite, thereby dampening demand for flake and spherical graphite. Despite this, there are several analysts now forecasting graphite deficits to begin as soon as 2024/25 as you can read in a recent InvestorNews article here.

Nickel prices fell slightly in December to US$16,279/t. The 1 year outlook for nickel remains poor due to oversupply concerns from Indonesia. A recovering global economy and Chinese property sector will be needed to help balance the nickel market, which is currently in oversupply.

Manganeseprices also fell slightly in December and are now at CNY29.20/MTU.

2023 has been a tough year for many critical mineral prices (except for gallium, germanium, tellurium, indium, tin, and uranium – a critical mineral in Canada) as a slowing China and global economy weighed down demand at a time where supply increased. Uranium was the standout performer in 2023 with a gain of over 75%. You can read an article here from back in April 2023 where we highlighted the coming rise of uranium.

The key to watch in 2024 will be if we see lower interest rates in China trigger a China property and economy recovery. A stronger U.S. and Europe in 2024 would also help boost the global economy and demand for critical minerals. Lower interest rates in 2024 could potentially make it a great year for the auto sector and EV metals.

Wishing you all a safe and prosperous 2024 from the Critical Mineral Institute (“CMI”).

Biden-Harris Administration’s $3.5 Billion Investment in U.S. Battery Manufacturing and Clean Energy Transition

written by InvestorNews | March 19, 2024

On November 15, 2023, the Biden-Harris Administration announced a significant investment of $3.5 billion to enhance domestic battery manufacturing in the United States. This funding is a part of President Biden’s Investing in America agenda and is allocated from the Bipartisan Infrastructure Law. The U.S. Department of Energy (DOE) will oversee this investment, aimed at increasing the production of advanced batteries and related materials across the nation. The initiative is a key element in supporting the clean energy industries of the future, including renewable energy and electric vehicles.

The investment focuses on creating and retrofitting facilities for various components of battery production, such as battery-grade processed critical minerals, precursor materials, battery components, and cell and pack manufacturing. A significant aspect of this funding is its emphasis on job creation, specifically good-paying union jobs, and its contribution to the goal of achieving a net-zero emissions economy by 2050. Additionally, the investment aims to ensure that half of all new light-duty vehicle sales are electric vehicles by 2030 and to establish a robust domestic supply chain.

U.S. Secretary of Energy Jennifer M. Granholm highlighted the importance of this initiative in boosting global competitiveness, creating jobs, and strengthening the clean energy economy. The investment is seen as pivotal in positioning the United States as a leader in the advanced battery market, which is crucial for a range of applications including grid storage, home and business resilience, and transportation electrification. With the expected significant growth in the lithium battery market driven by the demand for electric vehicles (EVs) and stationary storage, the U.S. aims to accelerate the development of a resilient battery supply chain, including the exploration of non-lithium battery technologies.

This $3.5 billion funding is the second phase of a total $6 billion provided by the Bipartisan Infrastructure Law. The first phase saw the DOE awarding projects that catalyzed over $5.8 billion in combined public and private investment. The second phase continues this momentum by expanding domestic battery manufacturing and supply chains. Key objectives include enhancing the U.S. competitive stance in battery materials processing, advancing battery manufacturing capabilities, reducing dependency on foreign critical minerals and technologies, and supporting underserved communities through the Justice40 Initiative.

The funding opportunity is also set to prioritize next-generation technologies and battery chemistries beyond lithium-based technologies. It includes an emphasis on projects that increase the production of critical materials, expand production facilities for cathode and anode materials, and enhance battery component manufacturing. The DOE plans to update the focus areas of this program every six months to keep pace with market and technology developments, with concept papers due by January 9, 2024, and full applications by March 19, 2024.

Tracy Weslosky, Executive Director of the Critical Minerals Institute, often referred to as the CMI, stated that substantial funding is essential to develop competitive North American critical mineral operations that can match China’s pricing. However, she emphasized that finding professionals with the necessary skills, knowledge, and practical experience is even more crucial than the minerals themselves for establishing sustainable supply chains in North America. Weslosky also expressed eagerness for future updates on leadership and support strategies in this endeavor.

The Executive Director for Critical Metals PLC (LSE: CRTM) Russell Fryer adds: “The current dynamics of cobalt supply for battery production raise significant questions. Notably, sources such as Idaho and Canada are not major contributors in this realm. This situation underscores the need for a comprehensive understanding of global supply chains and their implications for sustainable and ethical resource procurement.”

The DOE’s Office of Manufacturing and Energy Supply Chains (MESC) is tasked with managing this initiative, aligning it with broader efforts to modernize national energy infrastructure and promote a clean and equitable energy transition.

Collaboration Deal with Sumitomo, Nano One to Boost LFP Cathode Production in Canada

written by InvestorNews | March 19, 2024

Nano One Materials Corp. (TSX: NANO) operates the sole North American lithium iron phosphate (LFP) production facility located in Candiac, Quebec, with plans to convert the existing facility to the One-Pot process for production up to 2,000tpa by the end of 2024. The company will expand the production in Quebec to meet demand and its business model incorporates licensing and joint ventures for global expansion.

In an announcement on September 14, 2023, Nano One reported significant progress in demonstrating full commercial scale volumes from the Candiac facility. The company states:

“Recent One-Pot trials at the Candiac plant have yielded LFP at commercial scale with results mirroring lab performance. Transitioning to full commercial size reactors, Nano One’s LFP is ready for Q4 customer evaluations. Moreover, installation and optimization of the 200tpa reactors are ongoing.”

Additionally, Nano One recently announced a collaboration agreement with global cathode materials giant Sumitomo Metal Mining on September 25, 2023. This announcement included a strategic equity investment of C$16.9 million commitment and will undoubtedly provide potential opportunities in sales, licensing, and partnership opportunities. Notably, Sumitomo is a supplier of materials to Panasonic which in turn supplies Tesla with battery cells which shows the quality of their client lists.

Sumitomo’s established role in the sector as a leading miner, refiner, and cathode active materials producer solidifies the significance of this collaboration.

With global trends leaning towards the electrification of transport and clean energy, the demand for batteries and cathode materials is surging. Forecasts predict the cathode market in North America and Europe alone to reach US$85 billion by 2035, presenting unprecedented opportunities for emerging market players.

Nano One’s Business Strategy

While Nano One’s strategy remains versatile, the primary focus will be LFP production initially in Canada at the Candiac facility. Its business model includes licensing and joint ventures with partners for global expansion in jurisdictions like the US, Europe, and Asia.

In Conclusion

Nano One’s evolution from a minor participant to a significant player in the cathode materials sector is evident. Collaborations with industry leaders like Sumitomo, Rio Tinto and VW place them prominently on the map. The company currently boasts a market cap of C$320 million.

BYD and Tesla are totally dominating global electric car sales in 2023

written by Matt Bohlsen | March 19, 2024

Many people would probably be surprised to hear how poorly legacy car manufacturers are doing in terms of electric car sales. They would also be shocked how just two companies are totally dominating global plugin electric car sales. Those two companies are BYD Co. Ltd. (OTC: BYDDF) and Tesla Inc. (NASDAQ: TSLA).

BYD dominates total sales with about half coming from pure electric cars and about half from plugin hybrids. Tesla dominates in terms of total revenues as well as profit per vehicle.

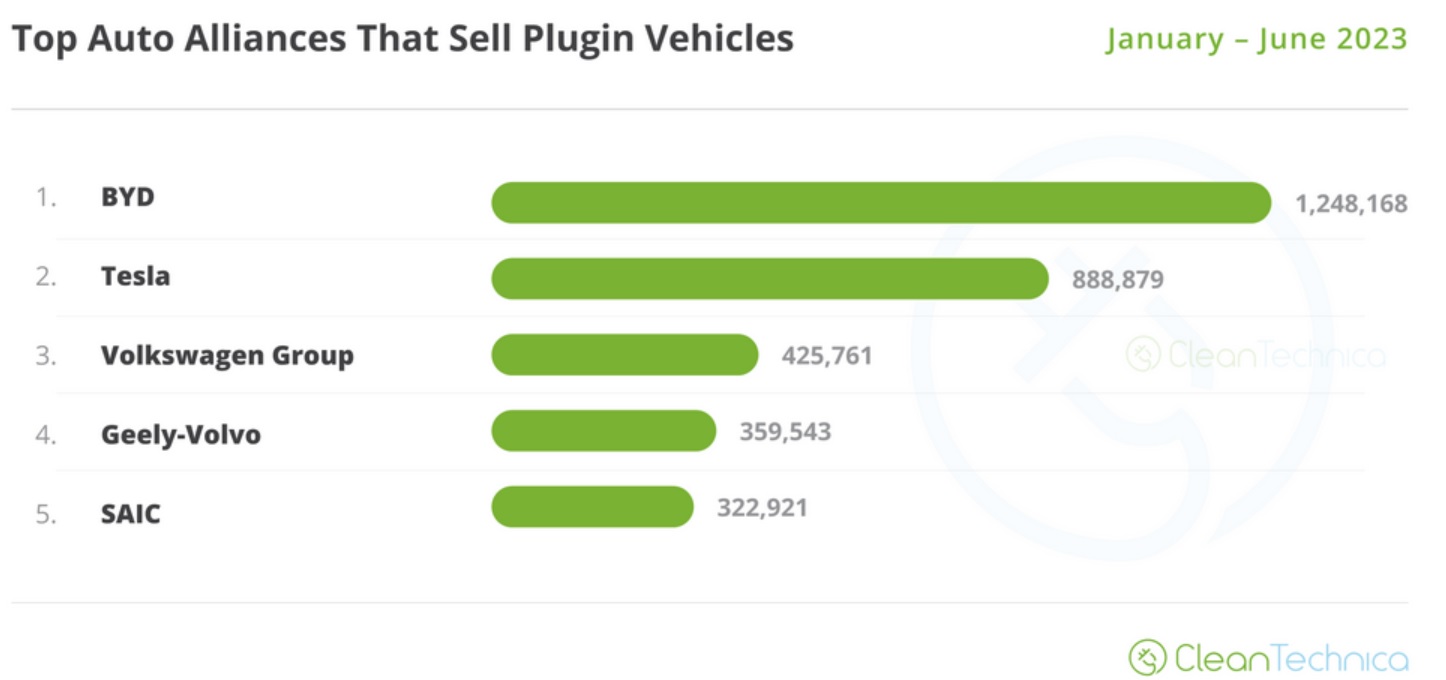

The chart below shows H1, 2023 global plugin electric car sales with BYD leading on 1,248,168 sales and Tesla on 888,879 sales.

The next closest is the Volkswagen Group with 425,761 sales, roughly a third of BYD and half of Tesla.

Top selling global plugin electric car auto groups Jan-June, 2023

Tesla and BYD’s lead looks set to continue in 2023, currently with a combined 36.6% of the market

Tesla and BYD have been expanding their manufacturing facilities at a feverish pace for the past several years and the results are now showing. Furthermore, by the end of 2023, their lead will be even bigger, in raw number terms. Tesla targets 1.8 million sales and BYD a massive 3 million sales in 2023.

Results like this are leaving internal combustion energy (“ICE”) legacy auto companies at risk of becoming extinct this decade as the world transitions rapidly towards EVs. For example, Toyota only sold 46,171 pure battery electric vehicles globally in H1, 2023.

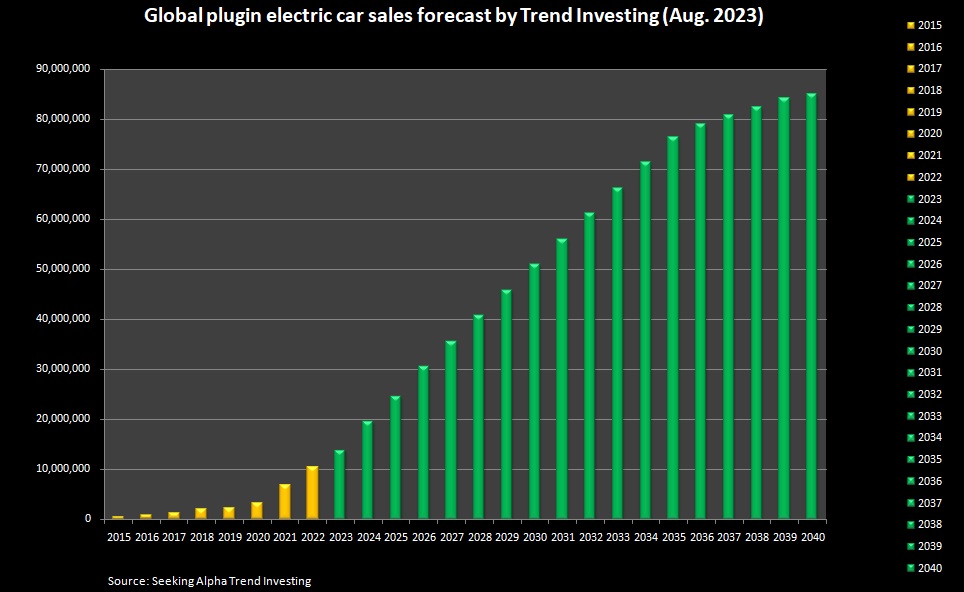

As shown on the chart below we are still in the early stages of the EV boom with sales forecast to increase exponentially over the next 10-15 years. Given the current dominance of BYD and Tesla, it is looking like they will get a major part of these future sales.

BYD is currently ranked number 1 globally with 21.4% market share YTD (Jan-June 2023).

Tesla is currently ranked number 2 globally with 15.2% global market YTD (Jan-June 2023).

Combined BYD and Tesla currently have 36.6% of the global plugin electric car market.

Global plugin electric car sales forecast to 2040 (green bars)

BYD sales continue to boom with 261,105 sold in July and 274,086 electric cars sold in August 2023. Tesla’s sales will be released at the end of Q3.

Takeaway for investors

BYD and Tesla are dominating global sales. They are really the only two companies selling electric cars at a profit and it shows with their tremendous growth in profits in recent years.

As reported on August 29, 2023, BYD posted a >200% surge in first half profit, with net profit in the first six months rising 204.68% to 10.95 billion yuan (US$1.50 billion), as compared to 3.6 billion yuan a year earlier.

Tesla’s Q2, 2023 net profit rose 20% YoY, despite massive price cuts for their vehicles. Tesla made ~$25 billion in revenue in Q2 (up 47% YoY), which puts them on a run rate of US$100 billion per annum in revenue. Q2 GAAP net income was a very nice US$2.7 billion. Looking ahead Tesla has multiple catalysts that can potentially surge revenue including – Cybertruck and Semi sales, Megapack sales, a Compact Tesla (Model 2) coming soon, and their AI potential via Full Self Driving (“FSD”) (robotaxis, Dojo, and Optimus robot).

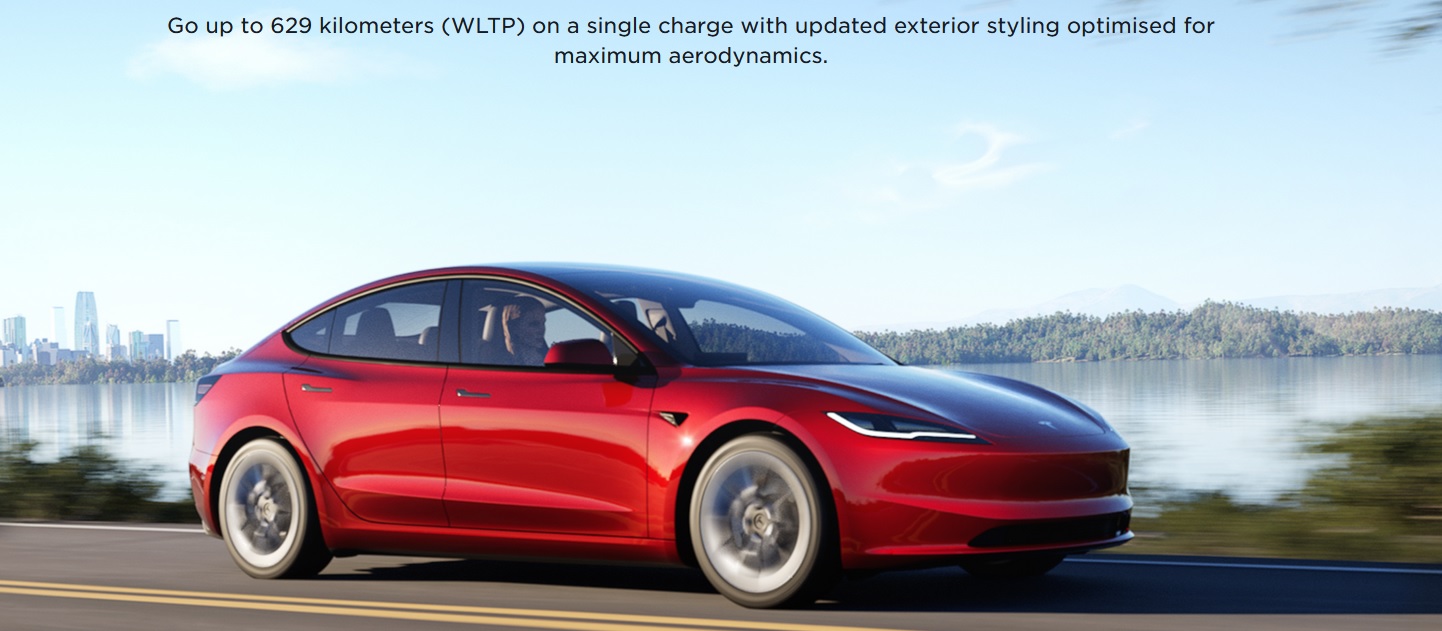

Tesla recently revealed their updated Model 3 with sleeker styling, longer range, new interior featuresand much more

For the skeptics out there who think the EV boom will not happen please read the next two sentences. Tesla Model Y became ‘the best-selling vehicle globally‘ (of all types) in Q1, 2023. BYD is now ‘the 5th largest carmaker globally‘ with 4.7% market share, based on July 2023 sales.

The EV boom is not only happening, it is happening faster than what most people thought.

BYD and Tesla now sell 36.6% of all global plugin electric car sales and are totally dominating the market. Little wonder both companies have enjoyed spectacular investment returns for shareholders over the past 5 years and look set to continue this decade.

Investor.News will continue to update investors on the progress of Tesla and BYD in 2023, as well as give some updates on their new products and other business divisions such as energy storage which is growing even faster than EVs.

Innovations for Tomorrow: The Must-Attend InvestorTalk Series of August 2023

written by Tracy Weslosky | March 19, 2024

As we catapult into a future shaped by quantum cybersecurity, green hydrogen, and state-of-the-art EV battery technology, the next week’s InvestorTalk events stand as your passport to the bleeding edge of innovation. Set your calendars; these sessions are brimming with insights and revelations.

Quantum eMotion Corp.(TSXV: QNC | OTCQB: QNCCF): On August 15, delve deep into the fabric of quantum mechanics with Francis Bellido. As cyber threats evolve, Quantum eMotion is ensuring our digital fortresses stand impregnable. Their patented Quantum Random Number Generator capitalizes on quantum unpredictability, heralding a new dawn in hardware security. Targets? Everything from Blockchain to Quantum Cryptography. Click Here to Register for this InvestorTalk at 9 AM EST.

SunHydrogen, Inc.(OTC: HYSR): Imagine powering tomorrow with sunlight and water. On August 16, Tim Young introduces us to the SunHydrogen Panel technology. With an ambition to fuel the emerging $12 trillion hydrogen economy, SunHydrogen aims to drive the future – emission-free. Click Here to Register for this InvestorTalk at 9 AM EST.

Nano One Materials Corp. (TSX: NANO): That same day, at 4 PM EST, Dan Blondal unveils the green magic behind efficient lithium-ion battery cathode materials. With giants like BASF and Rio Tinto as allies, Nano One’s technology eyes the vast expanse of electric vehicles, energy storage, and consumer electronics Click Here to Register for this InvestorTalk

The Grand InvestorTalk at The National Club: August 17 is an ensemble of visionaries:

Spencer Huh from NEO Battery Materials Ltd.(TSXV: NBM | OTCQB: NBMFF): Unearthing the potentials of silicon in EV lithium-ion batteries.

Bundeep Singh Rangar of Fineqia International Inc. (CSE: FNQ): Navigating the future web with digital assets, tokenization, and more.

Stephen Burega from Romios Gold Resources Inc. (TSXV: RG | OTCQB: RMIOF): From precious metals in the “Golden Triangle” of BC to global mineral explorations – it’s a golden journey.

Thomas Smeenk of Hemostemix Inc.(TSXV: HEM | OTCQB: HMTXF): Introducing blood-based stem cell therapeutics that have the potential to revolutionize healthcare.

RSVP for this event that kicks off at 9:30 AM EST by sending an email to [email protected]

Diving Deeper:

NEO Battery Materials Ltd.: Based in Vancouver, they’re redefining EV battery materials, particularly silicon anode materials, promising enhanced efficiency and capacity over traditional graphite anodes.

Romios Gold Resources Inc.: This Canadian mineral giant, with its vast claims spanning from BC’s “Golden Triangle” to Nevada, merges tradition with innovation in gold, copper, and silver explorations.

Hemostemix: A pioneer in autologous stem cell therapy since 2003, this World Economic Forum Technology Pioneer Award winner is scaling blood-based stem cell therapeutics, which promise groundbreaking treatments.

Fineqia: At the crossroads of the digital revolution, Fineqia is capitalizing on tokenization, blockchain tech, NFTs, AI, and fintech. From managing debt securities in the UK to investing in next-gen Internet technologies, they’re forging digital frontiers.

Prepare for a week of revelations and insights. Whether you’re a seasoned investor, an innovation enthusiast, or someone curious about tomorrow, next week’s InvestorTalks is a trove of enlightenment. Mark your schedule and be part of this journey into the future.

Elcora order is just the beginning of its journey in the manganese market

written by InvestorNews | March 19, 2024

Manganese is becoming a key part of the lithium-ion battery market, traditionally used in nickel, manganese, cobalt (“NCM”) batteries; but now it is also used in lithium manganese iron phosphate (“LMFP”) batteries. This new battery type offers greater energy density (and hence EV range) than the standard LFP battery. Manganese is still largely used in steel, but the battery demand looks set to grow much faster. Overall the global manganese market is expected to grow at a CAGR of 5.5% from 2023 to 2027.

LMFP batteries containing manganese are the latest development to improve lithium-ion batteries

As announced last month Gotion High-tech Co Ltd. (SHE: 002074) has developed a breakthrough LMFP battery that offers a “range of up to 1,000kms for a single charge and could last two million kms”. Their new battery pack will go into mass production in 2024.

In 2022 it was reported that “CATL will soon mass produce LMFP batteries”. Contemporary Amperex Technology Co., Limited (SHE: 300750) (“CATL”) is the world’s largest lithium-ion battery manufacturer by far with 37% market share and is a leading supplier of Tesla Inc. (NASDAQ: TSLA). At Tesla Battery Day in 2020, Elon Musk pointed out that Tesla targets to use manganese in its batteries for long-range electric cars.

At Tesla Battery Day 2020, Tesla targets to use nickel and ‘manganese’ batteries for long range vehicles where vehiclemass is not too large

Note: Red oval done by the author to highlight manganese

Today’s company made a key announcement this week regarding commencement of manganese ore sales.

Elcora Advanced Materials Corp.

Elcora Advanced Materials Corp. (TSXV: ERA | OTCQB: ECORF) (“Elcora”) is working towards becoming a vertically integrated battery material company. Elcora has developed a cost-effective process to purify high-quality battery metals and minerals that are commercially scalable.

Elcora’s key projects have graphite, manganese, and vanadium. Elcora also has exposure to anode materials and graphene.

“has received its first monthly order for 1000 metric tons of 37% + manganese ore. The delivery of the first part of the order is scheduled before the end of June 2023. The order was placed by a leading European customer looking for a long-term supply relationship and marks a significant milestone for Elcora’s mining division.“

The order is not large but it marks the beginning of what can be a good business for Elcora if they can achieve large-scale production. Manganese ore (37% Mn grade) currently trades at about US$3.13/ dmtu (Dry Metric Tonne Unit) FOB Port Elizabeth.

“The recurrence of orders is expected to generate significant revenue for Elcora Advanced Materials Corp, further strengthening its position in the industry. With the increasing demand for manganese ore, the company is well-positioned to meet the needs of its customers...Elcora Advanced Materials Corp is well-positioned to benefit from this growing demand, and this order is just the beginning of its journey in the manganese market.”

Elcora’s Atlas Fox Project in Morocco – Beni Mellal Manganese Deposit/Mine and the Ouarzazate Project (including the Omar Mine)

Elcora’s Atlas Fox Project in Morocco is rich in manganese. It is comprised of the Beni Mellal Manganese Deposit/Mine and the Ouarzazate Project (including the Omar Mine).

At the Beni Mellal concessions, Elcora has a 10-year Exploitation License. This manganese concession contains a surface deposit mine that operated during French colonial times. Elcora plans to leverage on-site infrastructure with ore ready for processing. In Q4 2023 Elcora plan to build a gravimetric concentrator to upgrade raw ore content (30% Mn) to 50% Mn and increase mine production to 2,500 to 3,000 t/month of 50% Mn concentrate.

At the Ouarzazate Project Omar Mine, Elcora has acquired exclusive mining rights and an option to purchase the 16 km² manganese mining concession. The concession contains both a surface deposit and underground mine. Elcora is leveraging on-site infrastructure and has existing manganese ore piles of approximately 6,000 tonnes that are ready for processing. Elcora plans to ramp up mining production to 2,500 tons per month at the Omar Mine.

Elcora’s overall manganese ore production capacity is targeted to be more than 5,000 metric tonnes per month from the above concessions.

Atlas Lion Vanadium Project in Morocco

Elcora owns the Atlas Lion Vanadium Project (304 Km2) concessions in Morocco. Elcora plans to further explore and develop these concessions with the goal of producing vanadium.

Elcora’s next steps for mining manganese and vanadium in Morocco

In total, Elcora currently owns seventeen polymetallic (vanadium, lead, other), one manganese (and one option to purchase) and one copper licences/concessions in Morocco.

Elcora is making strong progress on its goal to become an integrated battery metals producer. The Company already has the technology and facilities to purify high-quality battery metals (notably spherical graphite, graphene, and anode powder) and is now working on the mining side with manganese and vanadium (noting they already have a graphite mine). The Atlas Fox Projectin Morocco has commenced stockpiled manganese ore sales and plans to ramp up manganese ore production from its concessions to 5,000/t per month. Following this will be development work and potentially production from the Atlas Lion Vanadium Project, also in Morocco.

Elcora Advanced Materials Corp. trades on a market cap of only C$18 million, suggesting this may potentially be just the beginning for Elcora.

Government Subsidies Fuel Investment Frenzy in the Battery Gigafactory Race

written by InvestorNews | March 19, 2024

The news keeps on coming about new investments in battery gigafactories in North America as companies realize that governments are willing to throw stupid amounts of money at them in the form of grants, subsidies, and loans to make this dream come true. The leader of the pack is the U.S. Inflation Reduction Act (IRA), which was signed into law last August and offers US$369 billion of subsidies for electric vehicles and other clean technologies. The Act also incents EV makers to produce more vehicles in North America and secure the key minerals for them outside of China.

Not to be outdone, Canada is trying hard to compete with the U.S. by spending ghastly sums of taxpayers’ money to bring some of that activity north of the border. Time will tell if this will be a prudent use of ‘our’ hard-earned dollars but in the meantime let’s take a look at the latest news on the battery plant front.

Volkswagen to build its largest gigafactory in Southern Ontario

Last Friday, the Government of Canada let the ‘cat out of the bag’ as to how much it was willing to provide to lure Volkswagen AG (XTRA:VOW3) to Southern Ontario to build its largest gigafactory to date in St. Thomas, with an annual production capacity of up to 90 GWh in the final expansion phase. The Federal Government has agreed to provide up to C$13 billion (US$9.7 billion) in subsidies and a C$700 million grant, which does not include any potential funds from the provincial government of Ontario.

When you realize that this plant is expected to cost about C$7 billion to build, you can see why it was a pretty easy choice for VW. I’m pretty sure I could sell management on a deal like this back in the day when I was trying to put together infrastructure projects. In the Government’s defense, the numbers roughly match what Volkswagen would have received from the United States through the IRA. With that said, I’m still not convinced we should try and match what a country with 10 times our GDP is doing.

GM and Samsung to invest over US$3 billion to build a new EV battery manufacturing plant

Not to be outdone, the United States had a couple of announcements of its own to temper Canada’s ‘win’. Yesterday General Motors Co. (NYSE: GM) and Samsung SDI (KRX: 006400) said they will invest over US$3 billion to build a joint venture EV battery manufacturing plant in the U.S. (The companies did not identify the location of the plant.) The plant, expected to start production in 2026, aims to have an annual production capacity of 30 GWh.

This marks GM’s fourth U.S. battery manufacturing facility having already done 3 joint ventures with LG Energy Solution (KRX: 373220) in the form of Ultium Cells LLC plants, including a US$2.6 billion plant in Michigan set to open in 2024. In December, the U.S. Energy Department finalized a US$2.5 billion low-cost loan to the Ultium joint venture to help finance the construction of the new manufacturing facilities which also include Ohio and Tennessee.

Hyundai and SK On to build battery plant in Georgia

Not surprisingly, with South Korean President Yoon Suk Yeol in Washington to meet President Joe Biden this week, confirmation of another EV battery manufacturing facility joint venture was made. Although an MOU was signed last December, Hyundai Motor Company (KRX: 005380 | OTC: HYMLF) and SK On, a battery unit of SK Innovation Co. Ltd. (KRX: 096770) ratified plans yesterday to set up a battery JV in the state of Georgia, in an investment worth approximately US$5 billion.

When fully operational, Hyundai expects an annual production capacity of 35 GWh with the facility expected to begin manufacturing battery cells in the second half of 2025. These two companies appear to be embracing Georgia as their home away from South Korea given Hyundai separately broke ground in October on a US$5.54 billion electric vehicle and battery plant in Georgia’s Bryan County, while SK Innovation opened a US$2.6 billion battery plant in Commerce, Georgia, in January that is producing batteries for the Ford F-150 EV.

Battery metals supply concerns

This begs the question of where are all the raw materials to build all these batteries going to come from. Perhaps all these subsidies to attract the manufacturing facilities will be for not as we see others getting in on the act. And not just any “others” but those who already control more than half of global lithium resources, and include by far and away the world’s largest copper producer.

That’s right, while in Toronto last month for the PDAC Convention, Argentina’s Mining Undersecretary Fernanda Avila suggested that Argentina, Chile, Bolivia, and Brazil are planning to coordinate action on turning more of the region’s mined lithium into battery chemicals, as well as moving into manufacturing of batteries and even EVs.

It makes a lot of sense (at least to me) that these resource-rich nations would like to move further along the value chain by leveraging their mineral wealth into expanded processing capacity and perhaps as far as vehicle manufacturing. Chinese carmaker Chery Automobile Co. has already stated it wants to build a US$400 million EV and battery plant in Argentina in an effort to tap into the lithium triangle.

Another lithium-producing area of Argentina is in talks with China’s Ganfeng Lithium Co. (SHE: 002460 | HK: 1772 | OTC: GNENF) and Gotion High-tech Co. to make battery cathodes.

Final thoughts

Will this be another case of China being a better visionary when it comes to the electric vehicle supply chain? As a taxpayer who is helping to subsidize Volkswagen’s efforts, I certainly hope that isn’t the case. But then again, our government doesn’t exactly have a great track record of being efficient and effective stewards of capital.

Telsa Unveils ‘Masterplan 3’ and Ways to Invest in Renewable & Energy Transition Companies

written by Matt Bohlsen | March 19, 2024

Tesla‘s (NASDAQ: TSLA) Master Plan 3 was released in detail on April 5, 2023, and it gives the world a road map on how the world can transition to a clean sustainable energy future. It is arguably one of the most important documents ever released in history.

Key pillars of the plan include re-powering the existing grid with renewables (including solar, wind, geothermal, and hydro), switching to electric vehicles (“EVs”), switching to heat pumps, and some use of green hydrogen for high-temperature applications. Elon Musk also supports smart nuclear as a good base load power option, especially when compared to fossil fuel power, especially coal.

To achieve this, the world needs to build out a new infrastructure and a key part is stationary energy storage, mostly using batteries. Musk’s Master Plan 3 suggests we need a massive 240 TWh of energy storage globally to support both energy production and EVs. To get some perspective on this number, in 2022, the world produced only about 700 GWh of lithium-ion batteries. 240 TWh is equal to 240,000 GWh, which is 342x the current 700 GWh.

Of course, other energy storage apart from lithium-ion can be used, but certainly, the electric transport sector will rely on lithium-ion and it is estimated to need 112 TWh of the total 240 TWh needed. If the world was to steadily grow and reach 20TWh per annum (“pa”) of new energy storage production starting in 2030, then it would take 12 years (240/20=12) to reach the end goal sometime around 2042. In terms of costs, the plan suggests it would cost about US$10 trillion, which is only 10% of the world’s 2022 GDP. Also because electrification for transport and heat pumps are much more efficient, then the world would only need to produce 1/2 as much energy.

Tesla Master Plan 3 – The world needs 240 TWh of energy storage to become clean energy sustainableand avoid using fossil fuels

The fact that renowned investor Eric Sprott has recently added several new energy transition ETFs bodes well for the various sectors. It also helps individual and professional investors gain broad access to these markets via a single ticker.

Tesla continues to lead the world toward a clean and sustainable energy future. Their Master Plan 3 gives a concise and detailed picture of what needs to be done. It details solar and onshore wind as the two cheapest forms of energy production (page 19) and lithium-ion batteries as the cheapest energy storage (page 18) solution.

The clean energy transition has already begun with solar and wind as the fastest-growing new energy generation globally and battery energy storage global growth is set to double in 2023. To meet all the 240 TWh of global energy storage needed, lithium-ion battery capacity would need to grow by several hundred times. The global electric vehicle market share reached 13% in 2022 and is a key part of this megatrend.

The global energy transition and transport electrification is the biggest trend of our time, at least until the full build-out is completed by approximately 2050. Investors should embrace the change and understand it is inevitable.

Our children, grandchildren, and future generations will also want to enjoy a clean planet one day.

China Controls the Lithium Market and All the West Can Do (For Now) is Watch

written by Jack Lifton | March 19, 2024

Are lithium prices in free fall? Probably not. They are just moving to adjust supply to demand in China, and this is happening much faster than usual. The market is trying to “discover” the prices of lithium carbonate and lithium hydroxide. But this market is not controlled from New York or London, so traders there can only watch.

The global mining industry has been put on the path of a reckless exhaustion of natural resources by the largest commodity asset price inflation in history, caused, perhaps purposely, by America’s wanton “quantitative easing,” aka “printing money.” One result of this essentially free money was to allow the financializers to churn the world’s manufacturing industries’ enormous cashflow, particularly that of the OEM automotive industry, through the financial/political grinder. This event has now, in my opinion, brought that industry to its knees.

Along the way, it was necessary to develop the theme (fantasy?) of human being able to control the earth’s weather (aka, climate) by simply eliminating the use of the most widely available source of cheap energy, fossil fuels, which created our contemporary world’s economic progress for the last two centuries. Fossil fuels sustain our global economy as well as provide its ability to grow. Replacing it with a controlled and constrained energy industry that favors only the politically connected and richest individuals will ultimately reduce the majority of mankind back to expensive energy-caused penury thus reversing the growth of the last two centuries.

China and Lithium Prices

Gambling is very much a part of Chinese culture no matter what type of government the Middle-Kingdom has. Chinese traders love to bet on prices; they love to build and manipulate inventories to try to control prices.

Two-thirds of the world’s lithium, the most critical component of a lithium-ion battery is refined in China and 80% of the world’s lithium-ion batteries are made there.

The price of lithium is set in China and the market manipulations of Chinese trader-gamblers set that price.

Americans are shocked, shocked when the LME discovers that a nickel trader has deposited bags of stones rather than nickel metal as collateral.

In China, traders do not trust each other’s counts of physical inventory, and do the “bags of stones” thing a lot.

Lithium Prices and Western Ideas

It’s recently been said that Americans all too often presume that everyone else aspires to live and think as we do. Others must share our values, if only in secret, or at least be eager to learn them. This is a dangerous attitude to take with any nation or culture, but perhaps especially so with Russians and Chinese.

Its also been said that Western governments are filled to the brim with people entirely lacking in real-world experience or specialized knowledge.

The lithium markets are just reacting to forces that the USA and Europe do not control or really understand.